{kind=link}

Why ESG is Outperforming the S&P 500

Out Performing ESG Futures Start Here

- After markets closed on April 30, 2020, the S&P 500 ESG Index underwent its second annual rebalance.

- The S&P 500 ESG Index has provided low tracking error relative to the >S&P 500 with similar risk, and a superior returns performance of +2.68%.

- Here we examine some of drivers of the outperformance and examine how the availability of a liquid futures contract makes access easier.

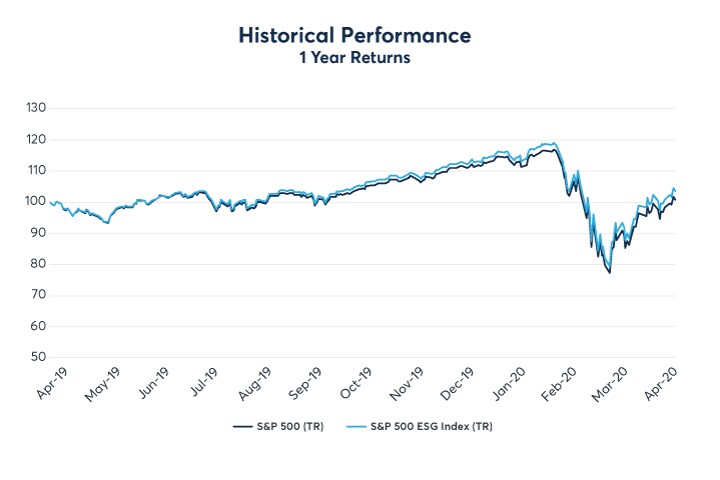

The S&P 500 ESG Index is Showing Resilience in the COVID-19 Crisis.

Over the past one–year period the S&P 500 ESG Index exhibited excess returns performance of 2.68%1 against the benchmark S&P 500 index. This is impressive given the objective of the S&P 500 ESG Index is not to outperform the benchmark. Instead, it can offer a sustainable alternative to the broad-based S&P 500, with similar risk and return, while at the same time achieving a boost in S&P DJI ESG Score performance.

One Year Historical Total Returns Performance of the S&P 500 ESG Index against S&P 500 Index

{kind=link}

Source: SPDJI

The Coronavirus pandemic is strengthening the hand of ESG investors2. Sustainability-themed funds saw record Q1 inflows in the US, while the rest of the market saw record outflows. Globally, investments in ETFs tracking ESG indices more than doubled, going from $22.1 billion in 2018 to $56.8 billion by the end of 20193. The pandemic has only reinforced Fund Managers’ belief in ESG, with investors focusing on environmental, social and governance themes

Firstly, Let’s Look at the Recent Rebalance.

The S&P 500 ESG Index is designed to be a broad-based, benchmark. The screening criteria states that companies are excluded if they have a low ESG score relative to industry peers, are involved in controversial weapons or tobacco, are not closely adhering to the UN Global Compact, or are involved in severe controversies4.

As of the 2020 rebalance, 311 constituents made it into the S&P 500 ESG Index. Some of the biggest additions include names such as Facebook (whose inclusion was largely driven by improvements in its governance score), Thermo Fisher, Costco, Eli Lilly and Wells Fargo. Some of the largest deletions included Walmart, Raytheon Technologies, Charter Communications, Crown Castle and US Bancorp5.

Being included in the index is perhaps more relevant now than ever before as there is growing regulatory importance. Growing regulatory importance makes those firms who are included in the ESG Index perhaps more relevant now than ever before. The need to integrate investors’ values in ESG is now, also a key consideration for money managers.

How can ESG drive performance?

The pandemic could potentially impact all industries due to simultaneous supply and demand shocks. Those issuers that have lower environmental, social and governance characteristics may be more particularly affected. An ESG lens teases out all sorts of risks that are not necessarily apparent in conventional financial analysis. This screening may be the reason that the S&P ESG 500 index has outperformed its parent index in the recent sell-off.

Many observers believe that strong ESG performance indicates better management, and that screening for companies with high ESG scores is simply a way to find good executive teams which translates into stronger long-term returns. The idea being that management teams that do a good job of minimizing their environmental footprint; promote good employee relations, contingency plan, enforce employee sick leave policies and are prepared for disasters, create resilient governance structures. These types of management teams are more likely to be adept at running all other aspects of a company’s business and should be better equipped to ride out a downturn.

ESG analysis regularly focuses on supply-chain transparency. These challenges often occur many steps up a supply chain, and when companies struggle to address them, it’s often because they simply don’t know much about where their raw materials really are provided from. Global supply chains present an excellent example of how interrelated our business worlds are.

For example, as the Coronavirus pandemic started to disrupt supply chains from China and authorities began to shut down economic activity, many companies were caught by surprise when their own products or services were affected leading to stock price shocks.

What Drove the Outperformance?

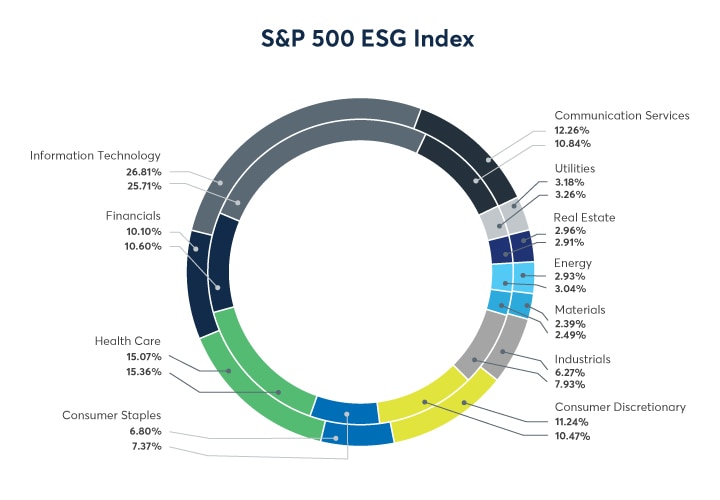

Of the newly rebalanced ESG index, the index weighting by GICS sector breakdown for the S&P 500 ESG Index as compared to the S&P 500 Index is shown diagrammatically below. Consumer Discretionary, Information Technology, Communication Services and Real Estate all have a higher weighting in the ESG version than the parent index.

S&P 500 and S&P 500 ESG Index weighting by GICS sector breakdown

{kind=link}

Inner ring: S&P 500 Index

Outer ring: S&P 500 ESG Index

Source: SPDJI

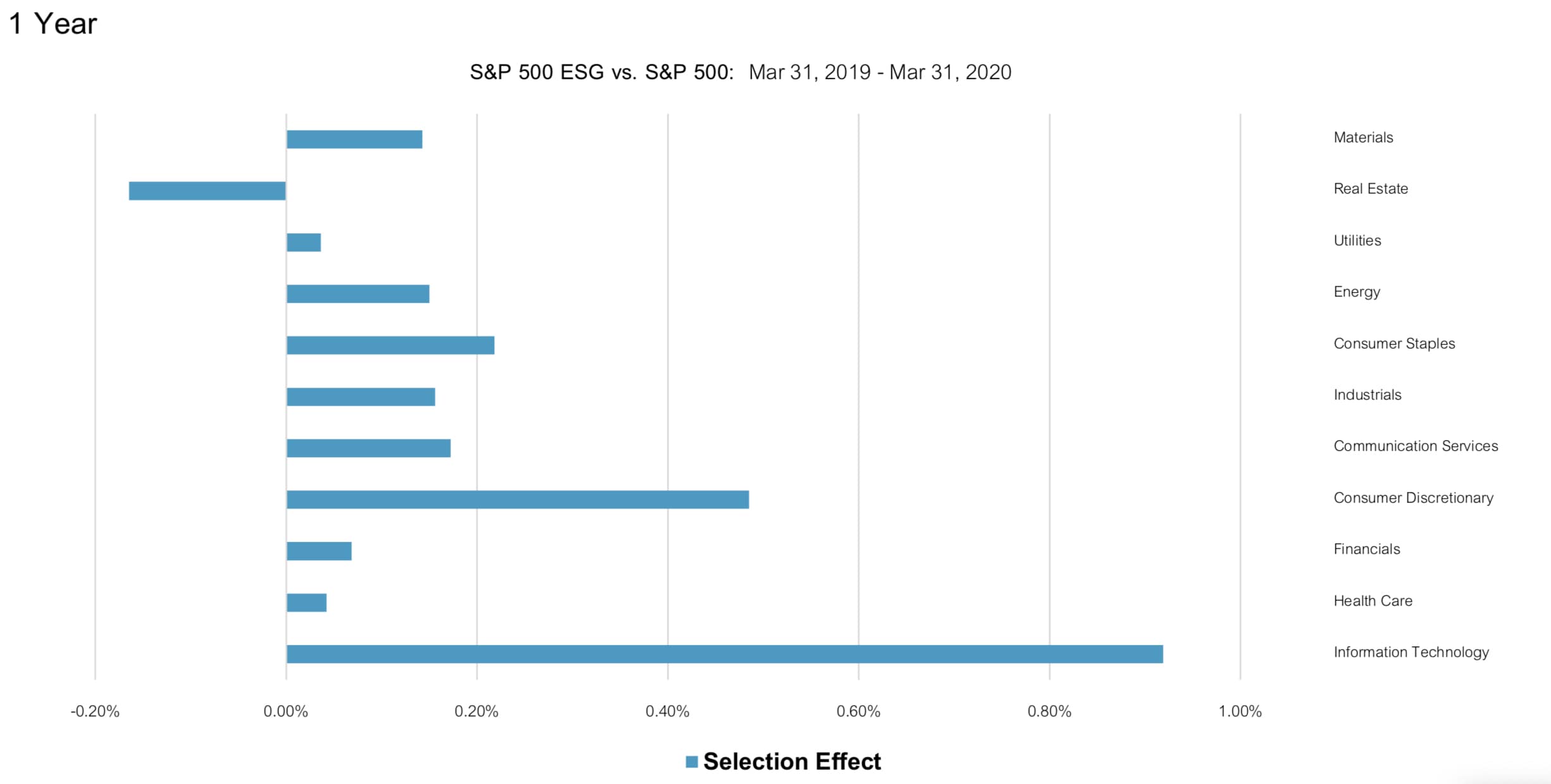

The main drivers of the outperformance of 2.68%, was a combination of allocation effect (+0.46%) together with selection effect (+2.23%).

In particular, the higher weight allocated to the Technology Sector saw those constituents performing better than those in the parent S&P 500 Index and so contributed to +1.30% outperformance of the S&P 500 ESG than the S&P 500. Of the 1.30% outperformance 0.92% was the stock selection effect and 0.38% a result of the weighting allocation.

Outperformance was also driven by better stock selection in the Consumer Discretionary (+0.47%), Consumer Staples (+0.21%), Industrials (+0.35%), and Materials sector (+0.20%).

Better stock selection is the main driver

S&P 500 ESG Index Performance Attribution – Selection Effect

{kind=link}

Source: SPDJI

At first glance one may assume that the outperformance is due to the ESG selection criteria making the index under-invested in energy, oil and gas; a naturally more polluting sector.

Oil and gas companies have been among the worst hit in the current downturn for a variety of reasons; there is drastically lower demand for crude oil as the number of people driving has fallen, limited storage capacity has driven oil prices into negative territory for the first time in history, energy companies are still reeling from recent price wars and many of them are overleveraged and drowning in debt. The inability of exploration and production companies to curtail production quickly, coupled with lower oil prices has caused the sector to underperform, comparatively speaking.

However, the market cap weighting to the energy sector is only slightly different between the two indices, hence the allocation is not the driver. The filtering process has seen the ESG index gain performance of +0.07%.

The S&P 500 ESG Index has provided low tracking error relative to the S&P 500, but also performed well due to the way the index methodology sorted the largest companies that drove performance.

Some companies that were significant drivers of the S&P 500’s performance in the past 12 months, such as Apple and Microsoft, passed through the screens and remained in the S&P 500 ESG Index and were allocated a higher weighing. Other major companies with less-than-stellar performance, such as Boeing, were excluded.

Another factor affecting a company’s ESG score, is the strength of its balance sheet. These companies are generally the ones that are run better and operate more efficiently. With the exclusion of Berkshire Hathaway, the same largest ten names by market cap appear in both indices, however given the difference in allocation, the weighting of the top ten constituents is 6.95% greater in the ESG index, and the weight of the largest constituent 1.73% more.

Post COVID-19, CME’s E-mini S&P 500 ESG Future is Attractive

The pandemic has only reinforced the focus on ESG and has accelerated its integration into mainstream, core, portfolio selection. Investors are accelerating their focus on ESG despite of, or possibly due to, the pandemic.

The E-mini S&P 500 ESG futures is the derivative solution for responsible investing, allowing clients to align their financial goals with their environmental, social, and governance values. The underlying index, which has a meaningful filtering methodology and a significant ESG boost, gives investors’ comfort that they can integrate ESG into the core of their portfolio whist still achieving a tight tracking error to S&P 500. The 5-year tracking error is 0.83%, allowing clients S&P 500 like performance but in an ESG positive manner.

On May 18, a new record volume day was achieved in the E-mini S&P 500 ESG Futures contract with a total of 5,071 contracts traded ($637mn notional). The OI growing by 986 contracts to 3,874 ($487mn notional).

In the six months since launch, the E-mini S&P 500 ESG future has established itself as one of the largest ESG futures globally in terms of the notional value of open contracts, trading in excess of $5.6 billion notional since launch with an average daily trading volume of ~540 YTD, with May running at 800 so far. Liquidity continues to grow, with a tight bid-ask spread, narrowing to 4 ticks wide for 10 lots. Market participants are accessing the ESG futures contract not only to tick the compliance box, but also to enjoy the outperformance.

The ESG futures contract can allow users capital efficiency by saving on margin offsets that may be available with other equity index futures. As things begin to return to some normality, we see clients assessing the market for ESG offerings. The versatility to manage positions through flexible execution, including Basis Trade at Index Close (BTIC), Exchange for Related Positions (EFRP’s) or block trades, offer multiple ways to find liquidity and another easy way to trade the E-mini S&P 500 ESG Future.

Further into 2020, as countries emerge out of the Coronavirus crisis, ESG topics are may be central to many governments and companies. French and German ministers have called for the EU to expedite their CO2 reduction plans and avoid pro-fossil fuel measures post lockdown to boost the economy. In the US, companies have pushed for a carbon tax and for green projects to be at the heart of recovery plans. Even within the aviation sector, in the US there is a push towards decarbonization and sustainable aviation fuels. Further, the EU is looking to make emissions cuts a pre-requisite for the bailout of any airline. This in turn will bring more focus on ESG futures.

As companies, investors, and governments investors look to allocate more capital towards ESG compliant exposures, the CME S&P 500 ESG Index futures can be a useful tool to help manager’s meet their ESG goals.

References

- SPDJI Presentation: S&P ESG Index Series and SP DJI Index Scores. Q2 2020

- FT Article headline: https://www.ft.com/content/19047cda-0648-48a9-a512-87653149026c

- S&P DJI Estimates

- Full methodology available at https://us.spindices.com/indices/equity/sp-500-esg-index-usd

- https://www.spglobal.com/en/research-insights/articles/what-can-sp-dji-s-custom-indexing-do-for-you