What is Contango and Backwardation

{kind=link}

Contango and backwardation are terms used to define the structure of the forward curve. When a market is in contango, the forward price of a futures contract is higher than the spot price. Conversely, when a market is in backwardation, the forward price of the futures contract is lower than the spot price.

Contango

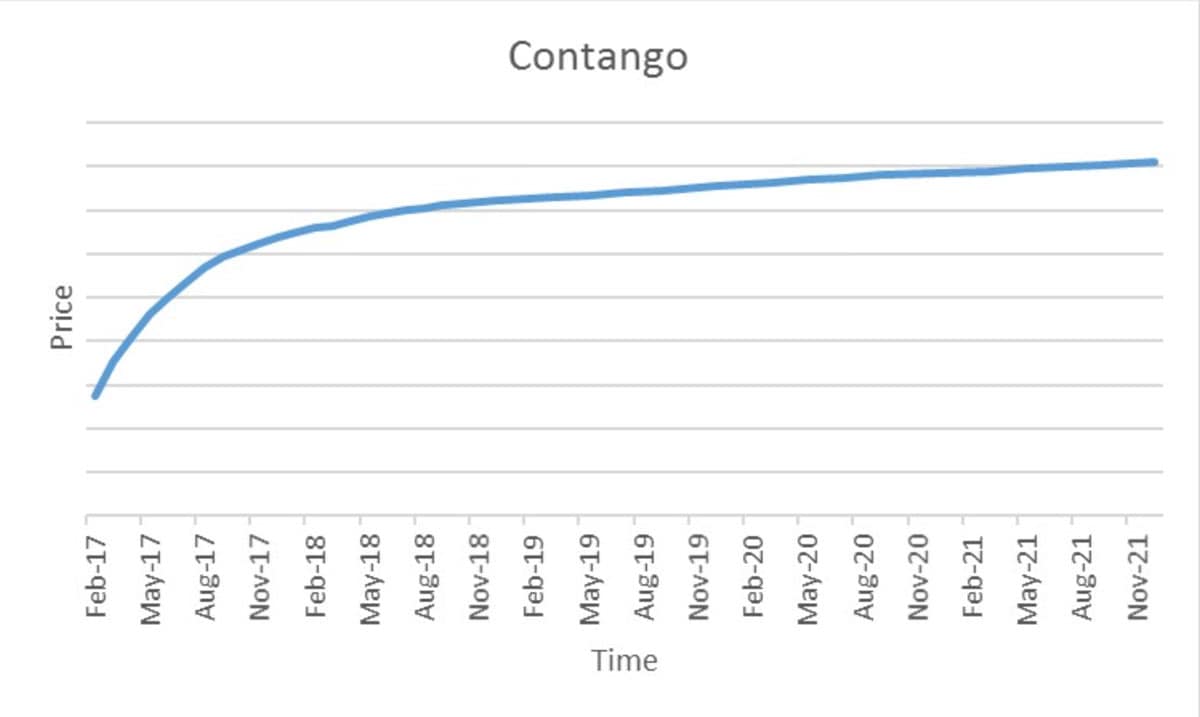

In the chart below, the spot price is lower than the futures price which has generated an upward sloping forward curve. This market is in contango - the futures contracts are trading at a premium to the spot price. Physically delivered futures contracts may be in a contango because of fundamental factors like storage, financing (cost to carry) and insurance costs. The futures prices can change over time as market participants change their views of the future expected spot price; so the forward curve changes and may move from contango to backwardation.

{kind=link}

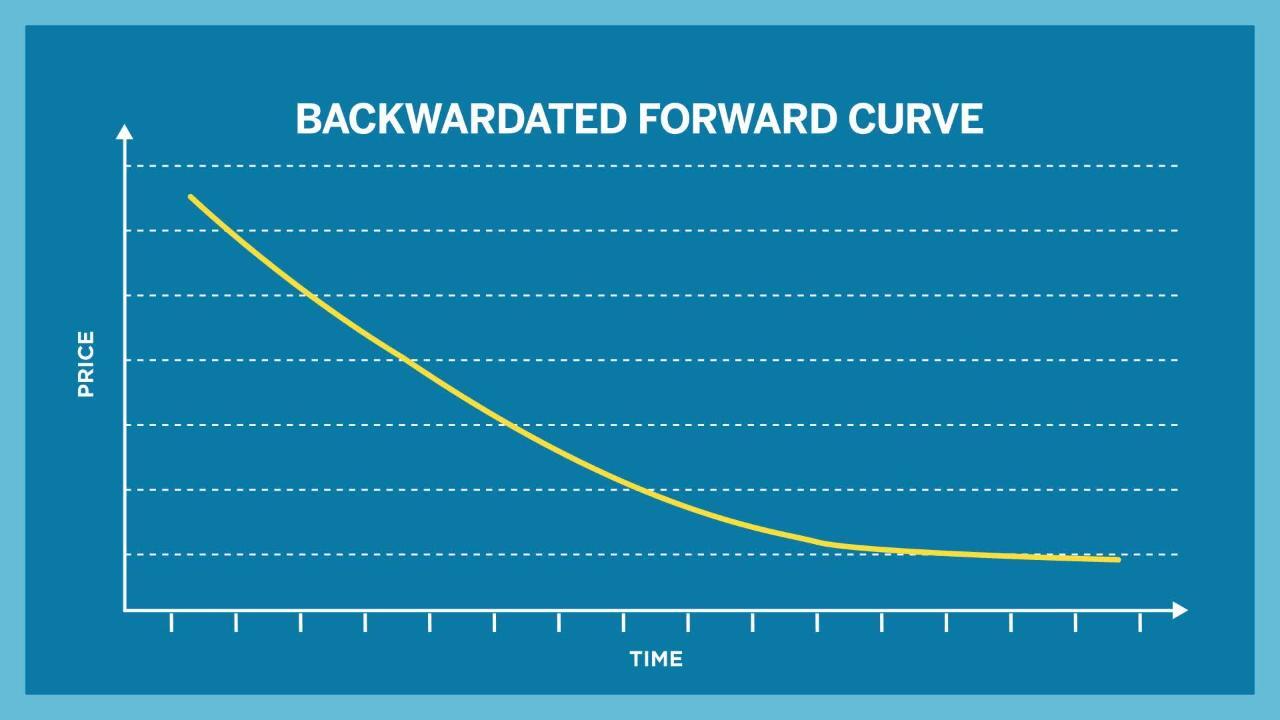

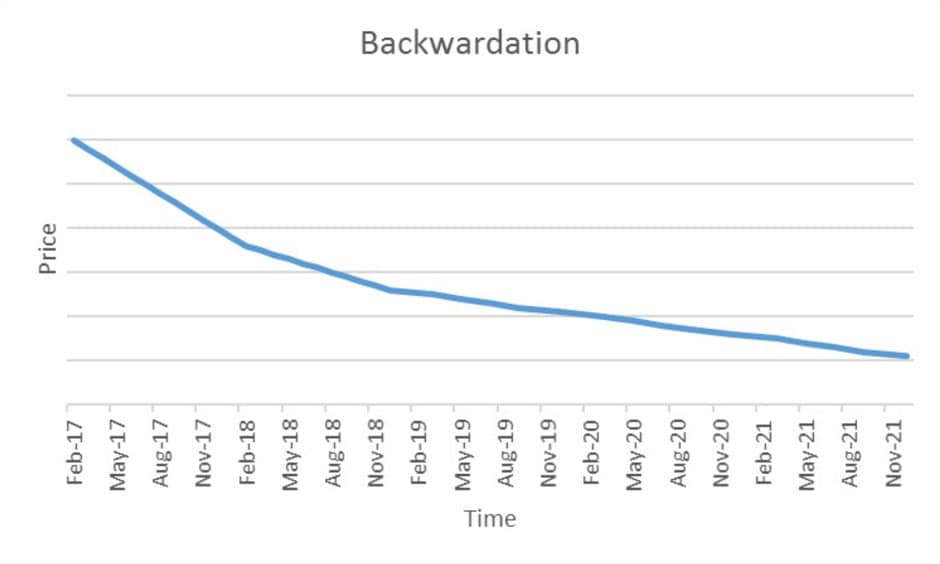

Backwardation

In the chart below, the spot price is higher than future prices and has generated a downward sloping forward, or inverted, curve which is in backwardation. The futures forward curve may become backwardated in physically-delivered contracts because there may be a benefit to owning the physical material, such as keeping a production process running. This is known as the convenience yield, which is an implied return on warehouse inventory. The convenience yield is inversely related to inventory levels. When warehouse stocks are high, the convenience yield is low and when stocks are low, the yield is high.

{kind=link}

Convergence

Over time, as the futures contract approaches maturity, the futures price will converge with the spot price, otherwise an arbitrage opportunity would exist.