Nasdaq Veles California Water Index (NQH2O) futures product overview

{kind=link}

The Nasdaq Veles California Water Index futures contract is the first of its kind to help market participants manage financial exposure associated with the price risk of the largest and most dynamic water market in the US.

Contract specifications

Let’s review the details of the NQH2O futures contract from CME Group. The contract size is 10 acre feet. Assume the NQH2O Index is trading at $500.00 per acre foot, the notional value of one NQH2O futures contract would be $5,000. The tick size of the NQH2O futures contract is quoted in increments of one index point ‒ so a one tick move in the NQH2O futures is equivalent to $10 per contract. For calendar spreads, the tick size is reduced to 0.25 index points or $2.50 per contract.

At any time, eight consecutive quarterly contracts ‒ in the March quarterly cycle ‒ will be available to trade, plus the nearest two non-quarterly serial contracts.

{kind=link}

For example, in December, the January and February serial contracts would be available. When the January contract expires, the April contract is added. The extended listing cycle will provide market participants greater flexibility to manage risks related to reductions in water allocations and the unpredictability of California’s water supply.

An example

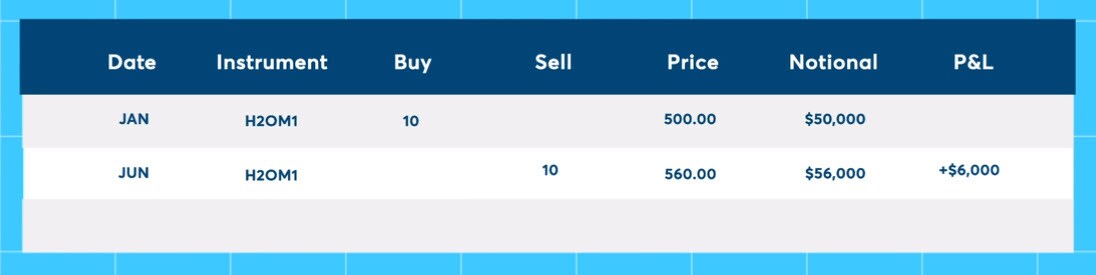

For instance, in January, a farmer forecasting a dry season estimates she needs to source an additional 100 acre feet of water to use in June and is concerned about rising water prices. The farmer sees that the spot market price for water delivered in June is $500 per acre foot and the June futures contract is also trading at $500 on CME Globex.

Anticipating higher water prices, the farmer decides to buy 10 June contracts at $500 per acre foot – thus covering the total amount of water she needs and protecting against the risk of a higher price for water in June. The notional value of the farmer’s futures position is $50,000.

However, she doesn’t need to pay the full amount and instead posts margin, which is a percentage of the notional value, to secure the position.

When the month of June arrives, the farmer aligns her spot/physical water purchase to the expiration date of the futures contract –in this case, the third Wednesday in June.

Assume, at this time, the spot price of water has increased to $560 per acre foot. Since the last day to trade the contract is the business day prior to final settlement, she closes her futures position on Tuesday by selling her NQH2O contracts at a price of $560 per contract and purchases her water in the spot market.

{kind=link}

If you recall, the farmer purchased the futures contracts at $500 per acre foot and later sold them at a price of $560 per acre foot. The $60, per acre foot, profit made from the sale of the futures contracts offset the increased price of purchasing water in the spot market, which also went up by $60. Netting the futures profit with the spot purchase price makes the farmer’s effective price paid for water $500 per acre foot.

By hedging with NQH2O futures, the farmer was able to successfully protect against the risk of rising prices. Please note, the prior example assumed a basis or difference between the cash price and the futures price of zero. There may be a basis between the two prices depending on the source of the water, location, and conveyance costs, as well as other factors.

NQH2O futures will be available to trade on CME Globex Sunday afternoon through Friday afternoon, nearly 24 hours per day, and will be block eligible.

The contract provides actionable price discovery and transparency ‒ allowing market participants the ability to efficiently manage the price risk associated with water’s scarcity.