Alpha/Beta and Portable Alpha

{kind=link}

Alpha

For example, assume the S&P 500 is up 10% over a particular period and an investor’s portfolio is up 12%. The additional 2 percentage points above the benchmark (12%-10% = 2%) is referred to as Alpha.

Alpha can also be negative, as would be the case if the investor’s portfolio returned less than 10% (the benchmark).

Some skillful investment managers can and do add alpha. Over the long run though, studies have shown that doing so is very difficult. In fact, most managers have a hard time matching their benchmarks, let alone exceeding it. And therein lies the reason why passive investing (where you buy every stock in an index, such as the S&P 500, in order to match the return of the market) has become so popular over the recent years.

{kind=link}

Beta

Beta is both a measure of volatility as well as a term that describes exposure to a benchmark or index such as the S&P 500. It expresses the relative volatility of a stock relative to the market.

The market in this case is the S&P 500. If a stock has a beta of 1.20, it is 20% more volatile than the S&P 500. If the S&P 500 was up 10%, a stock with a beta of 1.20 would be expected to rise by 12%. If a stock has a beta of .80, it is only 80% as volatile as the market as a whole. If the S&P 500 advanced by 10%, a stock with a beta of .80 would be expected to rise only 8%.

An S&P 500 Index fund, which owns each of the 500 members of the index, has a beta of exactly 1.00. Hence, if an investor was buying beta, it would refer to investing in the market as a whole, usually through derivatives such as S&P 500 futures. If an investor wanted exposure to small cap beta, she might obtain this through E-mini Russell 2000 futures. Futures are a cheap and efficient way to obtain beta exposure.

Portable Alpha

{kind=link}

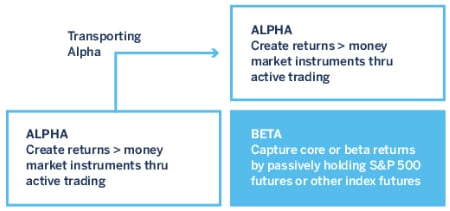

The result would be a strategy known as portable alpha.

Portable Alpha, also known as alpha transport or alpha-beta separation, is a strategy that uses derivatives to gain market exposure, coupled with an investment in a separate and distinct strategy (or set of strategies designed to generate excess returns), or alpha.

The market exposure obtained using derivatives such as stock index futures is typically described as beta, while the underlying capital investment that effectively collateralizes the derivatives exposure is commonly referred to as the alpha strategy. The goal is for the combined parts, the alpha strategy and the derivatives-based beta exposure, to generate an attractive risk adjusted excess return relative to a specified benchmark, generally the market index (beta) represented by a derivatives contract such as the S&P 500 futures.

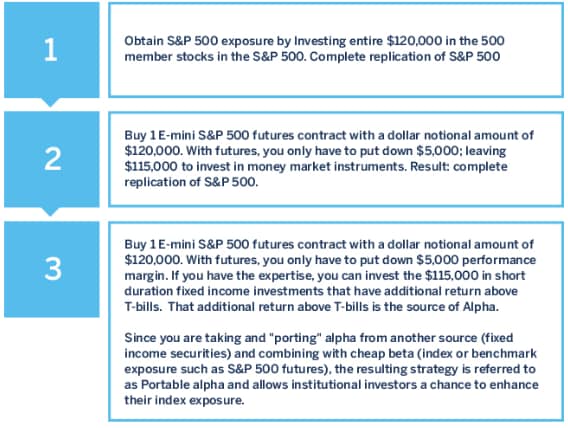

As long as the active fixed income investments returned greater than money market instruments, your returns would exceed the market or benchmark.

{kind=link}

Passive strategies strive to match the performance of a market index. Portable alpha strategies go further by combining active management with passive market exposure to enhance returns. This is especially important in an era of low investment returns in markets such as fixed income.

Blending Alpha and Beta

A Simple Portable Alpha illustration (Assume $120,000 investment)

{kind=link}

While the S&P 500 is a primary focus with equity portable alpha strategists, portable alpha can be done with nearly any benchmark, such as the Russell 2000, the S&P Midcap 400 as well as with fixed income portfolios and commodity investments.

Sources of Beta

- S&P 500 futures

- E-mini S&P 500 futures

- E-mini mid-cap 400 futures

- E-mini Russell 2000 futures

- Almost any benchmark that has a liquid derivative instrument.

Sources of Alpha that can be transported on top of Beta

- Fixed income securities (Treasury and agency bonds/notes, corporate bonds, mortgage-backed bonds/notes)

- Hedge funds and absolute return strategies

- Long/short strategies