https://www.cmegroup.com/content/dam/cmegroup/education/images/2019/short-dated-grains_984x137.jpg

{kind=link}

Using Short-Dated Grain Option for Maximum Diagonal Spread

Using Short-Dated Grain Options for Maximum Diagonal Spread Effect

Of the numerous option strategies available, diagonal spread strategies provide one of the most cost-effective ways to address the risk/reward challenge.

Rationale – Gamma Advantage

The basis of the diagonal spread approach is the gamma advantage that the long, closer-to-the-money, front-month option enjoys over the short, further-out-of-the-money, deferred-month option.

This gamma advantage stems from the higher rate of change of the deltas of closer-to-the-money options versus deferred-month, further-out-of-the-money options. A diagonal spread approach seeks to take advantage of this difference between various options gamma by buying a closer-to-the-money, front-month option and selling a further-out-of-the-money, deferred-month option to help finance the purchase of the long side.

This strategy puts the trader in the enviable position of being long an option that may increasingly behave more like an aggressive futures position sooner than the short option will if the market moves in the expected direction.

Short-Dated Grain Options – Enhancing a Diagonal Spreader’s Opportunity

In most cases and markets, diagonal spread opportunities are only available between an option that, ideally, expires within a couple weeks and another of the same underlying futures contract month that will expire in a month or two.

With short-dated options on new crop Corn, Soybeans and Wheat, traders may have an attractive risk/reward opportunity to buy a near-term short-dated option on one of these markets that expires within a few weeks and sell an option on the same underlying futures contract that doesn’t expire until October or November of that year.

The gamma ratios between an option that expires in a couple weeks versus one that doesn’t expire for many months can be extremely favorable and offer grain traders extraordinarily favorable risk/reward opportunities.

This may be the case during the often-times critical February-May period when South American growing and North American planting concerns can raise risk premiums resulting in higher historical and implied volatilities.

Furthermore, diagonal spreads can make it appealing to make a directional trade just before a significant USDA report, such as the upcoming Prospective Plantings report, with negligible risk if the market doesn’t move in the expected direction.

Considering Soybeans for instance, this year’s short-dated options that expire monthly starting in January are based on the new crop Nov19 futures contract.

As of this writing (March 6, 2019) the actual November 2019 options don’t expire for 233 days, until October 25, 2019. By sharp contrast, the May short-dated options based on the Nov19 contract expires in only 51 days on April 26, 2019 and possess much less time premium.

For instance, and with the underlying Nov contract trading at 9.42, the May short-dated 9.60 calls currently trade around 8-1/2 cents while the Nov 9.60 calls are trading around four times this premium at 40 cents. To find a Nov19 call that trades at the same price as the May short-dated 9.60 call, you would have to go all the way out to a 11.20 strike.

This time and gamma discrepancy allows for a favorable risk/reward diagonal spread opportunity where the vast differences in gamma are exploited in exchange for theta (time decay) risk, that is typically negligible.

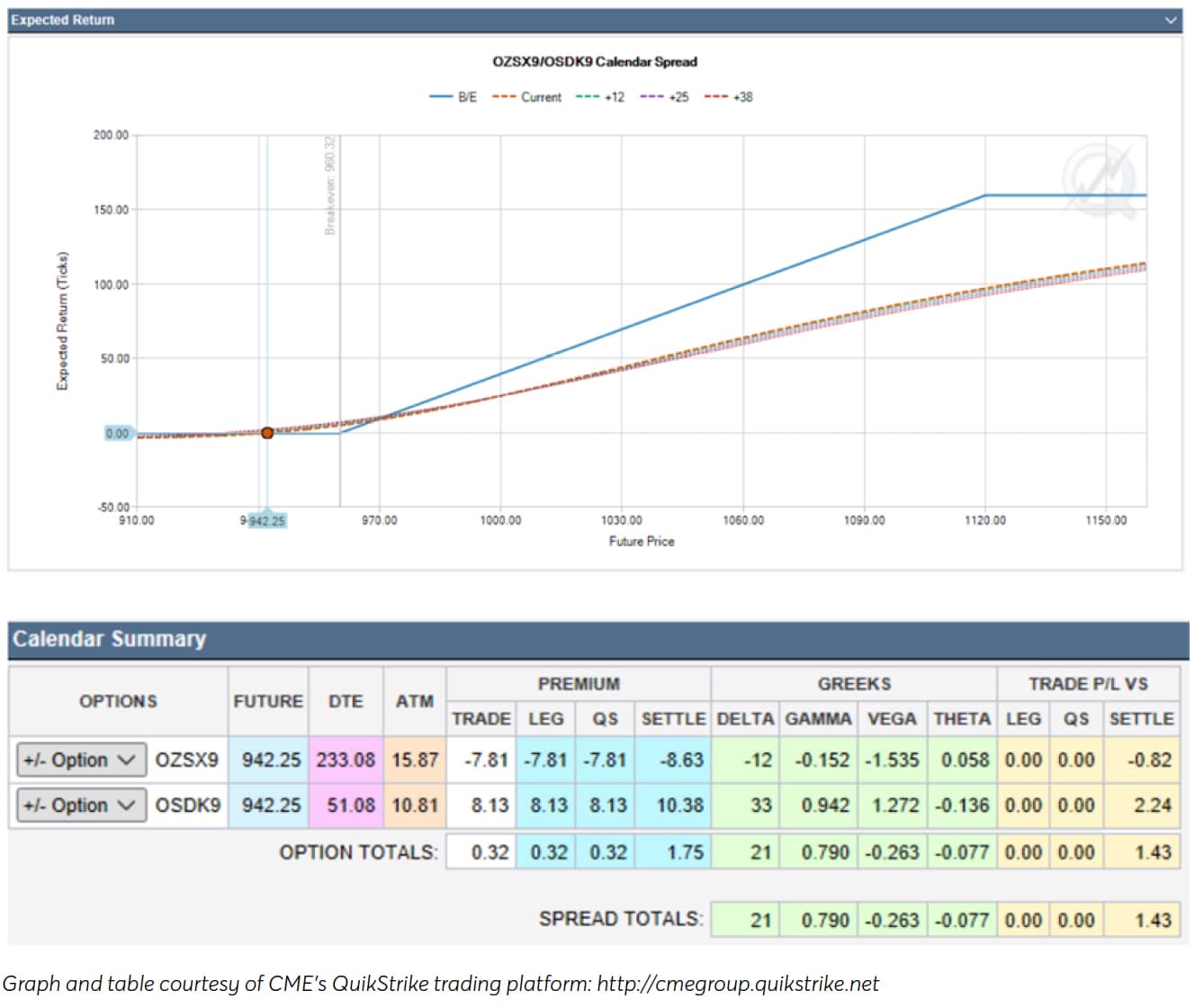

Bullish Soybean Example: May Short-Dated 9.60 Call / Nov 11.20 Call Diagonal

This diagonal spread involves buying the May short-dated 9.60 call for around 8-1/2 cents and selling the Nov 11.20 call for around 8-1/2 cents for a net cost of even. The gamma ratio between these two calls is 6:1 as the delta of the way-out-of-the-money Nov 11.20 call is only -12. By contrast, being only 18 cents away from going in-the-money and behaving like a futures contract, the delta on the May 9.60 calls is +33, producing a net delta for the spread of +21.

The Profit & Loss (P&L) graph of the May short-dated 9.60 / Nov 11.20 call diagonal approach is shown below. This is a bullish approach betting on a sharp, perhaps Prospective Planting report--driven spike around an acute technical setup. If a bullish call proves to be wrong and the underlying Nov19 futures contract declines sharply, the risk to this approach is negligible. If, alternatively, the market rallies sharply, the pay-off can be significant with a theoretical profit potential of $1.60.

{kind=link}

Bearish Soybean Example: May Short-Dated 9.20 Put/Nov 8.20 Put Diagonal

Applying this same diagonal spread approach to a bearish approach for example, one could buy the May short-dated 9.20 put for around 7 cents and sell a Nov 8.20 put for around 7 cents for a net cost of even. The net delta on this spread is -16 while the gamma ratio between these two puts is about 5:1.

The P&L graph of the May short-dated 9.20/Nov 8.20 put diagonal example is shown below. This approach is betting on a sharp, perhaps crop report-driven decline around an acute technical setup. If a bearish call proves wrong and the underlying Nov19 futures contract rallies sharply, the P&L graph shows the risk to be negligible. If the market declines sharply per the intent of this approach, the profit potential is very favorable indeed at up to $1.00.

{kind=link}

Managing Diagonal Spread Risk

If the market doesn’t trend in the direction for which a diagonal spread is established, there are basically two results or risks that must be addressed and managed: one that is negligible and one that could be significant, but can be easily managed.

If the technical setup and/or economic report produces a market move in the opposite direction of the intended diagonal approach, it could be assumed that the long, high-gamma, high-theta option will probably deteriorate to zero quickly.

However, the risk of the remaining short, deferred-month, further-out-of-the-money option that then would be getting even further out-of-the-money is negligible.

In this situation the approach can either be maintained until the short option eventually erodes to zero if it looks like the trend is extending the opposite way, or the entire spread can be covered for what will likely be a small loss on the overall trade.

The most adverse result to this approach is lateral, stagnating price action in the underlying contract. If the market doesn’t move sharply in the expected period of time, then the long, high-gamma, high-theta option that is intended to profit from market direction will erode at a faster rate than the deferred-month short and may expire worthless.

With the broader trend still intact, the eventual remaining, naked short option position ultimately poses unlimited risk. Understanding this, some traders may opt to consider covering the short side of the trade for a small loss with three or four days left to expiration of the long option.

If the market moves sharply and profitably in the expected direction, the trader is in a favorable position and can either cover the trade and take profits, exercise the long portion of the spread in what would become a futures position while maintaining the short side of the approach, or simply roll the long side of the spread up (in the case of a call diagonal) or down (in the case of a put diagonal).

Implementation

Theta is a drag against long gamma plays, as it is highest for high-gamma, around-the-money options that are nearer to expiration. Add to the equation that gamma ratios between two options will be at their widest in the final expiration days of the front-month option where time decay accelerates, quick confirmation or total negation of an expected directional move in the underlying market is preferred.

As shown above, short-dated options can allow traders to buy a long position with a month or two to expiration and sell the Nov Soybean options and still create a large gamma ratio advantage.

Establishing diagonal spreads in most markets with about a week or two to expiration and around a critical technical condition and/or the release of a USDA report may provide ideal circumstances for a favorable risk/reward opportunity.

Short-dated options on new crop Soybeans, Corn and Wheat contracts can provide a gamma advantage during the critical and often volatile period between February and May with U.S. spring planting considerations and into the summer months of June through August when both historical and implied volatilities typically increase.