{kind=link}

Using Futures to Hedge EU Soybean, Soymeal Imports & Crush

EU imports of soybeans, including U.S. origin, are on the rise. The EU is projected by the USDA to import 15.8 million tonnes of soybean in 2018/19. Alongside this, EU production of soymeal is forecast to hit 13 million tonnes in 2018/19, with a further 18.5 million tonnes of imports. With increased soybean and soymeal imports and usage, comes increased exposure to risks. CME’s Soybean and Soymeal futures are uniquely positioned to provide effective hedging tools to mitigate the associated bean and meal price risks.

Data Analysis

EU soybean and soymeal import prices and CBOT front month futures daily settlement prices are used to evaluate correlations for 2 years up to Sept 2018. Daily exchange rate adjustments reflect values in U.S. dollars per metric tonne (USD/MT):

Import Cash Price Series

- CIF Rotterdam U.S. Origin Soybeans

- Hamburg Soymeal 44% HIPRO

- Hamburg Soymeal 48% HIPRO

CME Front Month Futures Settlement Price Series

- CBOT Soybeans

- CBOT Soybean Meal

Hedge Effectiveness (R2) is the variation in cash commodity price explained by the futures price, or more simply, how much price volatility or price risk is diminished when using a futures contract to hedge against movements in cash prices.

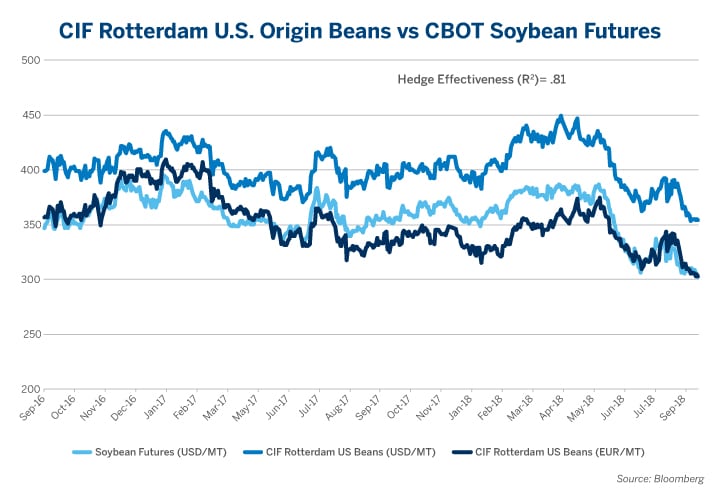

Soybean Hedge Effectiveness

{kind=link}

The analysis shows that CBOT Soybean futures prices are highly correlated with the CIF Rotterdam U.S. cash soybean import price, and therefore are a very useful hedging mechanism with a hedge effectiveness equal to 0.81. This suggests, using the CBOT Soybean futures, a soybean importer can expect a reduction in price risk of over 80 percent for CIF shipments of U.S. origin beans to the port of Rotterdam.

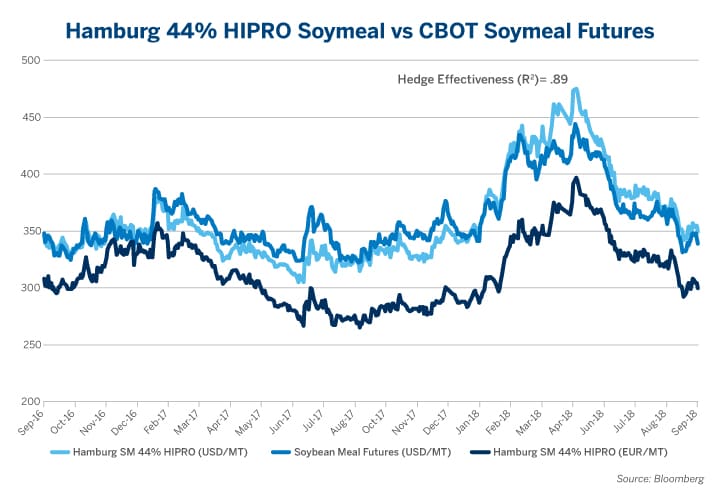

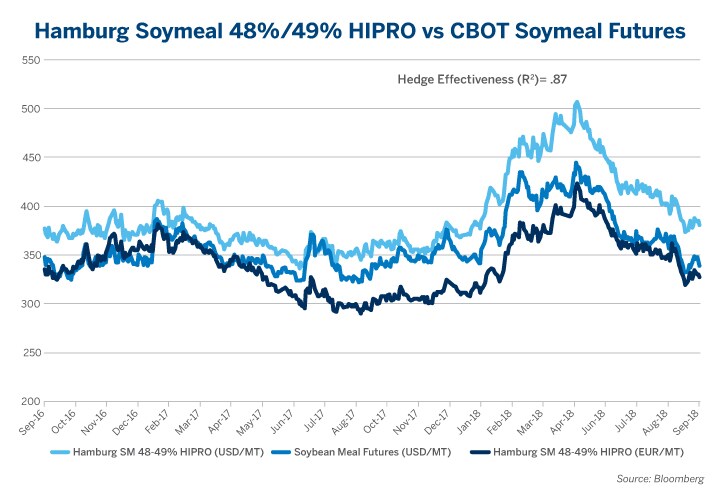

Soymeal Hedge effectiveness

{kind=link}

{kind=link}

According to the analysis, CBOT’s Soymeal futures are an ideal mechanism to hedge the price risk associated with EU soymeal importation and domestic production. With a hedge effectiveness of .87 for 48/49 % HIPRO and .89 for 44 % HIPRO versus Hamburg cash soymeal prices, EU compound feed manufacturers for example can reduce their price risk up anywhere from 87 to 89 percent by hedging their soymeal feedstuffs with CBOT Soybean futures.

Summary

The paper shows several EU soybean and soymeal cash markets which can be effectively hedged using existing CBOT Soybean and Soymeal futures contracts. All of these markets, especially the Hamburg 44 HIPRO Soymeal, showed great benefits in the utilization of CME futures in helping offset and mitigate the inherent price risk of the markets.

CME’s Soybean complex offers some of the deepest liquidity of any futures market, allowing buyers and sellers to enter and exit the market readily, and thus makes these products a must have in any hedgers portfolio of risk management tools.

For further information on CME’s Soybean and Soymeal futures and options contract, please go to https://www.cmegroup.com/trading/agricultural/grain-and-oilseed.html.