{kind=link}

Why Smart Money Trades Spreads—A Three-Part Series Part I

With the unprecedented flow of volume into futures contracts, it comes as no surprise that there are key features to learn about futures contracts. Liquidity, leverage, around-the-clock trading and tax advantages are among some of these great features. But one of the more useful features of futures contracts is the ability to spread futures contracts. Some veteran traders and professionals avail themselves to spread strategies because they can offer certain features that outright long or short positions can’t.

Moreover, with the coronavirus pandemic, worldwide financial markets have exhibited an enormous amount of volatility that is impacting some of the spreads we shall discuss.

The goal of this series is to help those with less experience understand the notion of spreading futures contracts. But before we get into why smart money trades spreads, let’s begin with a few definitions.

A spread trade is the simultaneous purchase and sale of two futures contracts in order to take advantage of price discrepancies. There are primarily three types of spreads* with futures (in this paper, we will focus primarily on inter-commodity spreads):

- Intra-market spread (aka: calendar spread or intra-delivery)—A spread in which the trader is long and short basically the same commodity futures, but different expiration months (i.e., July/November soybean spread).

- Inter-commodity spread—A spread in which the trader is simultaneously long and short two different futures, such as being long the E-mini S&P 500 (large-caps) and short the E-mini Russell 2000 (small caps).

- Complex spread—A spread in which the trader is long/short multiple legs, such as Eurodollar butterflies with futures (these are different from options*), the Soybean crush spread, or the crude oil crack spread. These complex spreads are usually traded by professionals.Pros and Cons of Spread Trading: As with any type of trading, spread trading offers a myriad of positives and a few negatives.

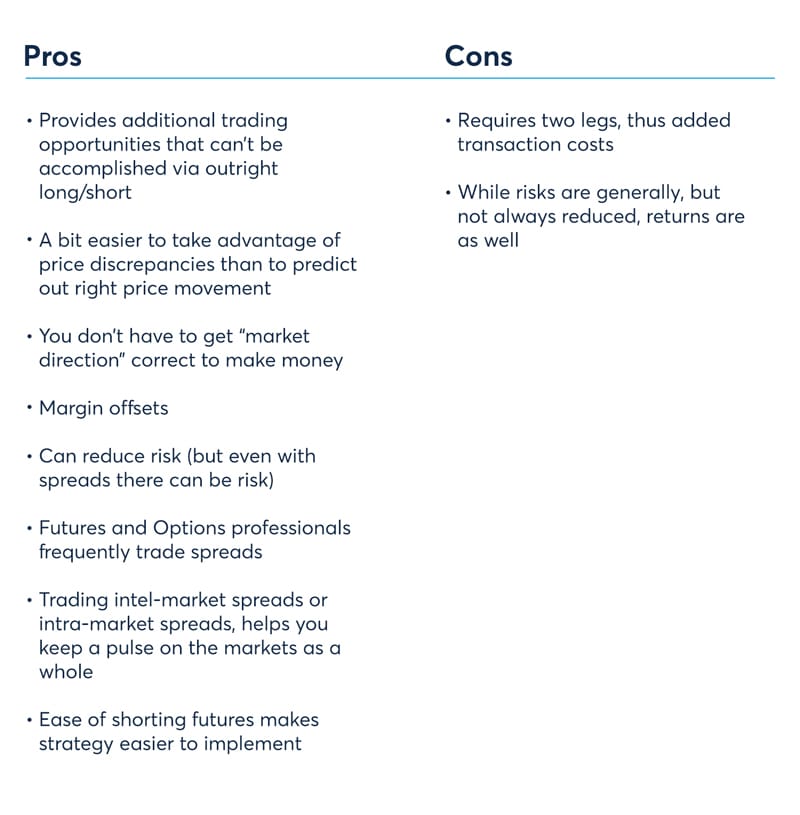

Pros and Cons of spread trading: As with any type of trading, spread trading offers a myriad of positives and a few negatives.

The first major positive is the ability to profit in both up and down markets. For example. If a trader is long WTI and Short Brent Crude at a differential of 5 (brent $5.00 premium to WTI), the trader will profit as long as the spread declines below $5.00. This can happen if prices in WTI and Brent advance or decline. As long as WTI gains on Brent, the spread will profit and the trader doesn’t have to worry about advancing or declining markets.

The second advantage is that spreading is unique to futures and as such affords futures traders a great deal more strategies other than outright long and shorts. If a trader thought small cap stocks were going to outperform large cap stocks, the trade can be done easily and cheaply with futures. While the trade can in fact, be done with stocks or even ETFs, the capital requirement and margin would be substantially larger.

One of the best advantages to spread trading is they often offer margin offsets or discounts. Later in this series, we will have several examples that demonstrate the advantage of margin offset. With margin offsets, traders enjoy significant cost savings! Figure 1 below lists many of the pros and cons of trading spreads with futures.

Figure 1

{kind=link}

*not to be confused with options spreads, where there are literally hundreds if not thousands of spread combinations given all the strike prices and expiration months.

A spread trade is the simultaneous purchase and sale of two futures contracts in order to take advantage of price discrepancies. There are primarily three types of spreads* with futures

— Dave Lerman

Concepts and requirements to understand before considering spreads

Before investors can trade spreads, they must adhere to a few “rules” and guidelines. Some spreads will be done in a 1:1 ratio. For example, the WTI-Brent spread is executed in a 1:1 ratio. But because of differences in notional amounts, other ratios might be required. The 2-Year Treasury to 10-Year Treasury spread uses a 2:1 ratio because of changes in notional value—the 2-Year having a $200,000 notional and 10-Year having a $100,000 notional.

Margin offsets can only be achieved if spread is done in accordance with clearinghouse ratios. Hence, if the clearinghouse recognizes a 2:1 ratio, the margin offset will only apply if the trade is done in a 2:1 ratio. Any other ratio will require greater upfront margin.

Spread traders should always check the CME Group website or consult with their FCM/broker for the specifics of the spread in which they are interested.

Common Spreads in Futures Trading

There are hundreds, if not thousands, of spread trades one can create with futures contracts. You could fill a book with seasonal and calendar spreads alone. In Part 1, we will introduce some of the more popular intermarket and intra-market spreads (and may cover seasonality and calendar spreads in more detail later in the series). Figure 2 shows a sample of common spreads.

In each part of this series, we will cover the basics (and some details) of how to construct these spreads, what the trader might expect from the strategy, and the ratio specifics and margin offsets.

Figure 2

| Spread | Trade Specifics | Margin offsets* |

| S&P 500/E-mini Russell 200 spread | Large caps outperform small caps or vice versa | Yes |

| Gold/Platinum spread | Gold outperforms platinum or vice versa | Yes |

| Gold/Silver spread | Gold outperforms silver or vice versa | Yes |

| July/November soybean spread | Old crop/new crop discrepancies | Yes |

| WTI/Brent crude spread | The battle between two benchmarks | Yes |

| 2-yr Treasury vs. 10-yr Tresury note | Yield curve play | Yes |

| *offsets available only at approved clearinghouse ratio | ||

Spread trading can be an important strategy to take advantage of many opportunities in different markets

Over the past 90 or so years, small cap stocks have outperformed large cap stocks by a few percentage points (13% annualized vs. 10% annualized).

Spreading Stock Index futures—Large Caps vs. Small Caps

Traders and investors keep a close watch on the key equity index benchmarks—typicallyl focusing on the S&P 500 and the Dow. The S&P 500 is the main benchmark used to measure how a portfolio manager performs. The index is comprised of large-capitalization stocks. The idea is to outperform the benchmark and explore investing opportunities. The S&P 500 is also an important economic barometer. In growing economies, the companies within the index do well, and their stock prices advance thus pulling the benchmark to higher levels. This was amply demonstrated in 2019 as the S&P 500 mounted record after record as the year drew to a close. In 2020, the severe drop in the S&P 500 in only three weeks mirrored the severity of the global economic shutdown due to the Covid-19 pandemic.

But beyond the large-capitalization universe lies mid- and small-cap stocks. For now, we will focus on large-caps and small-caps and consider mid-caps for a later discussion. The key benchmark for small-capitalization stocks is the Russell 2000 Index. And at times, this area of the market can sometimes march to the beat of a different drummer—i.e., outperform or underperform. Over the past 90 or so years, small-cap stocks have outperformed large-cap stocks by a few percentage points (13% annualized vs. 10% annualized). This is because small-cap stocks tend to grow faster, although they are riskier. Large-caps within the S&P 500 tend to be steadily growing stalwarts and are less nimble. But over the short term, large-caps and small-caps can leap-frog each other in performance. And this is where a skilled trader might see opportunities. Figure 1 below illustrates how these two indices exchange periods of outperformance. Although the chart compares 20 years of small/large-cap performance, we will focus on the period of December 31, 2017 until August 2020.

Over the calendar year 2017, the S&P 500 outperformed the small-cap benchmark Russell 2000 by 6.23 percentage points. But interestingly, by summer of 2018, small caps took the lead and by July were ahead by 5.7 percentage points. Why the abrupt swing?

In a word: China. Spring and summer of 2018 marked the beginning of the trade/tariff wars between the United States and China. Now, digging deeper, why would this affect large caps more and cause them to underperform? The answer lies with the large multinational companies that make up the S&P 500. Large multinational companies like Caterpillar, United Technologies, Boeing, and others have more to lose in a trade war as they derive a substantial percentage of revenue from overseas. Smaller companies that make up the Russell 2000 do not have as large a global footprint and thus they’re generally immune from trade wars.

Again, at the end of 2018, the relationship flipped again, and large caps took the lead despite the ongoing trade war. What happened? The fourth quarter brought a serious correction in the markets and when the market falls significantly, smaller, less well-capitalized stocks fall further. Hence the Russell 2000 underperformed in the latter half of 2018.

As of August 2020, the Nasdaq-100 has gone on to new highs, the S&P 500 is up 3.73% in 2020 and within striking distance of all-time highs, yet the Russell 2000 index remains nearly 6% below where it began 2020. Astute traders can capitalize on these opportunities. Sometimes they can be short-term diversions; other times they can take days, weeks, or months to develop.

With the liquid E-mini and Micro E-mini S&P 500 and Russell equity index products, this may present as a unique product suite that might allow for a spread trade geared toward a specific market viewpoint. To learn more about E-mini and Micro E-mini equity index products, visit cmegroup.com/equities.

With the liquid E-mini and Micro E-mini S&P 500 and Russell stock index products, this may present as a unique product suite that might allow for a spread trade that’s geared toward a specific market viewpoint.

Figure 1: Small cap and large cap performance over time.

| Year | Russell Performance | S&P 500 Performance | Russell Minus S&P 500 | Russell Outperforms |

| 12/31/2001 | 1.02% | -13.04% | 14.06% | Yes |

| 12/31/2002 | -22.39% | -24.22% | 1.83% | Yes |

| 12/31/2003 | 44.97% | 27.02% | 17.95% | Yes |

| 12/31/2004 | 17.42% | 10.59% | 6.83% | Yes |

| 12/30/2005 | 3.32% | 3.00% | 0.32% | Yes |

| 12/29/2006 | 17.00% | 13.62% | 3.38% | Yes |

| 12/31/2007 | -2.02% | 4.24% | -6.26% | No |

| 12/31/2008 | -38.22% | -40.97% | 2.75% | Yes |

| 12/31/2009 | 25.21% | 23.45% | 1.76% | Yes |

| 12/31/2010 | 25.31% | 12.78% | 12.53% | Yes |

| 12/30/2011 | -5.45% | 0.00% | -5.45% | No |

| 12/31/2012 | 12.31% | 11.52% | 0.79% | Yes |

| 12/31/2013 | 39.84% | 31.80% | 8.04% | Yes |

| 12/31/2014 | 3.53% | 11.39% | -7.86% | No |

| 12/31/2015 | -5.71% | -0.73% | -4.98% | No |

| 12/30/2016 | 18.05% | 8.50% | 9.55% | Yes |

| 12/29/2017 | 12.64% | 18.87% | -6.23% | No |

| 7/20/2018 | 10.50% | 4.80% | 5.70% | Yes |

| 12/31/2018 | -12.17% | -6.24% | -5.93% | No |

| 12/31/2019 | 25.42% | 31.29% | -5.87 | No |

| 8/07/2020 | -5.95 | 3.73% | -9.68 | No |

Spread trading illustration

A trader observes that while the S&P 500 is at new record levels, the Russell 2000 is still about 8% below its all-time high. Furthermore, he/she believes the performance gap will narrow and the Russell 2000 will again relative to the S&P 500. To take a position based on this opinion, the trade would require a long position in the E-mini Russell 2000 or the Micro E-mini Russell 2000 and a simultaneous short position in the E-mini or Micro E-mini S&P 500. The correct ratio according to the CME Group clearinghouse would be 2 Micro E-mini Russell 2000 futures for every 1 Micro E-mini S&P 500. As you can see from Figure 2 below, the trade offers an 80% margin offset! The entire trade can be executed for a margin requirement of $472.

If the Russell 2000 outperforms the S&P 500, this may present as opportunities for some. Should large caps maintain and extend their out-performance, this would probably not create opportunities to capitalize on.

Figure 2

| Contract | Exchange | Initial Margin/Leg |

| Micro E-mini Russell 2000 futures | CME | $580 x 2 = $1,160 |

| Micro E-mini S&P 500 futures | CME | $1200 x 1 = $1,200 |

| Position total gross margin | $2,360 | |

| Margin offset | 80% | |

| Total margin (as of 8/07/2020; subject to change) | $472 |

Conclusion

While this illustration features spreading small-caps vs. large-caps, one could also spread other parts of the market such as mid-caps vs. large-caps or mid-caps vs. small-caps. In addition, a trader could also spread foreign stock indexes such as the Nikkei 225 vs. the S&P 500 depending on which market the trader thought would perform the best. Sector futures also exist, and if a trader believes that utilities (for example) were going to outperform the overall market, a trade exists for that opinion as well. CME Group lists 10 Sector futures contracts (the 10 sectors that make up the S&P 500), and they can be spread against each other or against broad stock indexes subject to a number of conditions and requirements being met.

It is essential to consult with FCMs regarding their guidelines on margins (which are subject to change and subject to CME Group’s minimum margin requirements). Don’t forget to pay attention to the correct spread ratio. Spreads not done in accordance with clearinghouse ratios are subject to higher margins.

{kind=link}

{kind=link}