Understanding Natural Gas Risk Management Spreads & Storage

{kind=link}

Managing Natural Gas Risk

Calendar spread risk management is one of the key issues in trading natural gas in North America.

Seasons

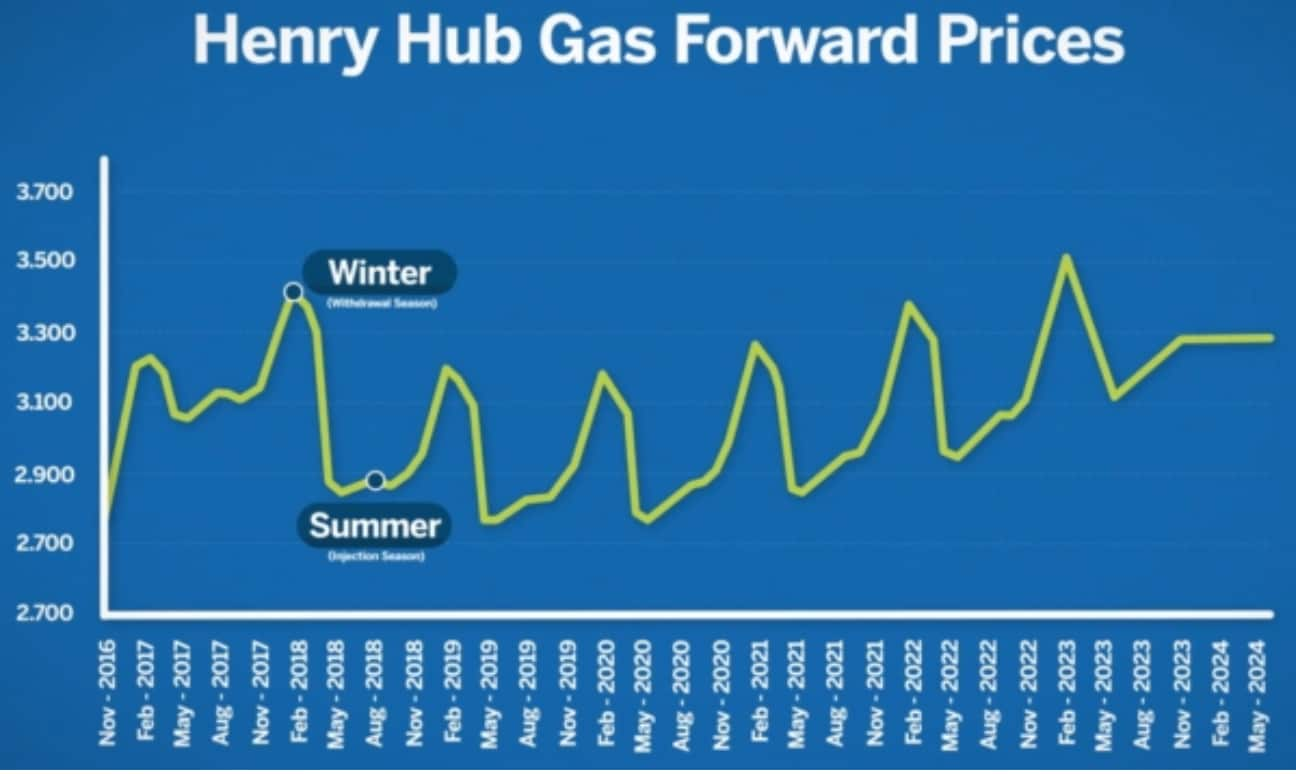

Natural gas prices show clear seasonality broken into two main seasons: winter, or withdrawal season, and summer, injection season. Winter in the United States generally ranges from November to March; summer is from April to October. During the summer season, gas demand decreases while production continues, resulting in excess natural gas that can be stored. During the winter season, gas consumption peaks as a result of increased heating demand from residential end-users, the industrial sector and utilities. As a result of unpredictable winter demand, winter natural gas futures generally trade at a premium to the summer futures.

Two examples of natural gas calendar spreads could be a summer-winter spread using the averages of the summer and winter months and a March-April spread, when winter demand slows and moves into the summer injection season. Natural gas storage facilities offer physical optionality to balance supply and demand in the gas market. Natural gas providers have the option to inject excessive gas production into underground storage facilities.

{kind=link}

Example One

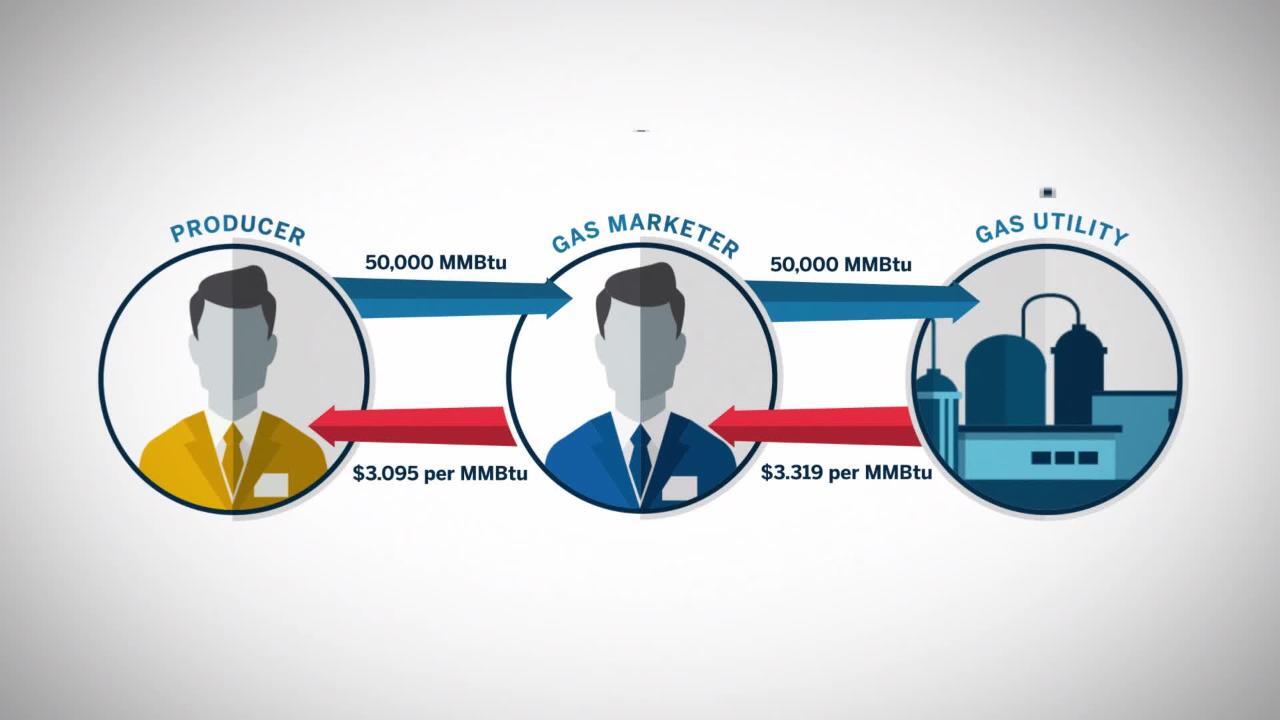

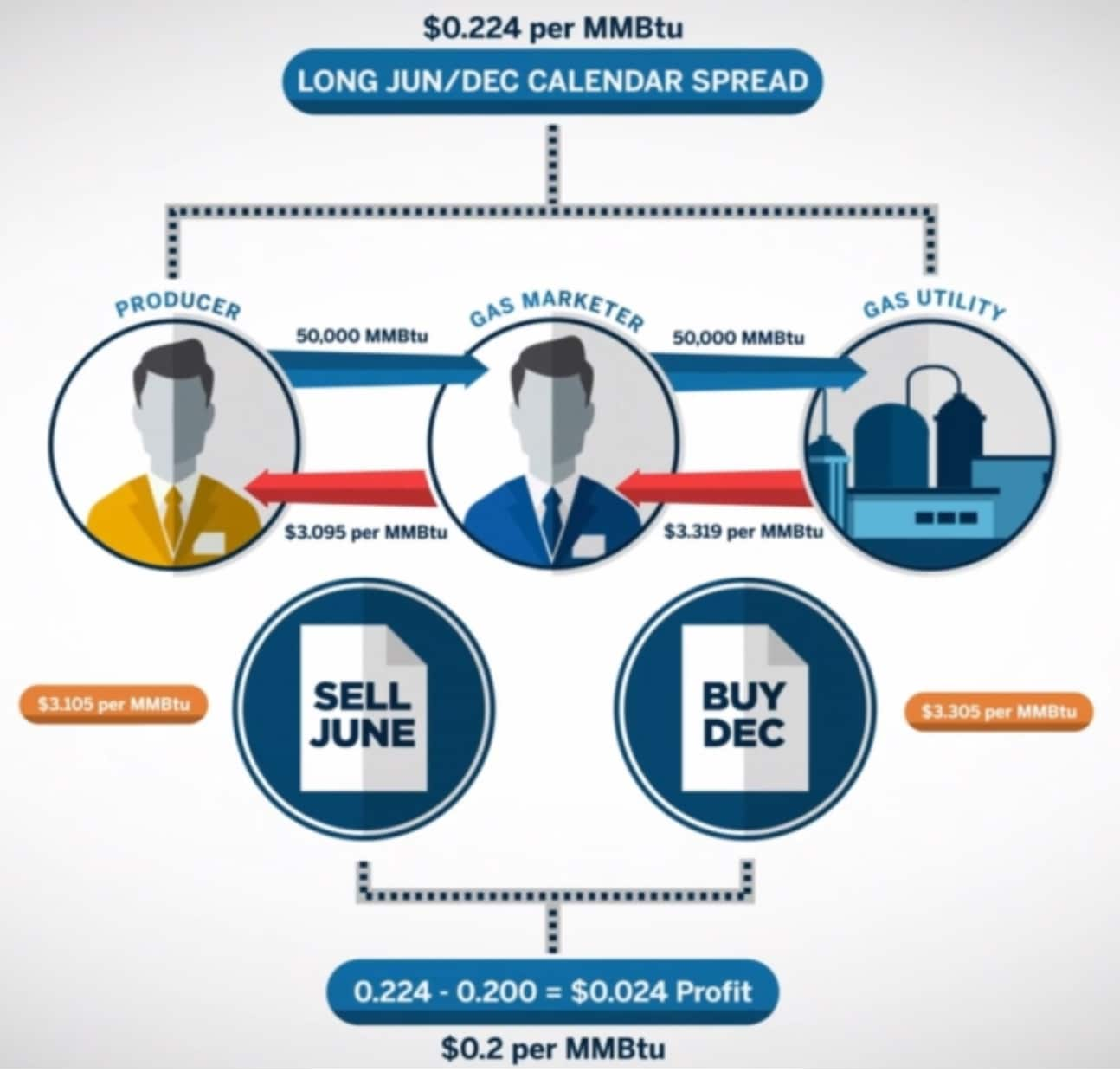

A gas marketer has entered into a contract to sell to a gas utility firm 50,000 MMBtu for December delivery at Henry Hub, Louisiana for a fixed price $3.319 per MMBtu. This marketer decides to hedge his physical volume risk so he buys 50,000 MMBtu from a producer for June delivery at Henry Hub for a fixed price of $3.095 per MMBtu. Essentially, this marketer has bought the June and December calendar spread for $0.224 per MMBtu with long June Natural Gas and short December Natural Gas at Henry Hub.

One approach to balance his price risk is to use a storage facility as a way to move forward his June long position. The marketer injects 50,000 MMBtu gas into the underground storage in June and withdrawals it in December for the sale position with overall storage cost of $0.12 per MMBtu and overall financing cost of $0.10 per MMBtu. As a result, this marketer makes $0.004 per MMBtu after the storage and financing costs.

{kind=link}

Example Two

Another alternative approach would be using financial instruments to hedge the calendar spread risk. The marketer sells 50,000 MMBtu or five Henry Hub June futures contracts and buys 50,000 MMBtu or five Henry Hub December futures contracts. With June futures priced at $3.105 and December futures priced at $3.305, this marketer effectively sold the June-December calendar spread for $0.2. Overall this marketer is able to unwind his positions and make $0.224-$0.2=$0.024 profit with financial instruments.

{kind=link}

Summary

Calendar spread risk management is a key issue for some participants in the Natural Gas market. We have just demonstrated one way futures could be utilized to manage that risk.