Covered Calls

{kind=link}

Understanding Covered Calls

Before we look at the covered call strategy, remember that the writer, or seller, of an option is obligated to deliver the underlying futures contract to the buyer of the option when it is exercised. To cover the risk of a short call position, at any time prior to the options expiration, a trader can buy a futures contract to deliver to the call owner if the short call is exercised.

Owning the futures contract to deliver into the call means that the assignment risk is covered; hence the phrase covered call.

Selling a naked call, which means selling the call without owning the underlying instrument, exposes the option writer to unlimited losses if the market moves up. The maximum profit potential is the premium received for the call.

For example, if a trader sold the 100 call for $5, the breakeven point for the call would be the strike plus the premium. In this case 105.

Between 105 (the breakeven point) and 100 (the strike), the profit increases from zero to $5. At or below 100, the profit is the full amount of the premium, namely $5.

Covered Call Strategy.

The covered call strategy consists of a long futures contract and a short call on that futures contract. The call can be in-, at- or out-of-the-money. Generally, traders choose a call that is at-the-money to maximize the premium that is received from the sale of the call.

Covered calls are executed as an income-generating strategy when the futures contract holder expects the market to remain stable.

The trader foregoes some of the up-side potential of the futures position in return for the premium received from the sale of the call.

Example

It is the end of June and our trader is long a September futures contract. He believes that the market will be quiet and stable through July, after which he believes that the market will rally tremendously.

He could hold his September futures position until expiration. But instead, he attempts to generate income by selling a call option that expires before August. He sells the July 100 call for $5.

Since he already owns the underlying futures contract, his positions will be aggregated. This is the payoff profile for the long September futures contract.

He received $5 from the sale of the 100 call. So, the futures contract breakeven point is lowered by $5 dollars, to 95.

But because he sold the call, his up-side potential is capped. He forgoes profit if the underlying market is above 105.

The long September futures contract and short July call combined have a payoff profile as shown. His profit is capped at $5, from the sale of the call, through July expiration. This is because he needs to deliver the futures contract into the short call.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/covered-calls-01.jpg

{kind=link}

Scenarios

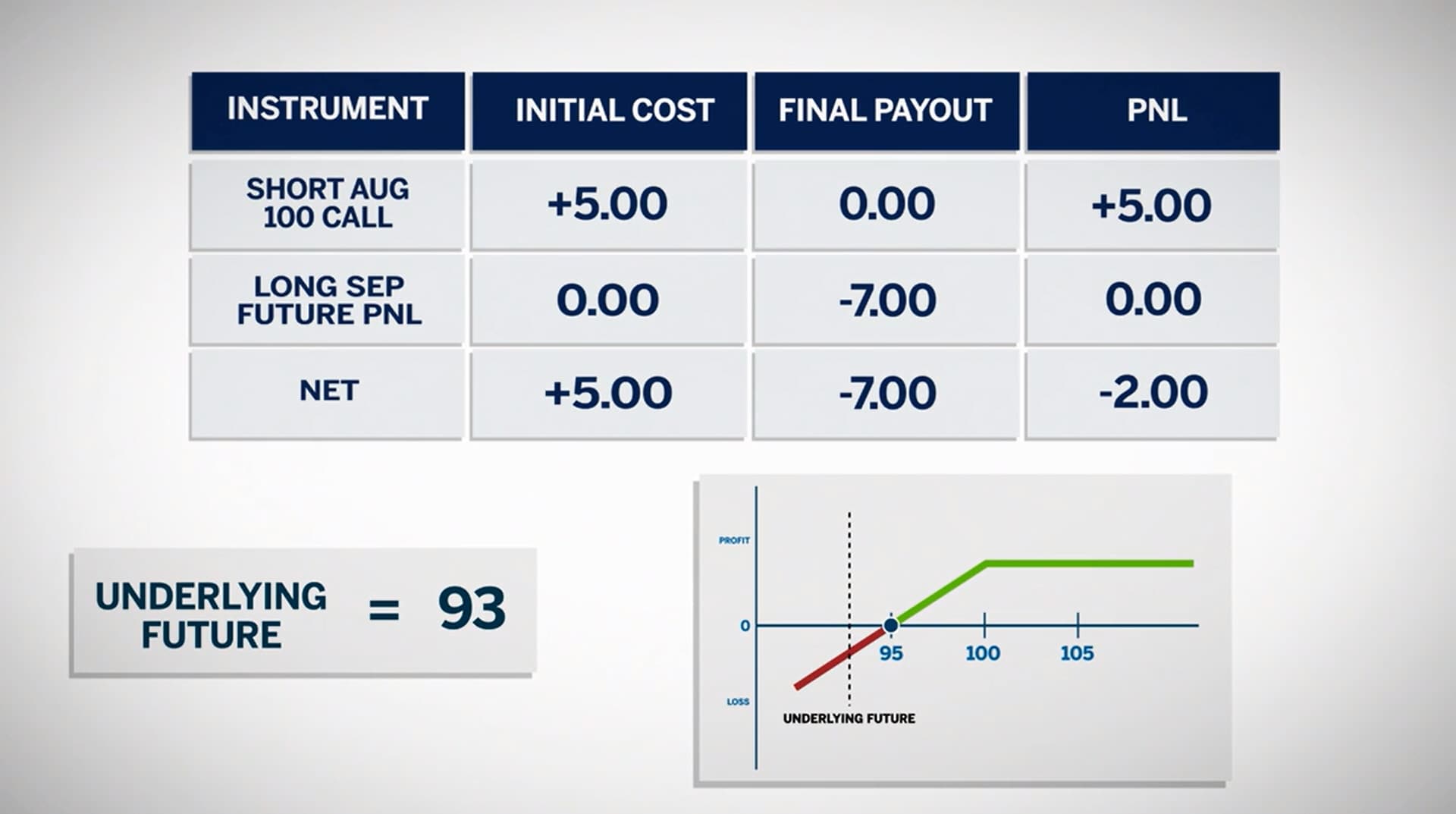

At July option expiration, if the September futures contract is at 93, his loss on this strategy would be two. The $7 of futures contract loss was mitigated by the $5 of premium from the call.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/covered-calls-02.jpg

{kind=link}

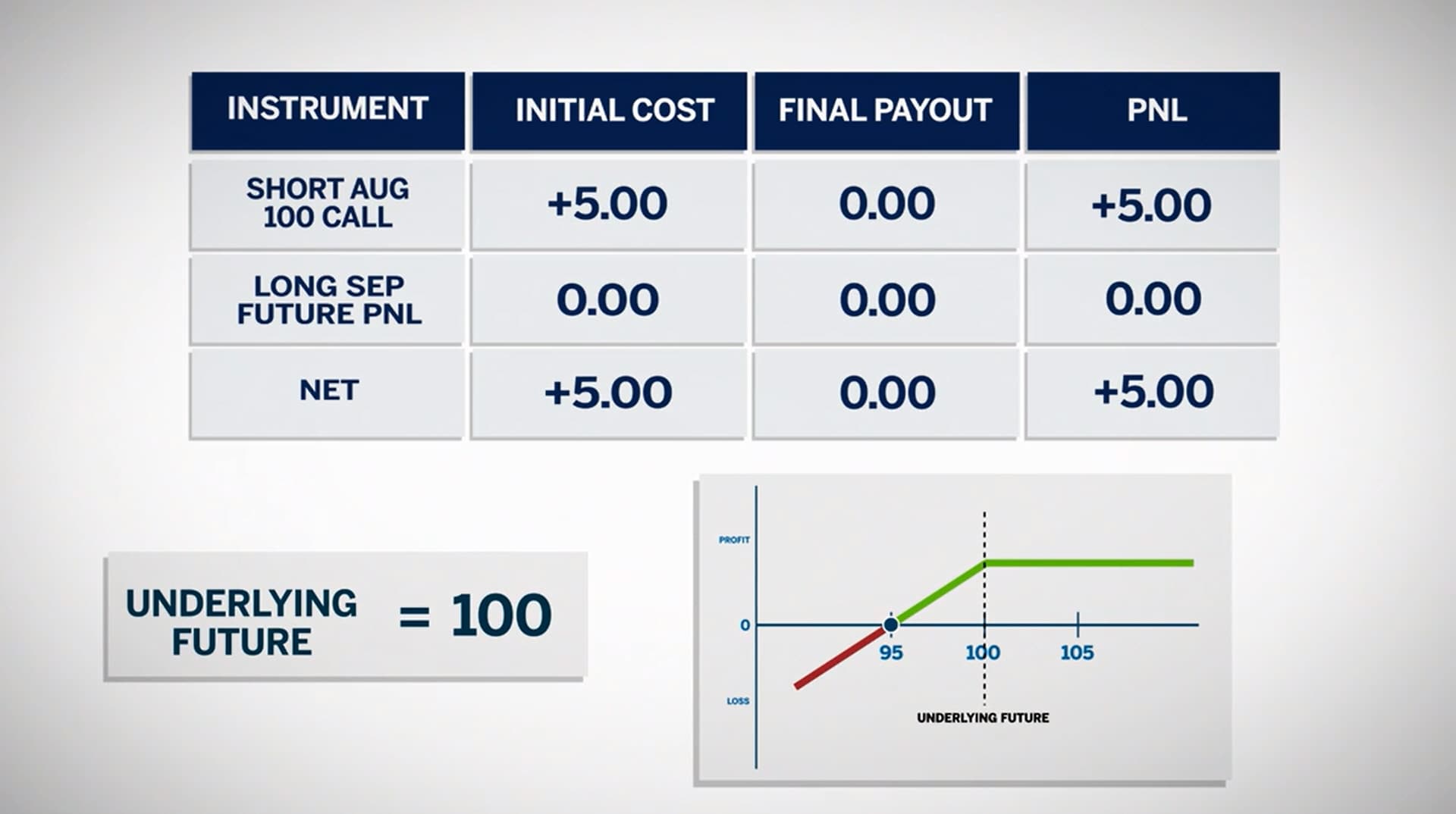

At July option expiration, with the September futures at 100, his profit will be $5 due to the futures PNL being zero and the call expiring worthless. This allows him to keep the full $5 of premium.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/covered-calls-03.jpg

{kind=link}

If the September futures contract was at 103, his profit would again be $5, $3 from the futures contract gain and $2 from the 100 call.

If the market had a tremendous rally earlier than he had anticipated, and the September futures rose to 120, his profit will remain $5, $20 from the futures contract minus $15 from the short call.

Conclusion

Covered calls are a commonly used and valuable options strategy providing income while lessening the sting of a downward market movement.