Put-Call Parity

{kind=link}

Individuals trading options should familiarize themselves with a common options principle, known as put-call parity.

Put-call parity defines the relationship between calls, puts and the underlying futures contract.

This principle requires that the puts and calls are the same strike, same expiration and have the same underlying futures contract. The put call relationship is highly correlated, so if put call parity is violated, an arbitrage opportunity exists.

The formula for put call parity is c + k = f +p, meaning the call price plus the strike price of both options is equal to the futures price plus the put price.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/put-call-parity-fig01.jpg

{kind=link}

Using algebraic manipulation, this formula can be rewritten as futures price minus call price plus put price minus strike price is equal to zero f - c + p – k = 0. If this is not the case, an arbitrage opportunity exists.

For example, if the futures price is 100 minus the call price of 5, plus the put price of 10 minus the 105 strike equals zero.

Say the futures increase to 103 and the call goes up to 6. The put price must go down to 8.

Now say the future increases to 105 and the call price increases to 7. The put price must go down to 7.

As we originally said, if futures are at 100, the call price is 5 and the put price is 10. If the futures fall to 97.5, the call price is 3.5, the put price goes to 11.

If a put or call does not adjust in accordance with the other variables in the put-call parity formula, an arbitrage opportunity exists. Consider a 105 call priced at 2, the underlying future is at 100 so the put price should be 7.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/put-call-parity-fig02.jpg

{kind=link}

If you could sell the put at 8 and simultaneously buy the call for 2, along with selling the futures contract at 100, you could benefit from the lack of parity between the put, call and future.

Market Outcomes

Look at different market outcomes demonstrating that this position allows individuals to profit by arbitrage regardless of where the underlying market finishes.

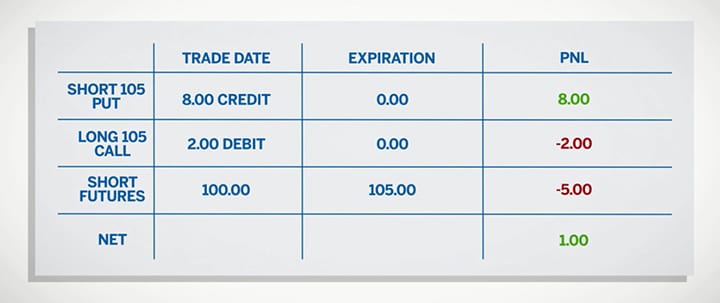

The futures price finished below 105 at expiration. Our short 105 put is now in-the-money and will be exercised, which means we are obligated to buy a futures contract at 105 from the put owner.

When this trade was executed, we shorted a futures contract at 100, therefore our futures loss is $5, given the fact that we bought at 105 and sold at 100. This loss is mitigated by the $8 we received upon the sale of the put. The put owner forfeited the $8 when he exercised his option.

Our long 105 call expires worthless, so we forfeit the $2 call premium. This brings our net profit to $1 with the loss of $5 from the futures and loss of $2 from the call and the gain of $8 from the put.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/put-call-parity-fig03.jpg

{kind=link}

Another scenario, the futures price finished above 105 at expiration. Our long 105 call is now in-the-money allowing us to exercise the call and buy a futures contract at 105. Because we exercised the option, our $2 premium is forfeited.

When this trade was executed, we shorted a future at 100, therefore our futures loss is $5. The $8 we received from the sale of the put is now profit because it expired worthless. If you add up the $8 gain from the put, less the $5 loss from the futures and $2 loss from the call you would net a profit of $1.

If the futures end exactly at 105, both options expire worthless. We lose $5 on the futures and make net $6 in options premium, therefore, we net $1.

We stated earlier that put-call parity would require the put to be priced at 7. We have now seen that a put price of 8 created an arbitrage opportunity that generated a profit of $1 regardless of the market outcome.

Put-call parity keeps the prices of calls, puts and futures consistent with one another. Thus, improving market efficiency for trading participants.