Establishing a Floor Price by Buying Put Options

{kind=link}

There are many risk management strategies available that offer price protection for short hedgers involved in producing or selling grain and oilseed products. Farmers, merchandisers, grain elevators and exporters understand the impact that a decline in prices could have on their business. It is important that they at least familiarize themselves with various alternatives for mitigating this risk and protecting their bottom line.

Selling futures contracts allows short hedgers to lock in a selling price for grain, because a loss in the cash is made by a gain in the futures market, and vice versa. This strategy will satisfy the needs of many short hedgers, who have calculated the selling price that will allow their business to be profitable.

Some hedgers would like the ability to establish a minimum selling price for grain, while still being able to take advantage of a potential increase in grain prices. That is where options come in, offering price protection plus flexibility.

This module will describe how grain sellers can purchase put options to establish a minimum, or floor, selling price for grain, while still maintaining the opportunity to sell grain at a higher price.

Example

Assume that it is Spring and a soybean producer has just completed his planting. He is concerned that soybean prices may decline by the time he harvests his beans in October.

The normal basis for his area in October is 20 cents under the November Soybean futures price, which is currently $9.50 a bushel. This would give him an expected selling price of $9.30, which is the November futures price minus the expected basis.

The producer has determined that a selling price of $9.30 will allows his operations to be profitable.

One alternative is to lock in the selling price of $9.30 with a short futures hedge, by selling November futures at $9.50. However, the producer decides to buy put options to establish a floor selling price and retain the opportunity to potentially sell his soybeans at a higher price.

By purchasing the put option, he has the right, but not the obligation, to sell futures at the strike price of the option.

In April, a November at-the-money put option with a strike price of $9.50 costs 25 cents. With this put option, he will establish a floor price of $9.05, which equals the put option strike price of $9.50, minus the expected 20 under basis, minus the 25-cent premium he paid for the option.

If soybeans prices fall, this is the minimum price he will receive.

FALLING PRICES

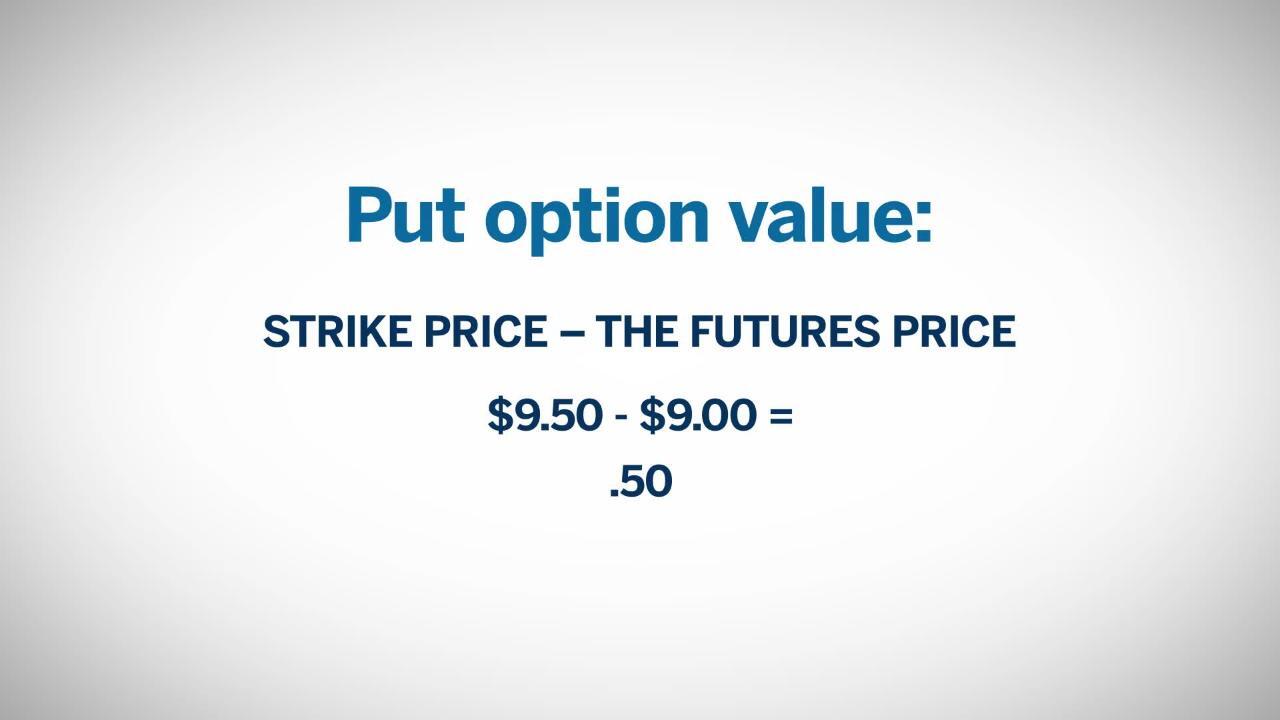

Suppose the November Soybean futures price falls to $9.00, which would mean a cash price of $8.80, the futures price minus the expected 20 under basis.

Since the put option gives the farmer the right to sell at $9.50, even though Soybean futures are at $9.00, the put option has a value of at least 50 cents, the $9.50 strike price minus the futures.

Deducting the 25-cent premium gives the farmer a net gain of 25 cents on his put option hedge.

The cash price of $8.80 plus the 25-cent gain provides the farmer with an effective selling price of $9.05 per bushel. Again, no matter how low soybean prices have fallen by the time he sells his beans in November, assuming the basis is stable, the lowest price he will get for his soybeans is $9.05.

RISING PRICES

Suppose the November Soybean futures price rises above the $9.50 strike price. In this situation, the farmer will still be able to participate in the upward price movement.

Say November futures increase to $10.00 a bushel. Taking into account the 20 under expected basis, the cash price in the producer’s area would be $9.80.

Since the $10.00 futures price is higher than the $9.50 strike price of the put option, the farmer allows the option to expire and sells his soybeans in the cash market.

The most he will lose is the 25-cent premium he paid upfront. His net selling price will be $9.55, which is the futures price of $10.00, minus the 20 under basis, minus the 25-cent premium.

With soybean prices falling, the net selling price of $9.05 was lower compared to the $9.30 he would have locked in with the short futures hedge, the difference, essentially, being the option premium. The farmer was willing to pay the premium because it allowed him to secure protection from declining prices and, unlike the short futures hedge, still have the opportunity to get a better price for his soybeans in a rising market: $9.55 versus $9.30 with a futures hedge.

He will receive less for his beans in this scenario than the $9.80 had he not hedged at all,

the difference, again, being the option premium. But, knowing that the price could just have easily declined, he was willing to pay this cost to ensure a minimum selling price for his soybeans.

Keep in mind that the farmer also has the possibility of selling his put option for any time value that it may still hold. Whatever he receives from selling the option would increase his net selling price even more.

Conclusion

The benefits of buying put options for the short hedger:

- He knows the cost of the option and the maximum loss up front: the option premium

- He is able to establish a floor price for his sales

- He still has the ability to take advantage of higher prices

No one can predict the future, but hedgers can take steps to manage it. Using grain futures and options allows those who need protection against falling prices to have peace of mind of knowing that they have taken steps to manage the risk involved in producing and selling these commodities for their business.