Energy Market and Risk Management with Options

{kind=link}

Managing Risk in the Energy Market

Like other commodities with wholesale markets, the electricity wholesale market is where electricity is frequently bought and then resold before it ever reaches the end customer. Wholesale participants in this market may not always own resources that generate power and they may not always directly serve the end users.

Three major types of participants engaging in the resale markets include:

- Electricity utility companies

- Independent power producers

- And Electricity marketers

In addition to directly buying or selling in the spot market, companies can also engage in bilateral transactions through negotiation, using a brokerage platform, or through a futures exchange. The transaction could be either a standardized contract like futures or they could be customized, like complex contracts known as structured transactions. In between the wholesale market and the end-customer are the Load Serving Entities (LSE). An LSE can either procure electricity in the wholesale market or they may own their own electricity generation resources.

{kind=link}

Options Hedging Example

Assume it is March and the nuclear plant economist has a positive short-term outlook for PJM regional electricity spot price during peak hours for the month of May. The nuclear plant operation costs are $20 dollars per MWh.

Plant’s Goal:

- Maximize profit

- Eliminate downside risk to fund operations at $20 per MWh

How could the economist take advantage of the potential for a short-term price increase and protect their downside price risk to ensure they have enough funds to maintain continuous operations?

The economist has two options:

- Negotiate a private deal (costly, time consuming,)

- Hedge using options on futures (more flexibility, lower costs)

Assume the May average forward price for PJM Western Hub is around $35 dollars per megawatt hour. Given its 1000 MWh capacity and 80% utilization rate in peak hours, this plant needs to sell around 800 MWh for each peak hour during the month of May.

How many contracts would be need to hedge the 800 MWh?

CME Group PJM Western Hub Real-Time Peak Calendar-Month 50 MWh Options Contract (ticker symbol PMA)

800 MWh / 50 MWh = 16 contracts (per day)

16 contracts * 20 days = 320 total contracts

The most straightforward approach for this plant to manage its position, is to sell their generation on the spot market while also going long a May PMA Out-of-the-Money Put, with a $21 strike price.

Strategy:

- Sell output at spot physical market

- Long OTM Put option at strike $21 per MWh for all peak hours in May

Assuming the current May average forward price for PJM Western Hub is around $35 per MWh, the out-of-the-money put option might only cost $0.3 per MWh to execute.

| Scenario 1 Payoff | Scenario 2 Payoff | |

| Spot Market in May | $40 per MWh | $17 per MWh |

| 320 PMA Put Option @ $21 strike per MWh |

$0.3 per MWh Put Premium Paid (Option expired worthless) |

$0.3 per MWh Put Premium Paid $21-$17=$4 per MWh profit (Option was in-the-money) |

| Net Revenue | $40 - $0.3=$39.70 per MWh | $17+$4 - $0.3= $20.7 per MWh |

Futures Hedging Example

Assume it is January, and a utility has a contract to serve their clients in the PJM Western Hub region, for 100 MWh for all the peak hours in the month of June.

How could the utility hedge their price risk in June?

The Utility has three options to hedge their risk:

- PJM Spot Market

- Bilateral customized transaction

- Exchange traded futures

Spot Market

The utility has the option to wait until June to buy electricity from the day-ahead, or real-time, Spot market, which is operated and cleared through the ISO. If they do this, they will be exposed to the price risk between January and June.

Bilateral Agreement

They also have the option to negotiate a bilateral contract with other firms in the wholesale market. But it usually takes time and counterparty risk assessment to be able to execute a customized transaction. Depending on the negotiation, the price this company could get might not be competitive as it is not a market price.

Exchange-Traded Futures

The utility decides to use standardized electricity futures from a futures exchange to hedge its price risk, as it offers the necessary liquidity to meet their needs while eliminating the counterparty risk.

To hedge their risk, the utility uses the PJM Western Hub Peak Calendar-Month Real-Time LMP Futures (L1) provided by CME Group.

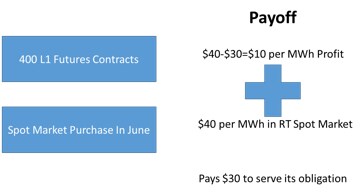

Assume there are 20 days of peak days in the month of June, and the futures contract (L1) has a size of 80 MWh. For 100 MW for all the peak hours, this LSE is obligated to 100 MW * 16 peak hours * 20 days = 32,000 MWh. To hedge its price exposure, it buys 400 contracts of L1 June futures at the price of $30 per MWh.

When June comes, the utility buys electricity from the real-time spot market to serve its customers for 100 MW per hour during peak hours.

By the end of June, we might assume the average price of all the peak hours in PJM Western Hub is $40 MWh. Since they bought 400 contracts of L1 June Futures, the profit from the financial futures position will offset the cost from buying in the spot market.

In the end, this utility only pays $30 MWh to serve its customers while the spot market is at $40 MWh. By hedging their price risk using electricity futures, they saved $10 MWh, which equates to $320,000 overall.

{kind=link}