Trading €STR futures

{kind=link}

CME Group offers two contracts based on the €STR benchmark rate to help with price discovery along the European money market curve: the Outright Three-Month €STR future (ESR) and the Three-Month €STR-Euribor Single Contract Basis spread futures (EUS).

Outright Three-Month €STR futures trade in IMM Index points:

IMM Index = 100 - (compounded daily €STR rate over the reference period)

Like other short-term interest rate contracts offered by CME Group, the contract size is defined by the dollar value of a one basis point move. For €STR futures, one index point is equal to one percent and is worth €2,500 per contract, which amounts to €25 per basis point.

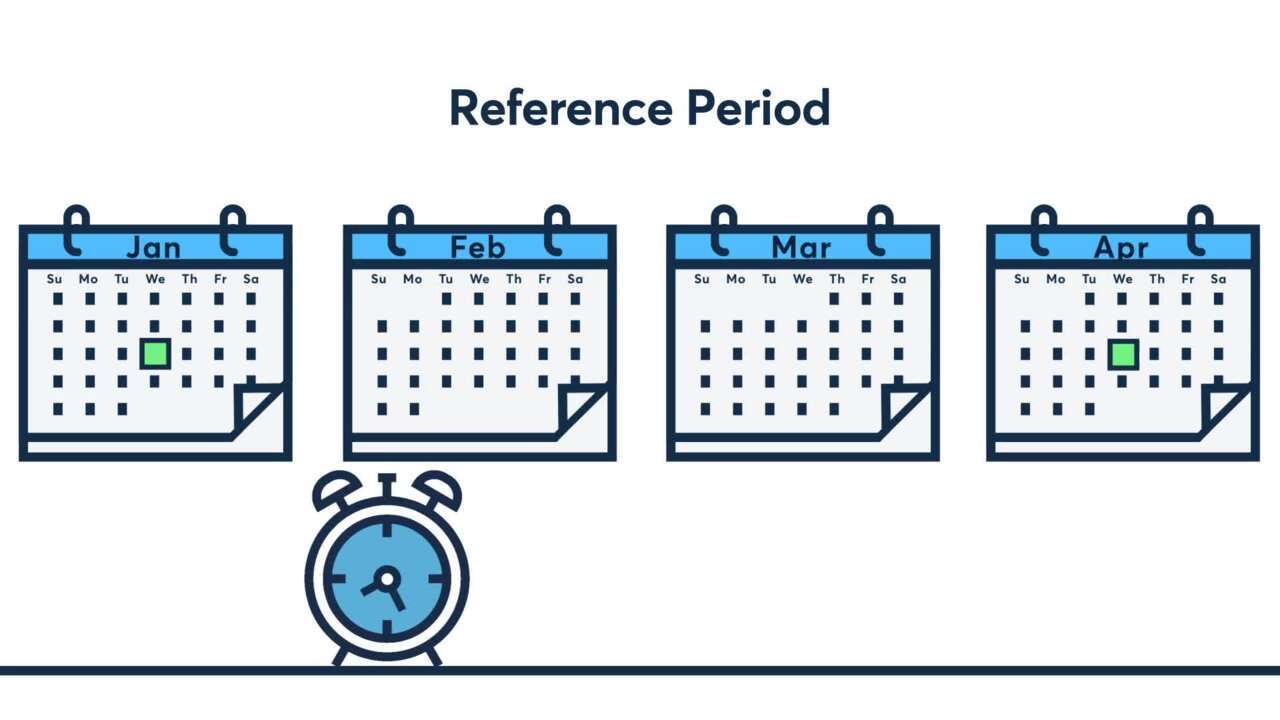

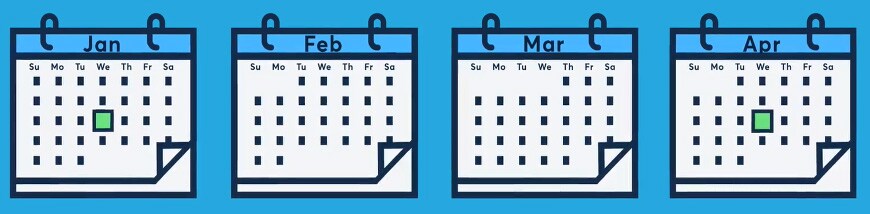

The final settlement price is determined by the compounded €STR rate over the relevant reference period, which starts on the third Wednesday of the named contract month and ends on the business day immediately preceding the third Wednesday of the contract’s delivery month three months later.

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/trading-estr-futures-img1.jpg

{kind=link}

Prior to final settlement, €STR futures prices represent market expectations for the compounded daily overnight €STR benchmark rates over the contracts’ reference periods, a fact that remains the case even as the contract enters this period. As time passes, an increasing number of the contract’s daily fixings become known; however, the contract’s price continues to trade based on a blend of actual and expected future fixings until the end of the reference period.

€STR outright contracts have a standard tick increment of one half of a basis point (0.005), however this reduces as the contract nears expiration:

- Contacts with over four months until expiration: half of a basis point (0.005)

- Contracts within four months of expiry up until the month of expiration: one quarter of a basis point (0.0025)

- Contracts within one month until expiration: one eighth of a basis point (0.00125)

The €STR Single-Contract Basis Spread futures contract is designed to represent the market expectations of the difference between the Three-Month Euribor benchmark and the expected value of a matching Three-Month €STR swap. For example:

https://www.cmegroup.com/content/dam/cmegroup/education/courses/images/trading-estr-futures-img2.jpg

{kind=link}

It is designed to replicate the FRA-OIS spread traded in the OTC market and the price of the contract tracks the spread. It is traded as a single contract and remains in that state until its final settlement date, at which point the contract delivers holders into a position in the same month outright €STR contract. Long contract holders are assigned long positions of the same named month of outright €STR futures, while short holders are assigned short positions in the outright. Additional details about how contracts are assigned at settlement can be found in this article.

For more information on both the outright and Single-Contract Basis Spread €STR futures contracts, visit cmegroup.com/ESTR.