Bear Spread

{kind=link}

A bear spread consists of a buy leg and a sell leg of different strikes for the same expiration and same underlying contract. This strategy will pay off in a falling market, also known as a bear market, that is why it is referred to as a bear spread.

Bear spreads can be constructed from either going long a put spread or short a call spread.

Put Bear Spreads

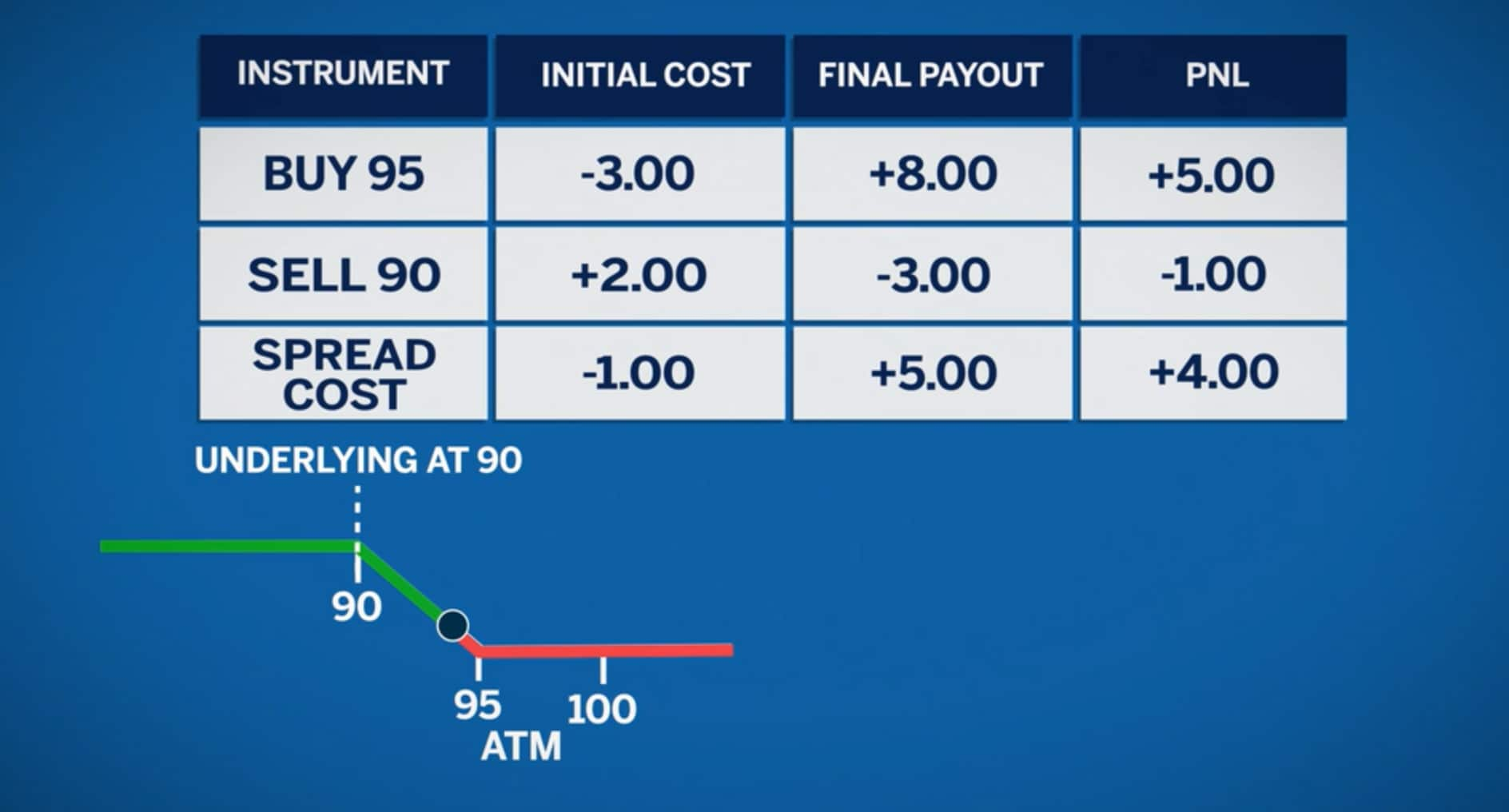

A trader believes that the market will have a moderate drop before the options expire. If the underlying market was trading at 100, he would buy a 95 put for $3 and sell the 90 put for $2.

By selling the 90 put, he receives a premium which offsets the cost of the 95 leg. The total cost of the spread is $1. The breakeven point for the spread is 94: the 95 strike minus the cost of the spread.

The best-case scenario is if the market finishes at or below 90. Because the 95-90 put spread will pay off $5. This is the maximum payoff for the spread, regardless where the underlying finishes. If we subtract the $1 cost of the spread, the total profit for the trade will be $4

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/bear-spread-01.jpg

{kind=link}

Assume the underlying finished at 87. The 95 put will pay the trader $8, but he will need to payout $3 on the 90 put. If the market finishes at 70, the 95 put will pay the trader $25, but he will need to payout $20 on the 90 put.

The worst-case scenario is if the market finishes at or above 95. Because both the 95 and 90 put expire out-of-the-money and are therefore worthless. So, the trader loses the full cost of the spread, $1. If the trader purchased only the 95 put at $3, his loss would be $3 versus $1.

If the underlying finishes at 92.5, the long 95 put will be worth $2.50 and the short 90 put expires worthless. The trader’s payout of $2.50 minus the $1 cost of the spread gives him $1.50 profit.

If the trader bought only the 95 put, his payout would still be $2.50, but that is less than the $3 he would have paid for the 95 put alone.

Call Bear Spreads

Selling a call is another way to be bearish on the market by allowing you to collect a premium that you keep if the underlying futures finish at or below the strike price.

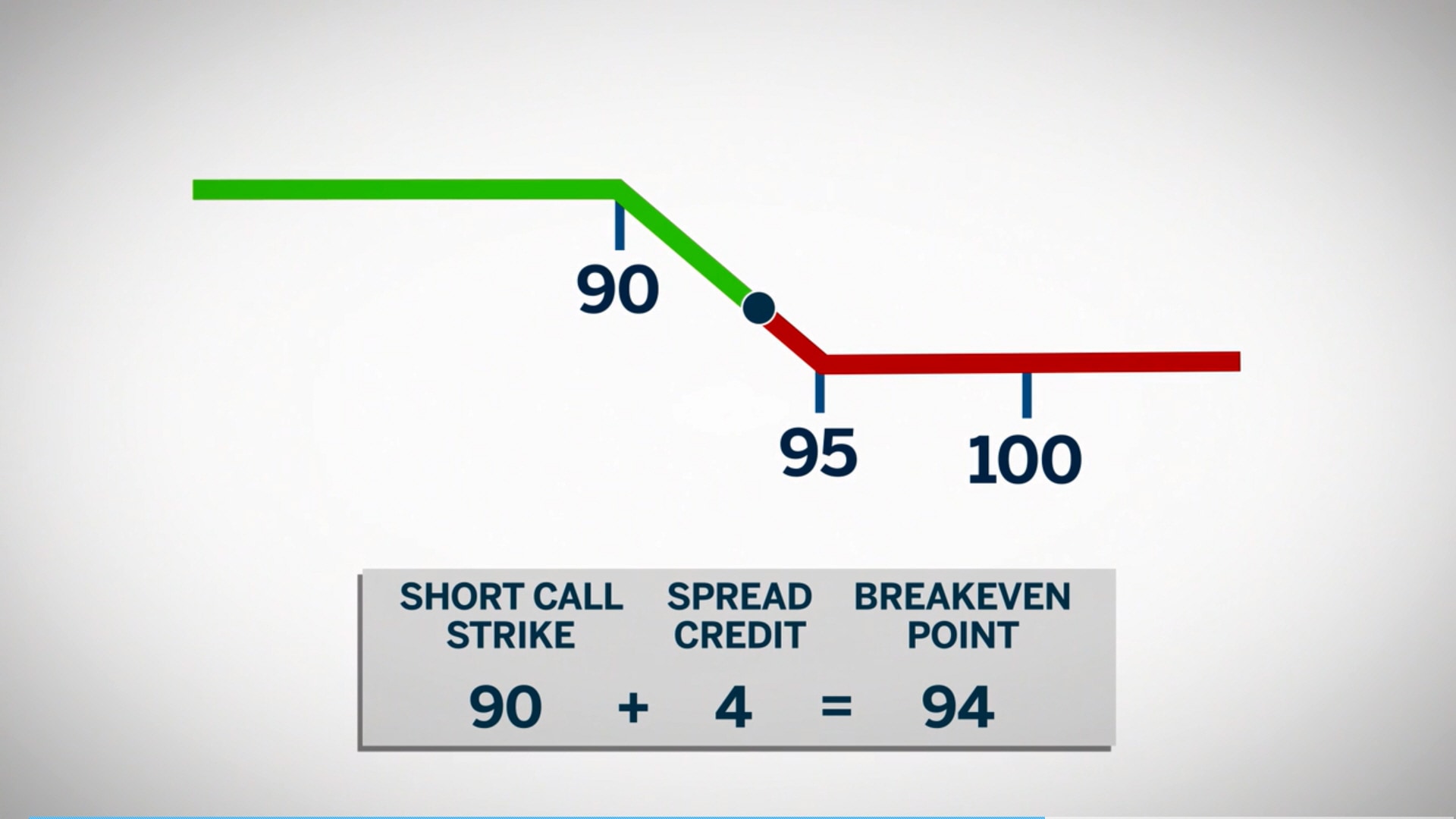

Instead of buying the 95-90 put spread, we can sell the 90-95 call spread. This would entail selling the 90 call and buying the 95 call, which would result in a $4 credit with the underlying future trading at 100.

The breakeven point for this spread is 94: the 90 strike plus the spread credit of $4. This is the same breakeven point as the put bear spread.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/bear-spread-02.jpg

{kind=link}

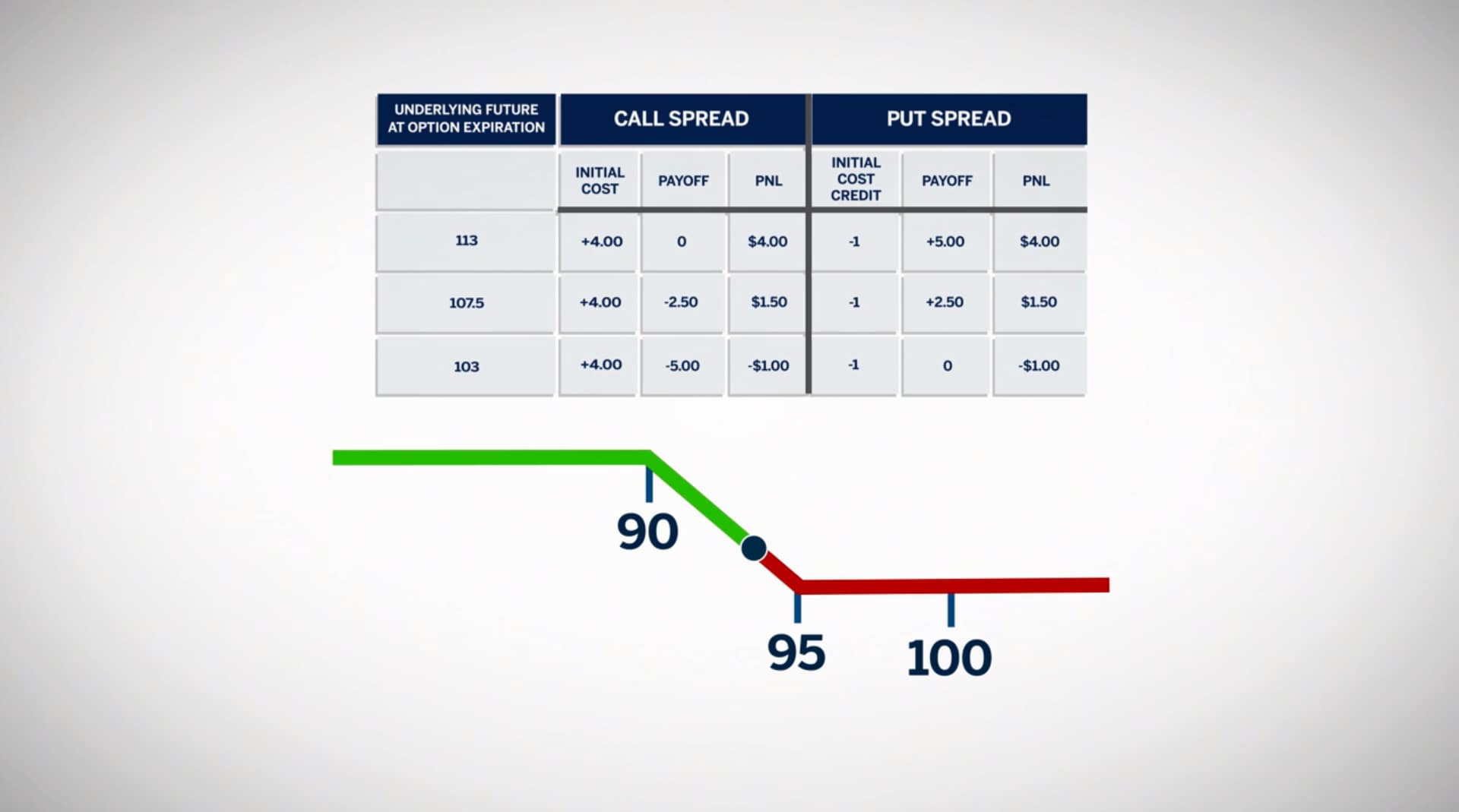

If the market finishes below 90, the calls expire worthless. Therefore, the trader keeps the $4 he received by selling the call spread.

If the market finishes at 97, the 90 call is worth $7 and the 95 call is worth $2 . Therefore, the call spread is worth $5 dollars. The trader received $4 and must now payout $5, resulting in a $1 loss.

If the market finishes at 92.5, the 90 call is worth $2.50. The 95 call expires worthless. So, the trader must pay out $2.50 from his $4 credit. Resulting in a $1.50 profit.

These scenarios have the same outcome whether we sell a call spread or buy a put spread to create a bearish position. Traders still want the market to below the high strike of the spread.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/bear-spread-03.jpg

{kind=link}