Option Ratio Spreads

{kind=link}

Option Volatility Strategies – Ratio Spreads

Another commonly traded strategy is the ratio spread. A ratio spread consists of long and short options, the quantities of which are in simple mathematical ratios such as 2 to 1 or 3 to 2. Traders will refer to these spreads as a 1 by 2, or 2 by 3.

Ratio spreads generally consist of all calls or all puts, with the same expiration and the same product. There certainly can be exceptions to this.

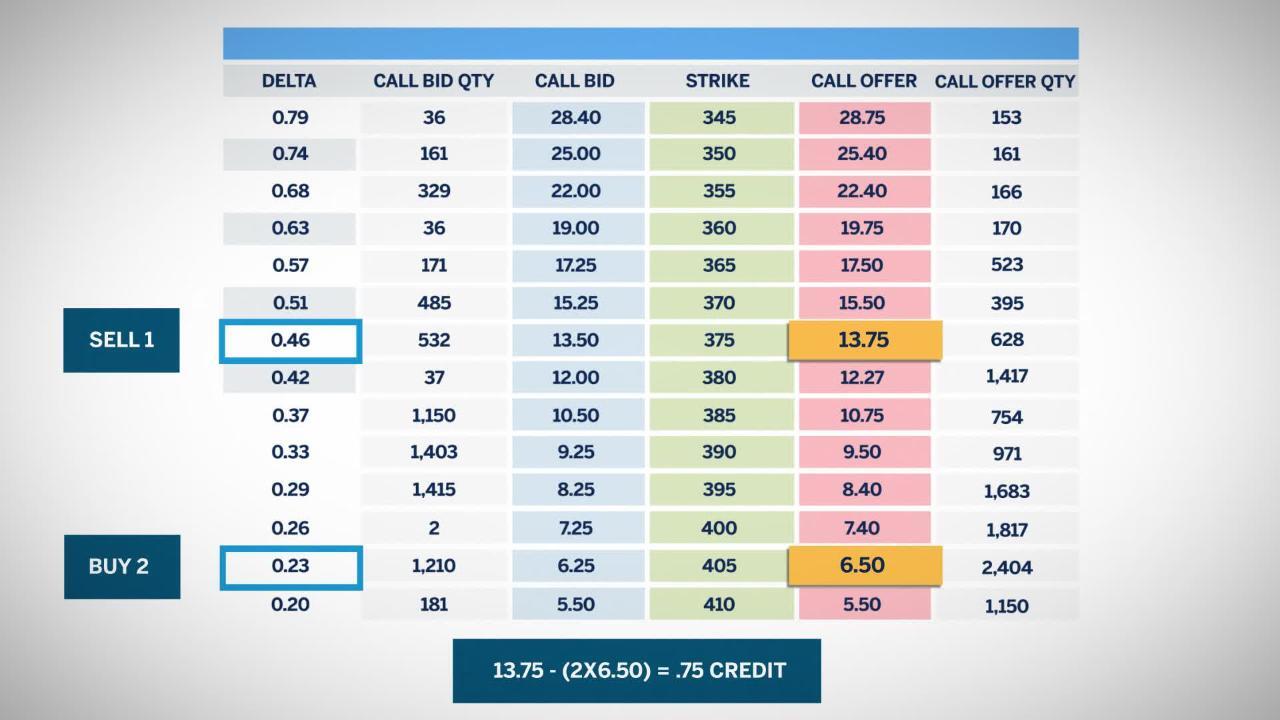

How the spreads are structured

These are not just random combinations of strikes. They are frequently a function of the deltas of the options in the spread. For example, a trader may want to buy upside exposure to the market. The trader will buy two of the 23 delta calls and sell one - 46 delta call to help finance the purchase.

The 375 strike has a 46 delta. The 405 strike has a 23 delta. The 405 option will need to be far enough in the money to overcome the loss from the 375 option. Therefore, the market will need to have a considerable upward move.

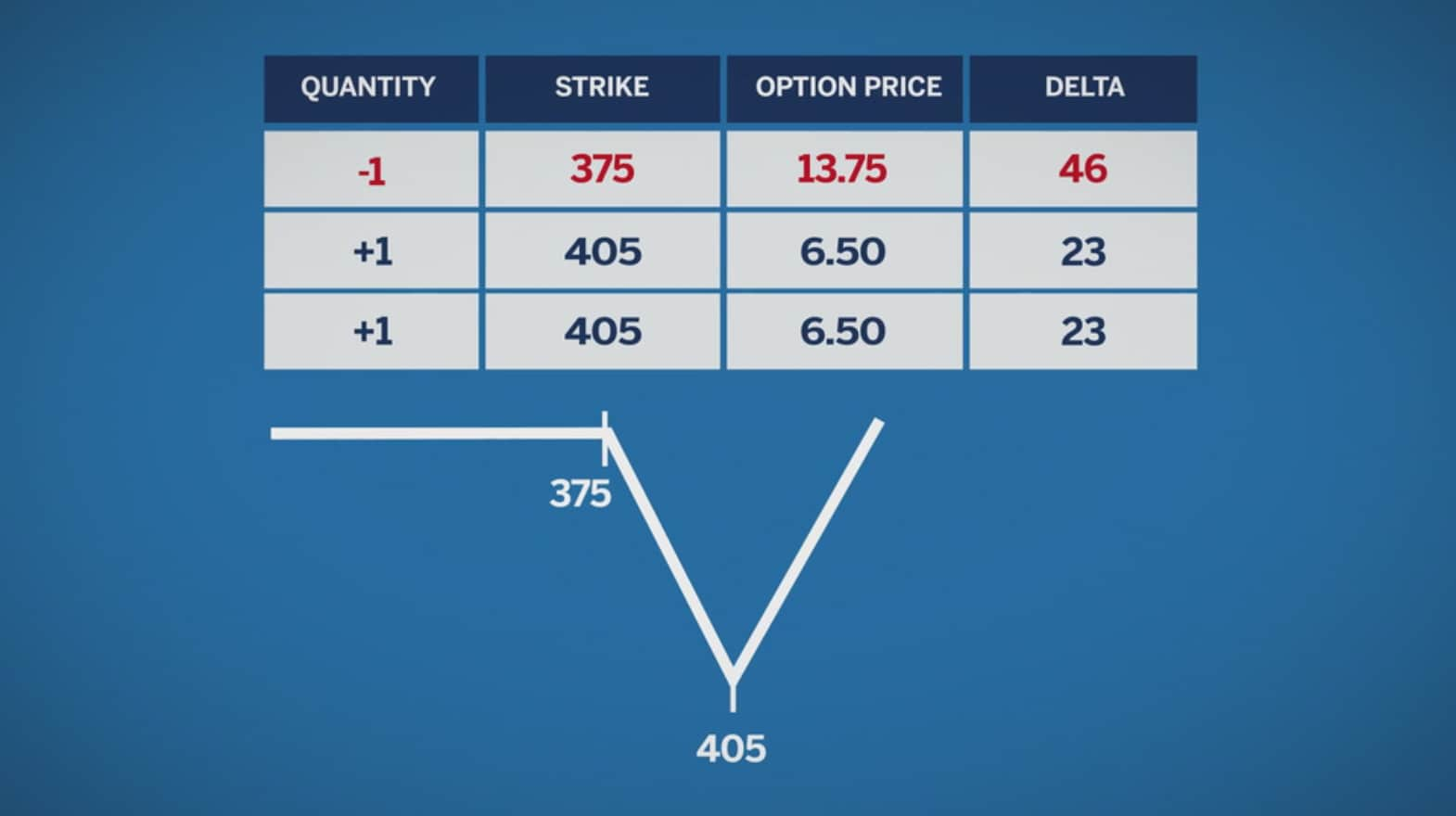

Examining the three instruments involved

Because this trade consists of three separate instruments, let’s look at each of them. Looking at te short 375 strike first, the payoff for that leg will look like a short call position.

Profit earning

Now let’s look at the 405 strike, these options both will have a long call payoff. The first 405 call that the traders bought will cap the loss on the 375 call that they sold.

As the market moves higher, any further losses incurred by the short 375 strike will be counterbalanced by gains on the 405 strike.

When we include the second 405 call, the payoff profile will look like this.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/option-ratio-spreads-01.jpg

{kind=link}

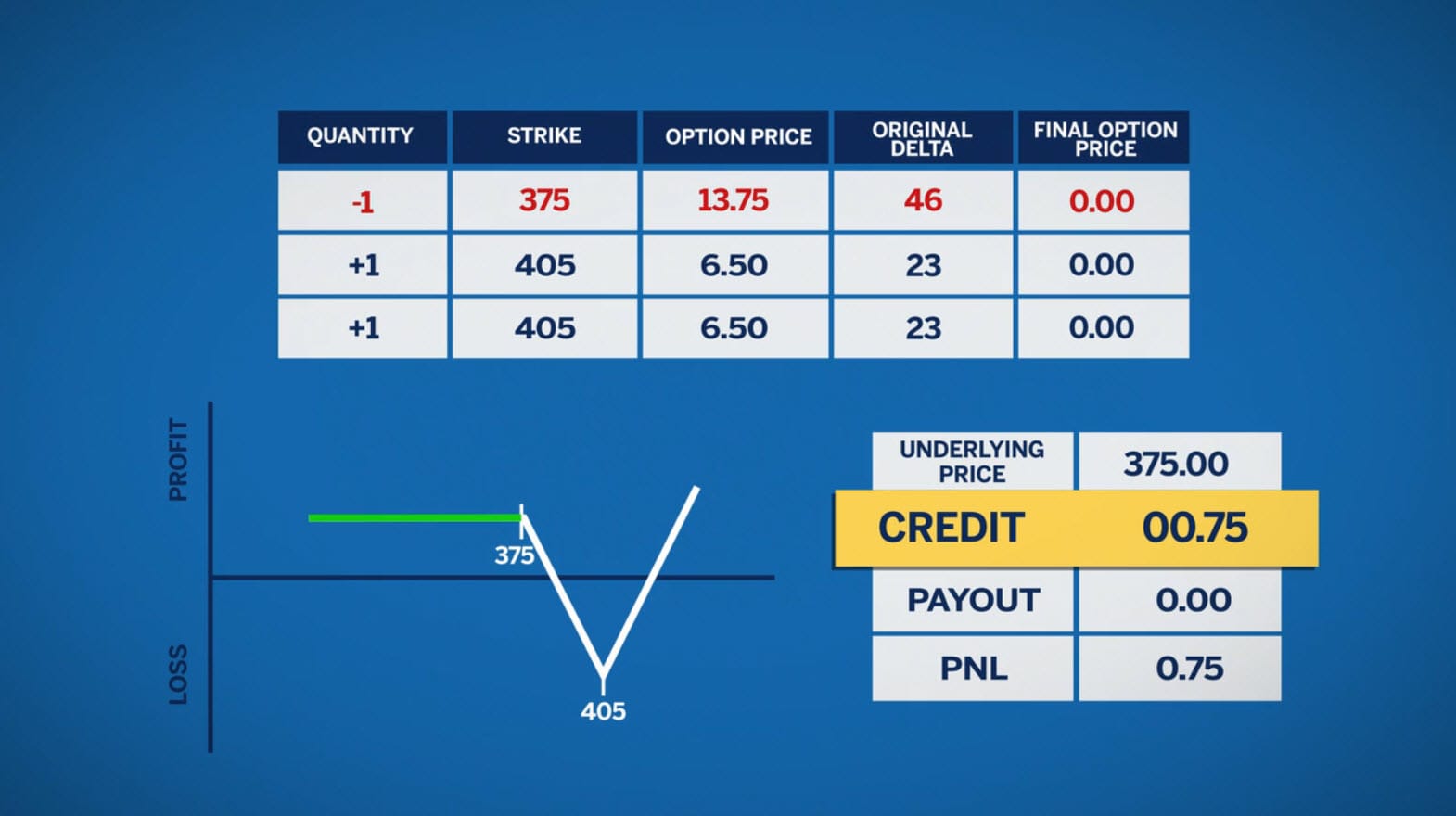

The trader receives a net credit of 0.75 for the ratio spread. Because he sold one option for 13 6/8, or 13.75, he bought two options for 6 4/8 or 6.50 each. Let’s look at this spread’s breakeven points.

If the market ends below 375, the trader will keep his .75 credit because all the options expire worthless.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/option-ratio-spreads-02.jpg

{kind=link}

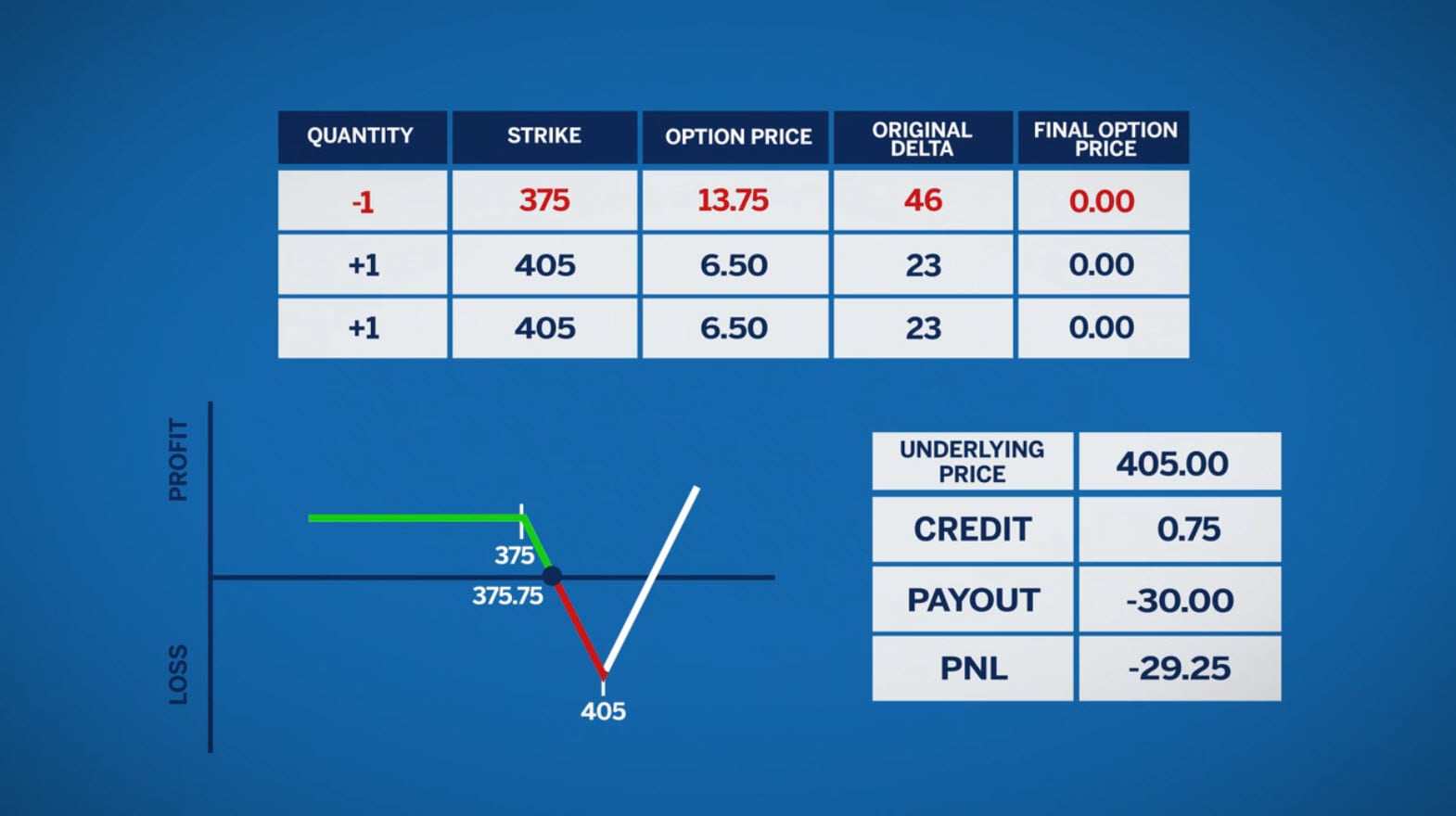

Loss reducing

If the market ends at 375.75, the payout he must make due to the short call’s being .75 in the money equals the credit he had received for the spread. This is the lower breakeven point.

If the market ends at 405, this is the point of his maximum loss: the 405 calls expire worthless, and he owes the market 30 for the short 375 call. If we subtract his original credit for the spread of .75, this lowers his loss to 29.25.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/option-ratio-spreads-03.jpg

{kind=link}

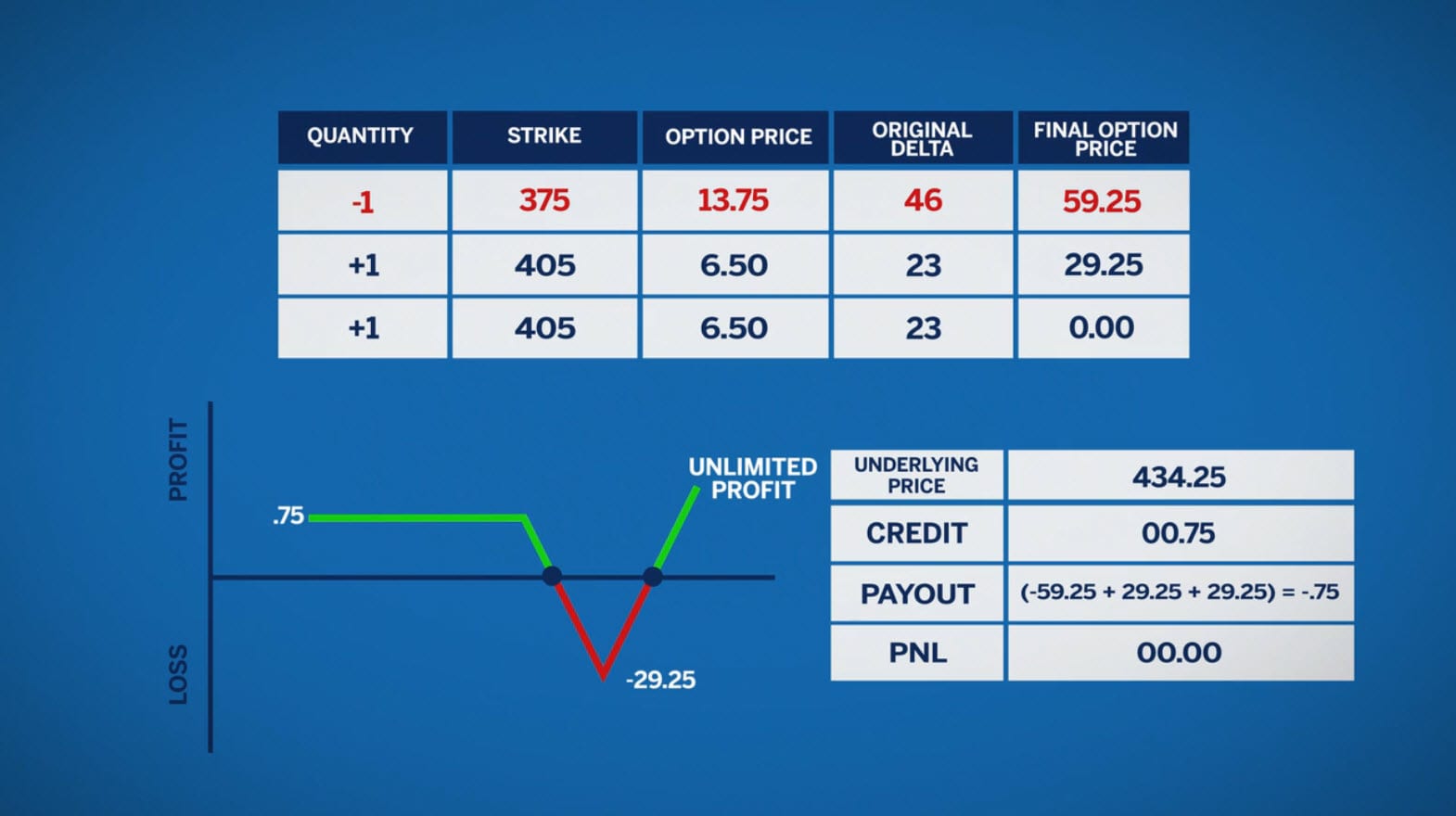

If the market ends above 405, both the 375 and 405 calls are in the money. Any further increases in the market that make the 375-call increase in value will also make the 405 call increase the same amount. Being short one and long the other, the trader is no longer affected by the upward market movement.

The second 405 call needs to overcome the max loss of 29.25 for the spread to be profitable.

Therefore, the market must reach 434.25 for our spread to reach its upper breakeven point. Anything above 434.25 is unlimited profit.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/option-ratio-spreads-04.jpg

{kind=link}

Conclusion

Ratio spreads can have multiple results based on market outcomes. Traders can express their view of the market with unlimited upside potential and limited downside exposure. Ratio spreads can be a capital efficient method for market participation.