https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/2019/ici-coal_984x137.jpg

{kind=link}

Year One: Indonesian Coal Derivatives (ICI 4)

In a short period, Indonesian coal derivatives have established themselves within the coal trading product landscape. Trading in the ICI 4 futures contract began twelve months ago, and we take the launch anniversary as an opportunity to look back and take stock. The introduction of any new futures contract is a challenging undertaking, and many contracts fail to see continuous trading following launch. We will assess the success of the ICI 4 product using three criteria: i) does it trade? ii) how far out along the curve does it trade? and iii) is there a fundamental reason why market participants use this product?

Growth in Trading Activity

The ICI 4 futures contract is the first financial futures contract that covers low-calorific Indonesian coal (4,200kcal/kg GAR). It is cash settled to the ICI 4 index, which is produced by price reporting agencies Argus and PT Coalindo Energy. Since our contract went live on February 5th, 2018, the contract has seen trading activity every month. Total volume traded to date1 amounts to 2,005 lots, equivalent to 2 million metric tons of coal. Notwithstanding a seasonal slowdown over the Christmas/end of year period, the volume and open interest trends are pointing in the right direction. The contract has found good industry support, with 5 different brokerage firms facilitating trades in the contract, and over twenty different firms trading to date. With the increasing number of participants, we are also seeing larger clips being traded, as counterparts are looking to hedge full cargoes in one transaction.

{kind=link}

Trading Hours

Trades in the contract were mainly executed during Singapore afternoon hours, with the bulk of trading (75% of total volume) done between 2pm and 7pm (corresponding to 6am-11am London time). This indicates that price discovery occurs during afternoon Asian hours and before most European traders begin their day. To illustrate this point, we compare the time of trade execution to that of our API 2 Coal Futures contract– the API2 is a globally relevant price for high calorific coal delivered in North-West Europe and is based on a joint Argus-IHS McCloskey assessment.

{kind=link}

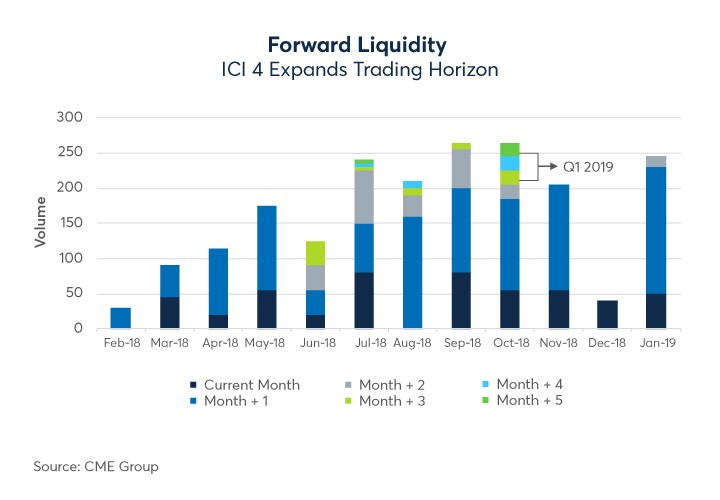

Term Hedging

One of the main purposes of futures contracts is the ability to manage commodity price risk over longer timeframes. Looking into trading data, we can see that the ICI 4 contract fulfils this requirement. Market participants were initially concentrating their activity at the nearby end of the forward curve, executing trades for the current month or for the first nearby month. Over time, the trading horizon of participants extended beyond the two front contracts. We can point to the month of October, when the first Q1 2019 trades were executed. Forward trading is a great milestone for any futures contract, as it indicates that participants are confident that the contract price reflects their physical exposure over the longer term. Forward liquidity is a crucial component of any successful futures contract.

{kind=link}

Alternatives to the ICI 4

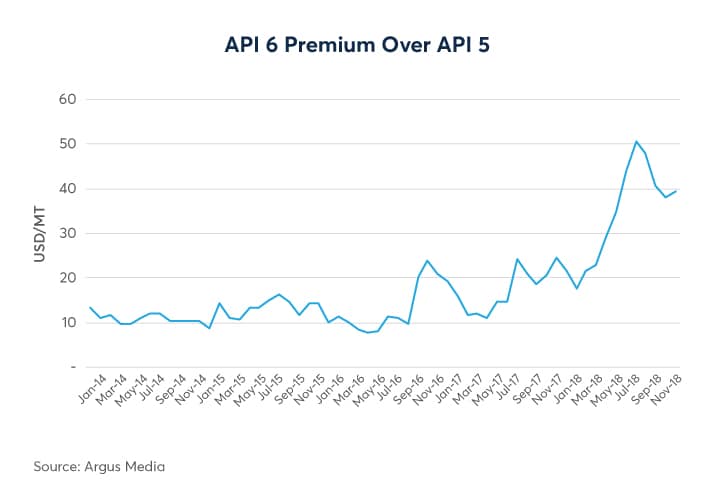

When alternative contracts offer higher liquidity and a longer trading history, why do market participants use the ICI 4? Historically, participants with price exposure to Asian coal used high CV indices (typically 5,500 or 6,000 kcal/kg NAR shipped from Newcastle, Australia). In the last year, prices of the 6,000 FOB Newcastle market skyrocketed, which led to an unprecedented widening of price spreads against lower CV grades. This can be seen in the relative price difference between API 6 and API 5, the Argus/McCloskey markers for the 6,000 and 5,500 FOB Newcastle export markets.

{kind=link}

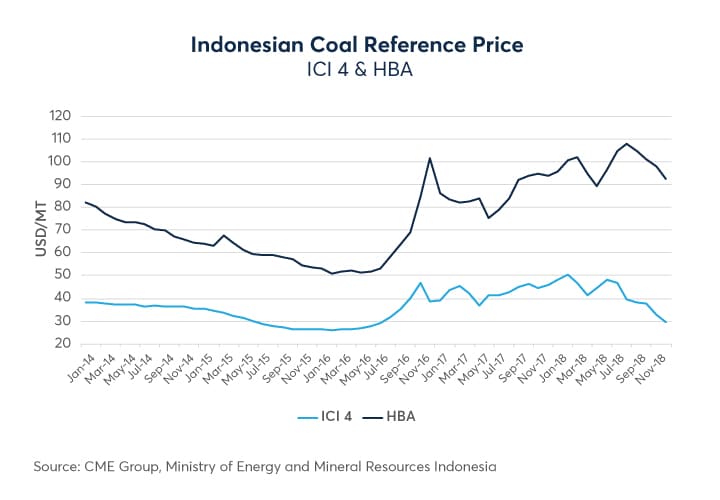

In the below chart, we compare the ICI 4 to the Indonesian Coal Export reference price (“HBA - Harga Batubara Acuan”). The HBA is a reference price published by the Indonesian government. It is a weighted average of different high CV assessments for coal shipping from Indonesia and Australia. The severe widening of the spread between HBA and ICI 4 indicates that high CV contracts are not a good proxy-hedge to manage Indonesian low-calorific coal price exposure. This increased basis risk indicates that price exposure to low-calorific coal originating from Indonesia may be hedged using a regional and CV specific hedging tool, namely the ICI 4 futures contract. Whilst the “great disconnect” within the high CV complex continues, participants can also make use of the whole range of hedging products available: besides the ICI 4 contract, CME Group offers Asian Thermal coal products based on the API 5 (5,500 FOB Newcastle basis)- both as 1,000 MT futures contract and as a 10 MT “micro” futures contract – and on the API 8 (5,500 CFR South China) in addition to the highly traded API 2 (CIF ARA) and API 4 (FOB Richards Bay) contracts.

{kind=link}

Market Fundamentals

Coal market fundamentals are providing further tailwind to the Indonesian coal complex. Indonesia is the world’s largest exporter of thermal coal used in power stations. Its two major customers, India and China, are also the world’s largest coal importers2. Chinese buyers are attracted to Indonesian coal to blend with their local production and prefer low-calorific, low-sulphur, Indonesian coal to higher priced Australian material. Despite abundant local reserves, India is also a keen importer of Indonesian coal: For many power plants in the South and the West of the country, it is more economical to import coal over sea routes from Indonesia than to haul Indian coal across the country via rail3. Despite the long-term positive outlook, temporary Chinese import restrictions imposed at the end of last year show that the market is also influenced by short-term factors. The spread widening between different CV grades should also emphasize the degree by which the market for FOB Indonesian coal differs from the market for high calorific coal – which is typically shipped from Australia to Japan and South Korea.

On the supply side, the Rupiah steadily depreciated against the dollar over the past 5 years. This means that royalties from dollar priced coal exports will continue to play an important role in balancing the Indonesian government budget. For 2019, it left its coal production target largely untouched (480 m MT in 2019 vs. 485m MT in 2018)4. The presidential elections in April 2019 will be one event to watch.

Conclusion

We measured the success of the ICI 4 contract against three criteria: i) trading activity – particularly during Asian market hours, ii) price discovery along the curve and iii) the economic rationale for using the contract. On all three counts, the contract is fulfilling its purpose. We are hopeful that continuous industry backing will make the second year even more of a success and will continue to support the contract. The physical export market from Indonesia is poised for further growth as India and China continue in their path of economic expansion. This provides the backbone upon which the ICI 4 paper market will evolve.

References

- as of February 1st, 2019

- https://www.reuters.com/article/column-russell-coal-indonesia/column-indonesia-wants-to-export-more-coal-buyers-ignore-the-call-russell-idUSL4N1WR24R

- https://www.cmegroup.com/Energy/Coal/Indias-Coal-Paradox.html

- https://www.cmegroup.com/news/2019/01/08/indonesia-sets-lower-coal-production-target-to-help-stabilize-global-price.html