Understanding Implied Liquidity in Equity Sector futures

{kind=link}

Liquidity for equity index futures is often measured by what investors can see quoted or traded on-screen. If the central limit order book (or CLOB) displays a wide bid-ask spread or shows small size, a market participant may incorrectly conclude that the contract is illiquid. However, with the multitude of ways to trade futures, such as through the CLOB, Basis Trade at Index Close, Block Trades, Derived Block Trades or Exchange for Physicals, investors can tap into additional sources of liquidity.

Finding Additional Sources of Liquidity

Consider, a fund manager that needs to trade $25 million in the Financial Select Sector Index intraday, and prefers to trade capital efficient futures. The manager calculates a need to buy 260 XAF contracts to achieve the desired exposure. The manager sees a 3-tick wide market on 15 contracts and notices that XAF trades ~2000 contracts per day on average. While realizing that working the order may take too long and may result in price slippage, instead, the manager contacts his/her broker, or a futures’ block liquidity provider, and indicates interest in a block trade.

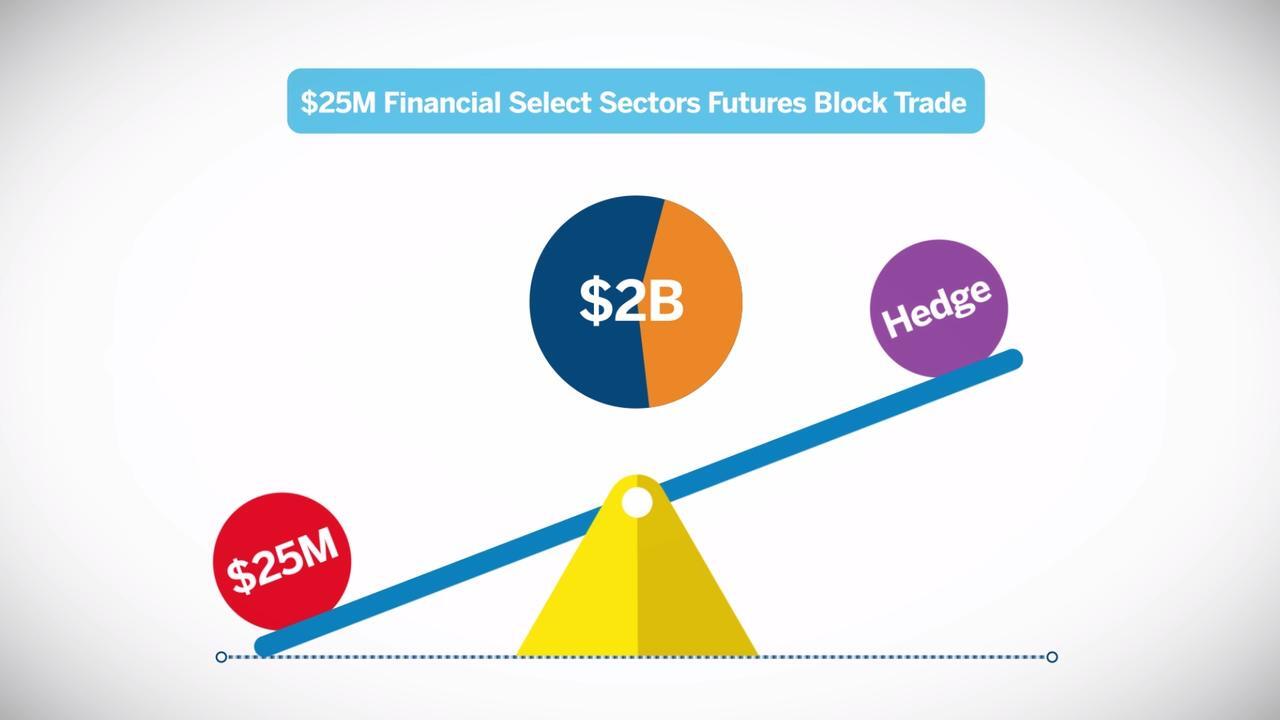

Block Trade

A futures block trade allows participants the flexibility to privately negotiate larger transactions at fair and reasonable prices. The dealer will most likely provide a market based on the liquidity of the underlying single-stock index constituents or the corresponding ETF. By taking advantage of the activity in adjacent markets, the block provider may quote prices on quantities, more than what could be seen on the futures CLOB. In this case, for a $25 million Financial Select Sector futures block trade, the dealer could easily combine its hedge from the nearly $30 billion that trades daily in the underlying stocks and the corresponding ETF market.

Derived Block Trade

A derived block trade is a block trade consummated by eligible contract participants, in which the price and quantity of the trade depends on hedging transactions in an eligible related market. Parties agree to the pre-defined notional or number of contracts and the markets in which the hedging transaction will take place. Additionally, a basis price will be agreed to and added to the index price of the resultant delta hedge in the related market.

Permitted hedging instruments include stock baskets and other eligible related market instruments such as ETFs. Pre-defined hedging methods are volume weighted average price (VWAP), time weighted average price (TWAP), percentage of volume (POV), and limit price (LP).

Basis Trade at Index Close (BTIC)

Liquidity in the Equity markets can be at its highest at the cash close. Market participants who are looking to trade at the cash close can look at Basis Trade at Index Close, or BTIC, block trades with futures. This aligns the futures block execution against the close, to leverage the volume transacted in the index component market-on-close (MOC) auctions. A BTIC block trade enables investors to trade futures at a negotiated spread to the underlying cash index official close and thus provides participants price and size certainty.

To execute a BTIC block, a fund manager needs to reach out to a liquidity provider and negotiate the fair value spread, or basis, of the futures to the Index, say -1.50 index points. The dealer may hedge the BTIC futures trade by buying the required number of shares per component in each stock’s respective MOC auction and perfectly replicating the cash index closing value. If the official index close was 385.0, the 260 futures contracts would be executed at 383.50 via the BTIC block. This enables a fund manager to execute a full order in one trade with price certainty, and encourages a dealer to trade more size via BTIC as a result of the hedge certainty provided by transacting stock in the MOC auction.

Exchange for Physical (EFP)

A fourth way to access futures exposure is by tapping into the liquidity of the ETF market and then converting the ETF position into futures via an Exchange For Physical (EFP) transaction. EFP transactions are also privately negotiated. For example, a fund manager purchased ~1 million shares of the Financial Select Sector ETF at a price of $30 to use liquidity in the ETF market, the fund manager could then negotiate an EFP with a dealer to exchange the ETFs for an equivalent futures position using E-mini Financial Select Sector Futures contracts.

Summary

The complete liquidity profile for a futures contract is dependent on the availability of equivalent, and substitute products that market makers can use to price and hedge the futures, as well as the availability of exchange mechanisms such as blocks, derived blocks, BTIC and EFPs that can be used to access the contracts. CME offers market participants exposure to benchmark equity indices where both on- and off- screen liquidity can be accessed to best meet their risk management needs. To learn more please visit cmegroup.com/equities.