Introduction to European Crude Oil

{kind=link}

Introduction to European Crude Oil

The North Sea in the 1970s and 1980s offered stable government, good access to markets and good financing opportunities. For these reasons, the crude oil benchmark, Brent crude, developed in this region.

Brent crude was adopted by producers in Russia, North and West Africa, and in Asia in the early 2000s. The physical market is dominated by the trading in a forward market that enables users to trade monthly oil cargoes for three to four months ahead.

Forward trades are either full-size North Sea crude cargoes of 600,000 barrels or smaller, 100,000 barrel partials that are cash-settled unless the same buyer and seller trade six partials in the same delivery month.

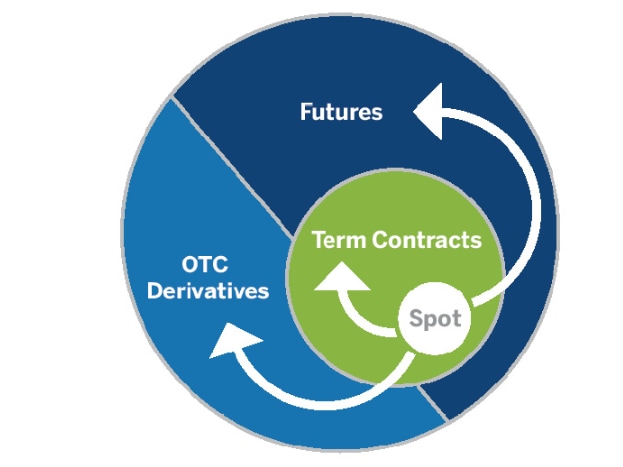

The Brent Spot Market

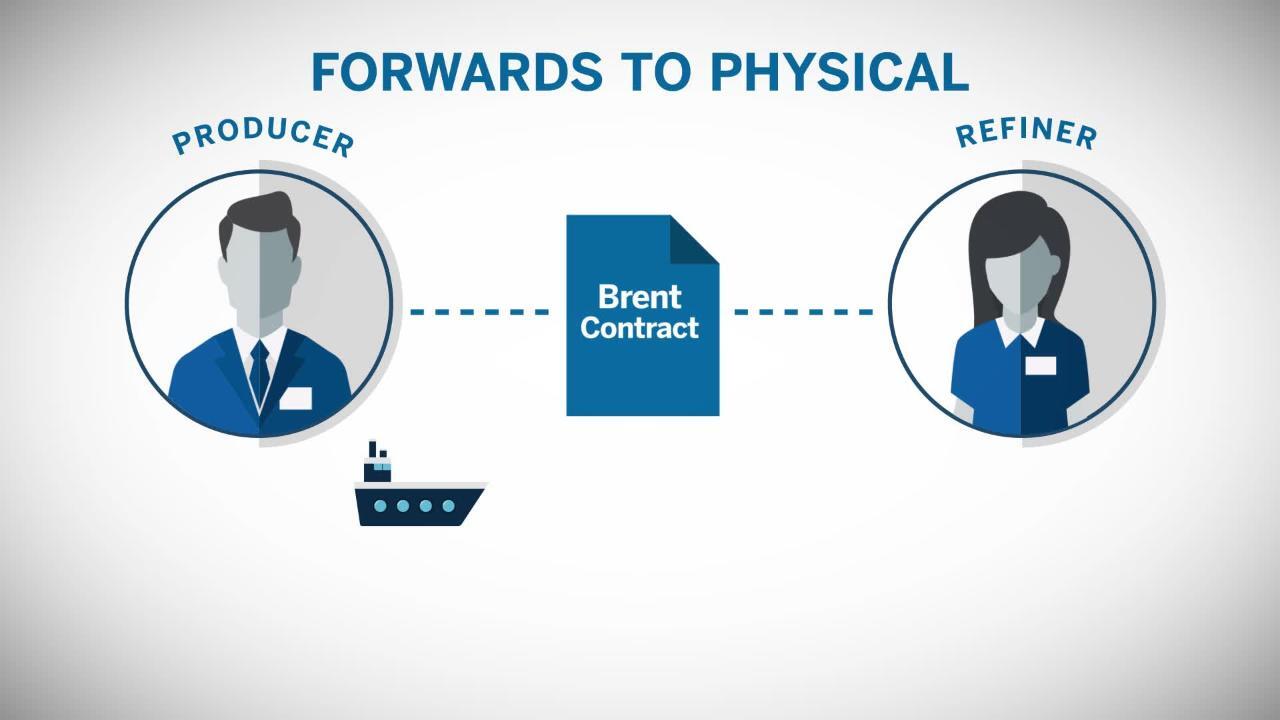

There is an established mechanism for moving from the forward to the physical market.

A producer agrees a month-ahead forward contract with a refiner for a specific contract month.

The field operator of one of the specified fields announces the loading dates month-ahead before the month starts to be wet.

Equity producers can either start nominating their cargoes or they can keep them. When a buyer is passed a cargo, they can choose to keep it or pass it along, creating a chain with whomever they have a month-ahead contract with.

If the cargo is nominated on-time the buyers must accept the cargo offered. Once the deadline for nominating a cargo has passed, the cargo turns physical and it can then be traded as dated Brent cargo as precise loading dates will be attached to that cargo.

The spot, or physical, market for Brent is called Dated Brent, referencing the value of spot cargoes trading in the North Sea. Several different crude grades underpin Dated, which vary in quality and price. An adjustment mechanism enables these grades to be assessed to a standardised specification in term of quality.

The cheapest of the underlying grades is used to determine the value for Dated Brent. Dated Brent is widely used by both the upstream and downstream, as well as the broader energy industry. Prices are also used by some of the relevant tax authorities in the calculation of the tax reference prices used by the industry.

The Development of Futures for the North Sea

With the forward market already developed and successfully trading, the futures market, was a logical next step in Brent’s evolution.

Based on the activity in the forward Brent market, the futures markets developed in the late 1980s. Today, they are a major price benchmark reference for European oil trade. Futures facilitate trading further down the curve with contracts listed in months for up to 10 years ahead.

There is a wide range of market participants in the futures market, from commercial energy firms, to traders, to financial participants. This makes the Brent futures market a significant price discovery tool, available for trading 23-hours-per-day.

Brent futures are cash-settled against an index price that is based on the trading of cargoes in the forward Brent market. The Brent market also offers monthly financial-based contracts based on the underlying futures market.

Sitting alongside the cash and dated structures are a series of financial-based derivative contracts facilitating the hedging of both short-term and long-term crude oil markets.

The Wider Brent Derivative Markets

There are a series of financial-based contracts available to successfully manage short-term and long-term risk in the North Sea.

At the near-term end, there are weekly Contracts for Difference (CFDs), which allow you to manage exposure to the Dated Brent price for a specific week, or set of weeks, up to 12 weeks ahead.

Monthly contracts and financial-based futures based on the underlying futures market, are also listed to help you hedge exposure to Dated Brent.

Brent’s Physical Supply Base

The underlying crude grades, which underpin the Brent market, are Brent, Forties, Oseberg, Ekofisk and Troll (deliverable from January 2018). Production in these crudes has fallen over the years, and quality differences between each grade means that adjustments had to be made to compensate participants if they accepted or delivered a different quality crude oil. Outside of these main benchmark crudes, the other producing regions are in the UK and Norwegian North Sea, as well as offshore Denmark and the Netherlands.

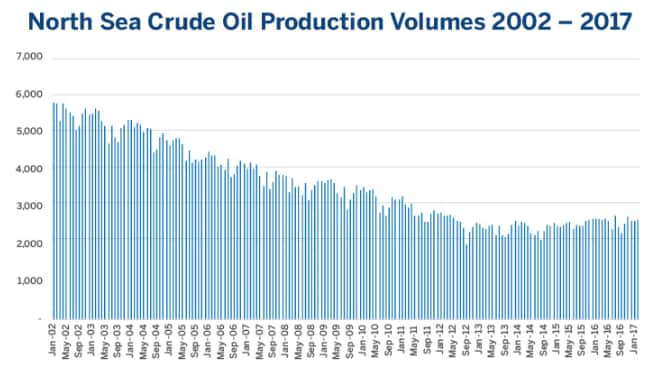

Production costs for the main oil producers in Europe tend to be high when compared to other regions. Supply has fallen from a 2002 peak of around 6 million barrels per day and the 2016 volume was around 3 million barrels per day, as shown in the chart below.

{kind=link}

New discoveries of oil deposits were made, but these tend to be smaller than in other parts of the world. Some upstream operators turned their attention to other regions where the reserve base is typically higher and cheaper to extract. Niche upstream operators in the North Sea are used to drilling for oil in areas that are difficult to extract from and have had some successes for future production, especially in the Norwegian oil sector.

Source: JODI (Joint Organisations Data Initiative)

European crudes are most commonly stored and refined locally within the European market, but some cargoes are exported outside the region to countries in Asia. Some of the crudes are transferred into storage in the Asia region or are sold directly to refiners in the region.

The spread between Brent and the Asia benchmark, Dubai, are used to support this trade. Similarly, U.S. crudes that are exported to Asia or Europe can be traded using two benchmarks, the WTI and Brent. Liquidity is high on both spreads and these are active markets listed for trading on the exchanges. The WTI-Brent spread has been very volatile in the recent past, and with U.S. exports being permitted, the spread is likely to represent a true reflection of the arbitrage economics from the U.S. Similar parallels could be drawn for the WTI-Asian crude spreads where there were several exported cargoes to refiners in the region.

{kind=link}

Hedge Example – Using Dated Brent

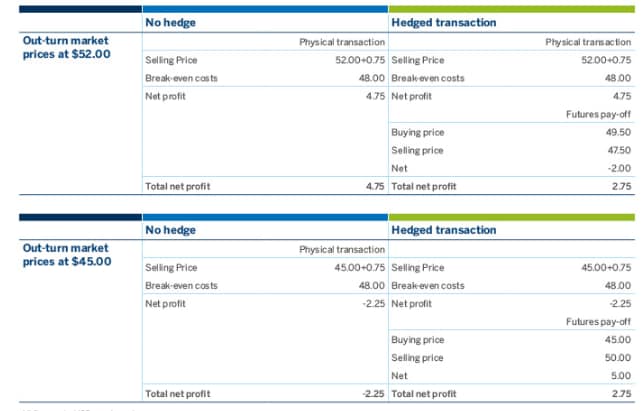

A North Sea oil producer agreed to a six-month supply deal of 1 million barrels per month with an oil refiner. The pricing basis for the contract is the monthly average of Dated Brent + a premium of $0.75 cents per barrel for each shipment.

The producer is looking to fix the sales price to the refiner for the next six months to protect from the downside impact of falling prices.

The breakeven cost for the producer is $48.00 per barrel so a price level higher than this would see the producer generating a profit. The current price for the next six months is averaging $49.50 per barrel.

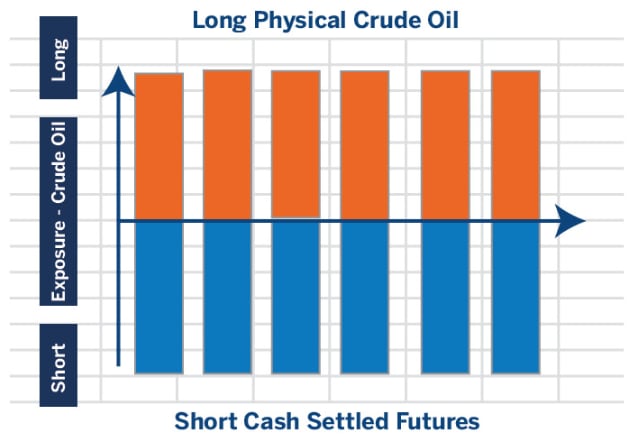

The producer is a natural long in the physical market and is therefore exposed to a fall in prices. To protect against this risk, the producer is looking to hedge their forward price exposure in the futures market. For the producer to be fully hedged in the market, they would take a short position in the futures market to align with a natural long position in the physical market. The diagram below shows what a hedged position would look like for the producer.

{kind=link}

The price of Brent crude is averaging $49.50 per barrel over the next six months, as determined by trading activity in the futures market. If the price falls below the $48 per barrel breakeven cost, the producer would be running their production at a loss and would potentially face a reduction in output. Or they would supply crude at a loss to the refiner.

The producer faces two choices: exposure to the market price or hedging its production and selling forward the price of crude oil for the next six months.

By achieving a hedge price of at least $48 per barrel for each delivery month, the producer can provide cash flow certainty and maintain all its supply commitments.

WHAT INSTRUMENT WOULD BE USED FOR THE HEDGE?

The Brent Dated to Frontline futures contract covers the price differential between the daily price of Platts Dated Brent and the futures settlement for the financial Brent futures contract for that day. Therefore, using a hedge combination of the DFL for each delivery month plus the financial Brent futures price for each delivery month would be an effective way to hedge.

HEDGE FORMULAE

The Dated to Frontline futures (DFL) price for September + the Brent Financial price for September = a September flat price Dated Brent value for September delivery. The formulae can be modified to generate a monthly Dated Brent price for each delivery month.

We can consider two possible scenarios over six months: either the spot price increases from $48 to $52, or it falls back down to $45. There was a negotiated differential to the spot price of 75 cents per barrel, which was built into the price. In both cases, the producer can achieve stable margins of $2.75 when using the monthly futures as a hedge:

{kind=link}