About Contract Notional Value

{kind=link}

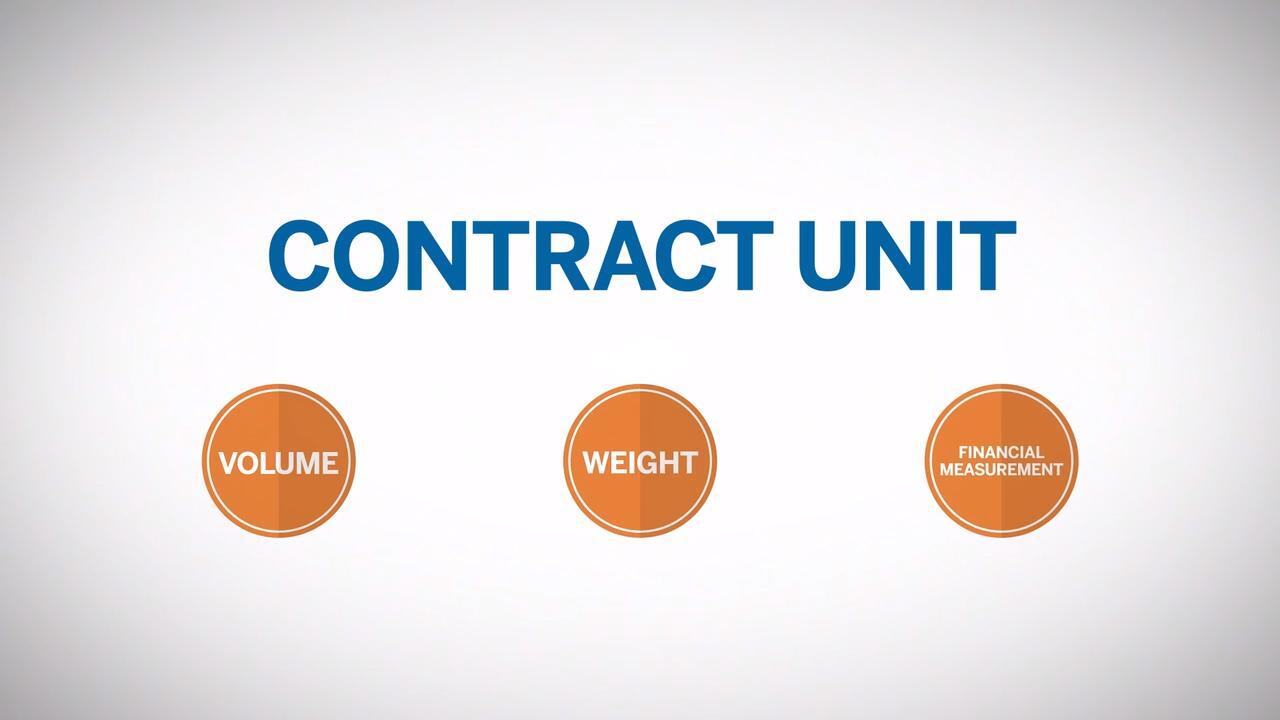

Contract Unit

The contract unit is a standardized size unique to each futures contract and can be based on volume, weight, or a financial measurement, depending on the contract and the underlying product or market.

For example, a single COMEX Gold contract unit (GC) is 100 troy ounces, which is measured by weight.

A NYMEX WTI Crude Oil contract unit (CL) is 1,000 barrels of oil, measured by volume.

The E-mini S&P 500 contract unit (ES) is a financial calculation based on a fixed multiplier times the S&P 500 Index.

Contract Notional Value

Contract notional value, also known as contract value, is the financial expression of the contract unit and the current futures contract price.

Determining Notional Value

Assume a Gold futures contract is trading at price of $1,000. The notional value of the contract is calculated by multiplying the contract unit by the futures price.

Contract unit x contract price = notional value

100 (troy ounces) x $1,000 = $100,000

If WTI Crude Oil is trading at $50 dollars and the contract unit is 1000 barrels, the notional would be;

$50 x 1,000 = $50,000

Now assume E-mini S&P 500 futures are trading at 2120.00. The multiplier for this contract is $50.

$50 x 2120.00 = $106,000

The Importance of Contract Unit and Notional Value

Notional values can be used to calculate hedge ratios versus other futures contracts or another risk position in a related underlying market.

Hedge Ratio

How might a portfolio manager, with a $10M U.S. equity market exposure, use notional value of E-mini S&P 500 futures to determine a hedge ratio?

Hedge ratio = value at risk/notional value

We can determine the hedge ratio using our previous example of the E-mini S&P 500 futures with a value of $106,000.

Hedge ratio = 10,000,000/106,000

Hedge ratio= 94.33 (approximately 94 contracts)

If the portfolio manager sells 94 E-mini S&P 500 futures against her long equity cash position, she has effectively hedged her market risk.