{kind=link}

Volatility impacting EU hot-rolled coil pricing mechanism

Established pricing mechanisms in the European hot-rolled coil (HRC) market are comparatively antiquated compared with other sectors.

Long-term contracts are often done on a fixed-price basis, leading to increased risk exposure and resulting in unnecessarily protracted talks when they need renegotiating. In the rare cases where buyers and sellers do use an index, they settle against one that publishes just once a month.

This approach made sense when raw materials were priced annually, and at a fraction of their current cost. But since iron ore and coking coal have moved away from annual benchmark pricing to shorter-term contracts — monthly and spot, in the case of iron ore — raw materials’ volatility reverberates throughout the supply chain. These monthly prices are comprised of daily index publications.

An index that publishes once a month will fail to capture the range of prices over that period and will lag the real market during upswings and downturns.

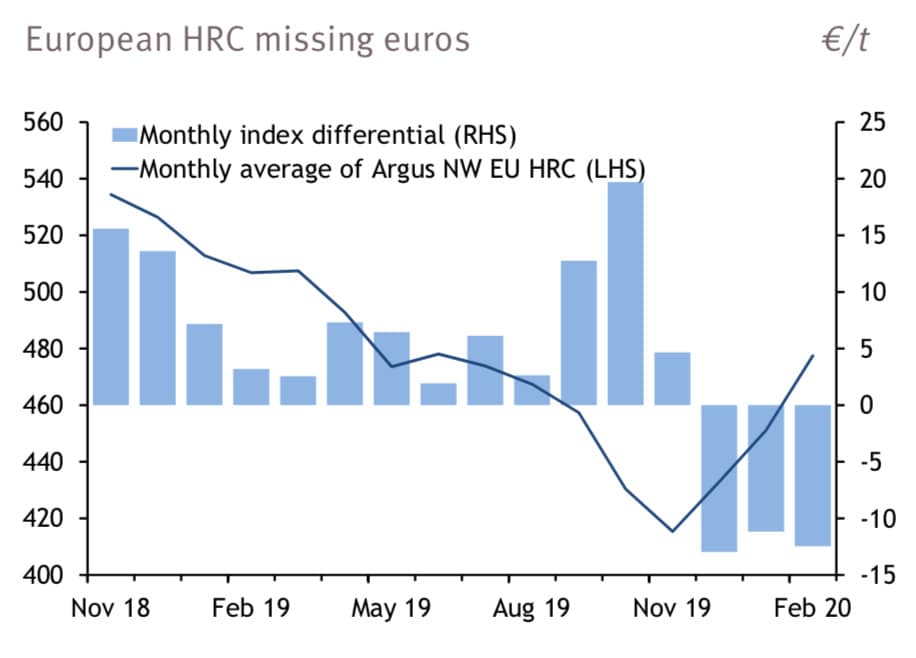

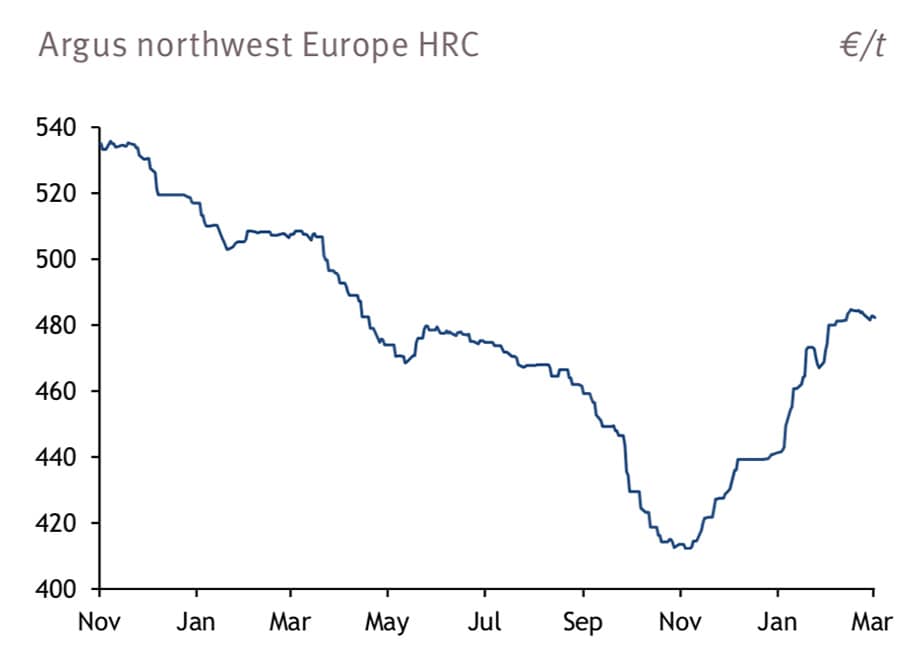

To put this in context, the February average of the daily Argus northwest Europe HRC index was €477.78/t. The monthly published index for February was €465/t. So mills selling against this index were literally throwing away €12.78/t.

Of course, this was good for the buy-side, but they would end up paying more than the real market in a downturn. Buying or selling against an index that publishes once a month makes it difficult to forecast revenue going forward and to mark a stock position against the market.

A daily index provides more clarity than the likely monthly average a few weeks in, and it is easier to track its performance relative to the marketplace. Sales and purchases against the monthly average of a daily index are also much easier to hedge, as most risk management tools typically settle against daily, if not weekly, indexes.

{kind=link}

Hedging use cases

CME Group has announced the launch of a north European HRC futures contract based on the Argus assessment for northwest European HRC.

Last year was challenging for the European steel industry, with regional pricing among the lowest in the world, and traders having to try and be creative to make material work. At this moment in time, the launch of the CME Group futures contract is highly welcome. There is pent up demand to hedge, not just from buyers and sellers, but also traders looking to support their physical operation.

A hedging strategy can be used to increase price certainty, thereby reducing the impact of volatile commodity prices on earnings and cash flows. It supports business stability and continuity and can have a significant impact on a firm’s competitive positioning. By fixing revenues and/or costs, hedging can provide creditors with a higher certainty of debt coverage, thereby potentially leading to the offer of more favourable lending terms.

{kind=link}

A futures contract can enable physical market participants to offer fixed prices, and delivery optionality to customers, while hedging their own price risk by taking the opposite position in the paper market. Financial hedging through futures can be an efficient way to manage commodity price risk. It gives market participants a tool to switch from fixed-price risk to a floatingprice exposure, or vice-versa. For intermediaries, it allows them to manage any mismatch between upstream costs and downstream revenues, for example, when a firm’s upstream procurement costs are linked to an index, but the firm’s downstream OEM customers require a fixed-price contract. The flexibility offered by the European HRC futures contract allows for dynamic hedging of commodity price risk for up to 12 months forward, meaning that participants can lock in favourable prices for forward deliverable months.

For firms sitting on inventory, futures markets also provide an efficient way to hedge against adverse price movements. By selling contracts on the paper side, those participants may be able to protect themselves from falling prices impacting the value of their stock.

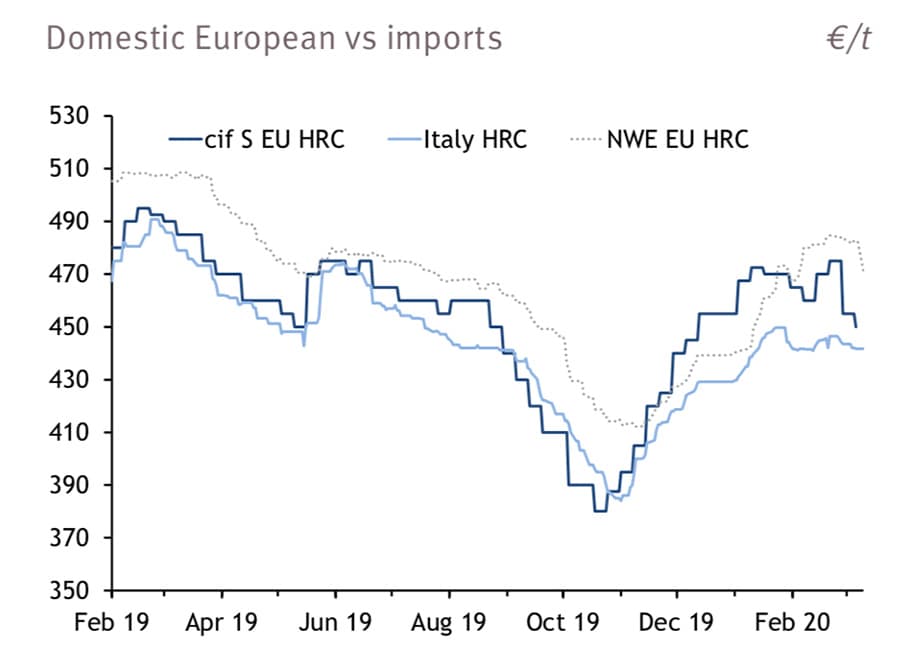

The CME Group contract settles against a monthly average of the daily Argus northwest European price assessments. Owing to its high correlation to Italian HRC and cif Italy prices, it can also be used as a proxy-hedge to manage exposure to prices in these markets. However, participants should be aware that a change in the price difference between those markets could impact the performance of their financial hedge based on northwest Europe HRC.

North European HRC Steel (Argus) futures contract (Commodity Code: EHR) is financially settled, meaning that the physical business is untouched by paper hedging activity. The contract is available for trading on CME Globex, an electronic trading system that provides global connectivity to market participants, and for submission for clearing through CME ClearPort. CME ClearPort provides clearing services for over-the-counter (OTC) markets — it allows for the clearing of transactions negotiated off screen, either directly between counterparts or through specialised OTC brokerages.

Trading exchange-cleared products on CME Group offers the additional safety and security of central counterparty clearing and of anonymous execution. CME Group operates a wellcapitalised and regulated clearing house, CME Inc., which guarantees cash flows to and from buyer and seller, regardless of whether the trades were executed on CME Globex or through CME ClearPort. Positions are risk-assessed daily, and the CME Group clearing house will collect or pay out margins on these positions. The collection of margins is necessary in order to manage and minimise counterparty credit risk.

{kind=link}

Conclusion

In conclusion, price risk management in the European steelmaking industry has long since lagged behind that of more liquid industries, such as parts of the energy supply chain. More recently, European steelmakers have felt the pinch as regional input costs and sales prices have become disconnected from hedging strategies that rely on Asian prices for steelmaking inputs. With CME Group’s launch of this new European HRC hedging tool based on Argus price assessments, the European steelmaking industry should be far better equipped to manage commodity price risk.

If you have any questions regarding the North European Hot-Rolled Coil (Argus) Futures Contract and would like to receive the price assessment as soon as it is released, please contact:

Colin Richardson

Head of Steel

metals-m@argusmedia.com

CME Group Metals Team

metals@cmegroup.com