{kind=link}

WTI Extends its Reach as US Export Growth Transforms Global Crude Oil Market

WTI Extends its Reach as US Export Growth Transforms Global Crude Oil Markets

Executive Summary

Increasing demand for US crude oil exports is reaffirming global reliance on the CME Group’s NYMEX Light Sweet Crude Oil futures contract (referred to as “WTI futures”) while firmly establishing WTI as the price discovery leader in the crude oil market. The WTI futures contract and its underlying physical market is the most liquid and transparent in the world. The US pipeline market provides a straight-forward structure for trading and pricing physical crude oil, compared to the Brent market which involves an opaque matrix of price assessments comprised of cargoes traded (if any), cash forward deals (which are increasingly illiquid), transactions in Contract for Differences (CFD) swap futures (which are cash-settled derivatives), and a quality adjustment (which can vary based on the specific North Sea grade). Consequently, WTI has taken on a more significant price-setting role globally.

In 2020, a milestone was reached when US crude oil exports to Europe surpassed the total supply of Brent (BFOET) crude oil streams, establishing WTI as a key price marker for the European oil market. As US crude exports gain deeper penetration in the global oil markets, S&P Global Platts (“Platts”) has undertaken an initiative to reform the Brent market which is plagued by declining production and decreasing liquidity in the physical spot market that underpins the Brent futures market. The Brent basket of crude oil streams has expanded over time to provide additional spot market liquidity, and the cargo loading window has been extended from the original 15 days ahead to 30 days ahead currently. However, the prospects for market reform are uncertain, and there is no clear consensus among market participants for the best path forward.

The growing competitive position of WTI in world oil markets is driven by two key factors: 1.) Export growth; and 2.) Record US oil production.

US crude oil exports and production

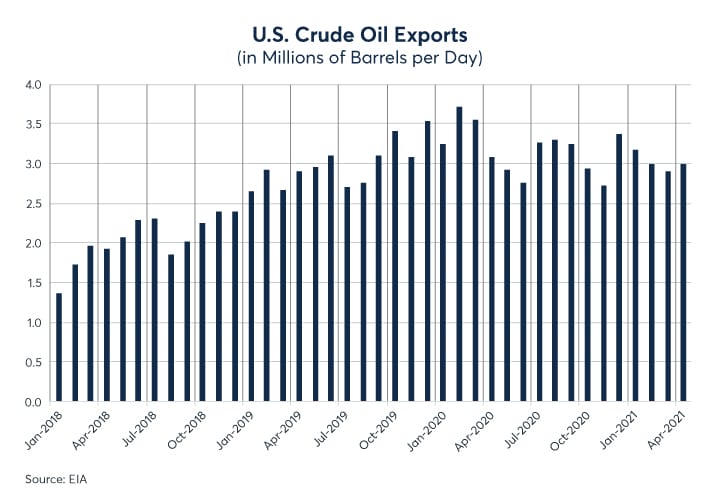

US crude oil exports climbed to a peak of 3.7 million barrels per day (b/d) in February 2020 and reached an annual average of 3.2 million b/d in 2020. The main destination for US crude oil exports in 2020 was Asia at 1.4 million b/d, followed by Europe which averaged 1.15 million b/d in 2020. As US crude exports gain deeper penetration in the global oil markets, the US has become a dominant supply source for the European refining market. Consequently, WTI has extended its price-discovery role as the marginal supplier of oil to Europe.

The growth in exports has been transformative for the US crude oil market. Houston has become a major export hub, and new infrastructure has been constructed to process the growing export volumes.

{kind=link}

US crude oil production climbed to a peak of 13.0 million b/d in November 2019, and then stabilized at 11.5 million b/d on average in 2020, higher than Saudi Arabia and Russia.

Cushing logistics

At the heart of the global pricing network, the Cushing, Oklahoma hub provides the physical delivery mechanism for the WTI futures contract. When the WTI futures contract was first listed in 1983, Cushing was a vibrant hub for cash market trading connected to a vast network of pipelines, refineries, and storage terminals.

Today, Cushing is the key nexus of market fundamentals for the global crude oil market, with nearly two dozen pipelines and 20 storage terminals with shell capacity of 100 million barrels, the largest storage hub in the world. The US pipeline market provides a highly liquid and straight-forward structure for pricing physical crude oil, with a robust spot market at major trading hubs in Cushing, Midland, and Houston. By contrast, the Dated Brent (or “spot”) market is not transparent and relies on a complex matrix of price assessments comprised of spot cargoes, cash forward deals, transactions in weekly contract for differences (CFD) swap futures, and a quality adjustment based on each specific North Sea grade.

Cushing storage levels are highly visible and published weekly by the US Energy Information Administration (EIA), providing important transparency to the marketplace. In contrast, the Brent (BFOET) loading terminals in the North Sea have zero storage capacity, and waterborne floating storage is opaque and not reported publicly.

WTI-type crude oil is directly connected to the export market in the US Gulf Coast via pipelines from Cushing, Oklahoma and Midland, Texas. The Cushing hub is directly connected to the Gulf Coast waterborne terminals via pipeline with nearly 2 million barrels/day capacity; the Midland, Texas hub is linked to the export market with over 5 million barrels/day of pipeline capacity. Since the US first permitted exports outside of North America in 2016, volumes have grown significantly. This has placed the US firmly on the map in terms of the big global crude suppliers and increased WTI’s significance as a global benchmark.

It is not just the storage or pipeline capacity that make Cushing the critical hub as the delivery point for the global oil benchmark, but also the interconnectivity between a diverse mix of commercial hedgers. The WTI futures contract allows for delivery through Enterprise and Enbridge facilities in Cushing, or at a facility that is connected to either. The Cushing terminals provides a key junction point, capable of facilitating the transfer of millions of barrels of crude oil every day. The physical-delivery requirement of WTI futures provides a direct link to the underlying cash market, and the futures contract also provides the security of a clearinghouse for buyers and sellers.

{kind=link}

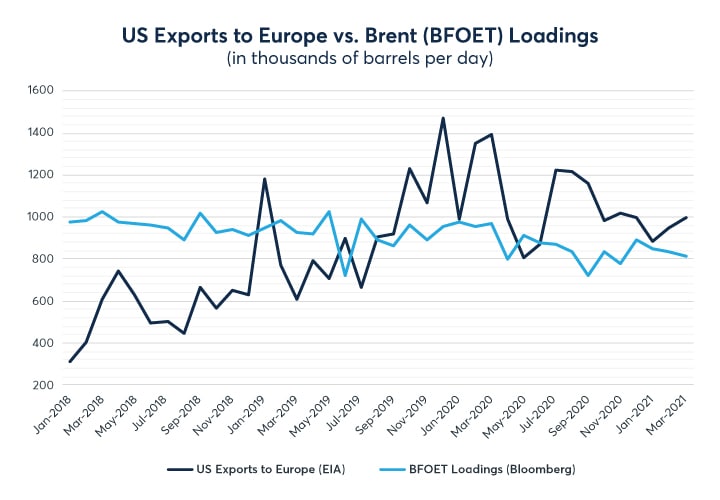

Rising US exports to Europe surpassed Brent supply in 2020

Surging US crude oil exports to Europe surpassed the total supply of Brent (BFOET) crude streams in the North Sea in 2020. US crude oil cargoes delivered to Europe averaged 1.15 million b/d in 2020, compared to average Brent (BFOET) loadings of 870,000 b/d. Cargoes of WTI are now actively traded in Rotterdam, and both Platts and Argus are publishing assessments for WTI delivered to the European market. With daily export volumes of over one million b/d to Europe, WTI is now a baseload grade for the European trading community and its refiners, according to Platts.

{kind=link}

Source: EIA and Bloomberg

The Brent market faces growing uncertainty

In the face of declining production and sparse liquidity in the physical Brent market, Platts has undertaken an initiative to reform the Brent cash market that underpins the Brent futures market. Platts predicts that Brent (BFOET) loadings in the North Sea will decline to less than one cargo per day (600,000 b/d) in 2022, down from 870,000 b/d in 2020. Platts has withdrawn its original proposal to radically alter the Brent market by transforming the Brent assessments from an FOB basis to a CIF delivered basis to Rotterdam. In addition, the Platts proposal expanded the Brent basket to include cargoes of delivered WTI type crude oil. This proposal was designed to inject spot market liquidity into the declining supply of Brent (BFOET) grades, but it would impact the value of millions of barrels of open interest in the various Brent-related futures contracts. After mounting criticism of its proposal, Platts has delayed a decision on market reform and is seeking additional feedback on possible solutions.

The complexity of the Brent market makes it difficult to find a solution to the current dilemma of rapidly declining production and decreasing spot market liquidity. In the past, Platts has expanded the crude oil streams in the Brent basket to include Brent, Forties, Oseberg, Ekofisk, and Troll (BFOET). Further, the cargo loading window has been extended from the original 15 days ahead to 30 days ahead to provide additional spot market liquidity. At this time, the prospects for market reform are uncertain, and there is no clear consensus among market participants for the best path forward. As a result, WTI has extended its significance as the global benchmark.

MYTH: WTI is a regional land-locked benchmark.

REALITY: WTI crude oil is not land-locked; it is directly connected to the US Gulf Coast export market via pipelines from Cushing, Oklahoma and Midland, Texas. The Cushing hub is directly connected to the Gulf Coast waterborne terminals via pipeline with nearly 2 million barrels/day capacity; the Midland, Texas hub is linked to the export market with over 5 million barrels/day of pipeline capacity. At the same time, the production of North Sea Brent (BFOET) crude oil streams is declining rapidly and physical market trading in the Brent spot market is illiquid. US exports of WTI to Europe have surpassed Brent (BFOET) production and have injected needed liquidity into the European spot market, while also increasing WTI’s significance as a global benchmark.

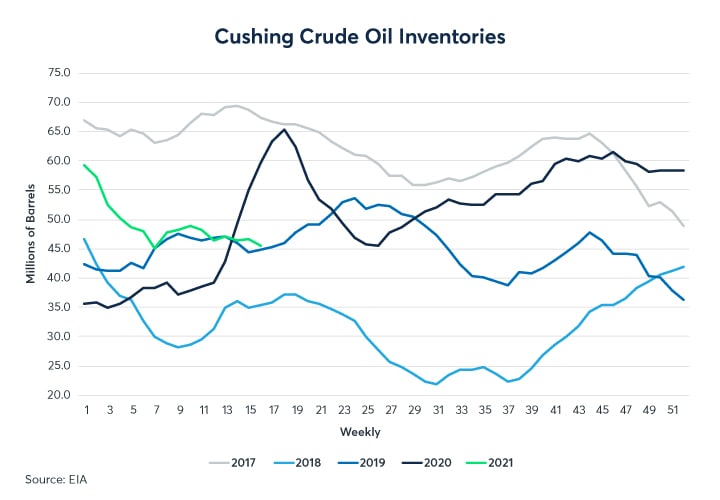

MYTH: The Cushing hub has limited storage capacity and almost reached full capacity in May 2020.

REALITY: The Cushing hub is the largest in the world with 100 million barrels of shell storage capacity. At peak storage levels in May 2020, crude oil inventories reached 65 million barrels in Cushing, leaving 35 million barrels of excess capacity. The Cushing storage levels are highly visible and published weekly by the US Energy Information Administration (EIA), providing important transparency to the marketplace. By comparison, the Brent (BFOET) loading terminals in the North Sea have zero storage capacity, and floating storage is opaque and not reported publicly.

MYTH: WTI futures are geared for financial participants, not physical market participants.

REALITY: The WTI futures contract is the most liquid physically-delivered contract in the world with direct price convergence to the underlying Cushing WTI cash market as opposed to an opaque index. Market participation in WTI futures is diverse and includes hundreds of commercial hedgers, including refiners, oil traders, and banks; as well as investment funds and retail investors.