{kind=link}

Use case: EUR/USD data on the FX Market Profile

Use case: Using the FX Market Profile Tool to examine the EUR/USD markets

CME Group’s FX Market Profile (“FXMP”) tool is now enhanced to offer more data across the cash and futures foreign exchange markets in order to enhance participant decision making. The tool combines data from the EBS spot FX markets and CME FX futures to enable traders to analyze the activity within the FX market across 18 currency pairs.

With the FX Market Profile, traders can gain insights into:

- Where is the top of book spread, how does it differ between markets, and how does it change over the course of the day

- What time of day is each marketplace most active and when might it be the most efficient to execute orders

- How much liquidity is there available at top of book, and how does this extend across ten levels

- How has the liquidity profile changed over set time periods up to 6 months

Below, we focus on EUR/USD in order to provide some concrete examples of the data and analytics available within the FXMP tool.

The enhancements in version 2 of the FXMP tool includes the addition of FX Link data, 7 additional currency pairs, actual futures volume data (in both contract and notional terms), and the ability to conduct historical liquidity analysis. The core of tool, which offers a comparison of the liquidity in OTC Spot FX (from EBS Markets) and CME FX futures has been extended to show information on the orderbook depth in these markets out to 10 levels.

Given these enhancements, the FXMP tool now has three main tabs – ‘Cash Futures Analysis’, ‘FX Link – Futures’, and ‘Historical Analysis’. Whilst this paper will highlight some of the analytics from each of these three tabs in turn, there is a wealth of other data and functionality within the platform – including the ability to download the data in to excel or CSV formats with up to 5 minute granularity.

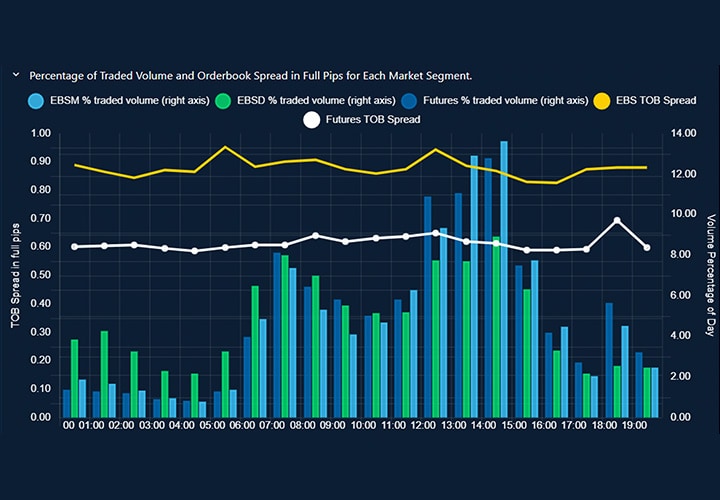

Looking at the Cash Futures Analysis for June 2021, the first chart presented is an analysis of the distribution of traded volume and bid-ask spread.

{kind=link}

Time on the charts are shown in unadjusted GMT and the volume percentage of day represents the % traded in that hour for each liquidity venue i.e. it does not show the relative market share. The distribution for EUR/USD shows the higher level of activity across both OTC and listed FX markets to be during the London trading day (7:00 GMT to 16:00 GMT), and in particular, during the crossover period between London and New York (12:00 GMT to 16:00 GMT). What is also shown is that on the EBS Direct platform, more activity is skewed towards the APAC session than on other platforms – suggesting traders based in the region and/or trading this time-zone should make sure to consider pricing from EBS Direct on a relationship basis when planning a trade, driven by its unique exposure to large regional banks in that region.

The top of book (“TOB”) spreads for both EBS Market and CME futures are consistent throughout the trading day, and whilst Futures (the white line) are inside OTC Spot FX (the yellow line) for the whole day, traders should also consider what amount of liquidity is immediately available at this spread. i.e. TOB Spread data is not volume weighted.

The FXMP tool enables traders to not only see the TOB depth in both markets, but also to see how the order books develop (in both depth and spread) over multiple levels all the way out to ten levels deep.

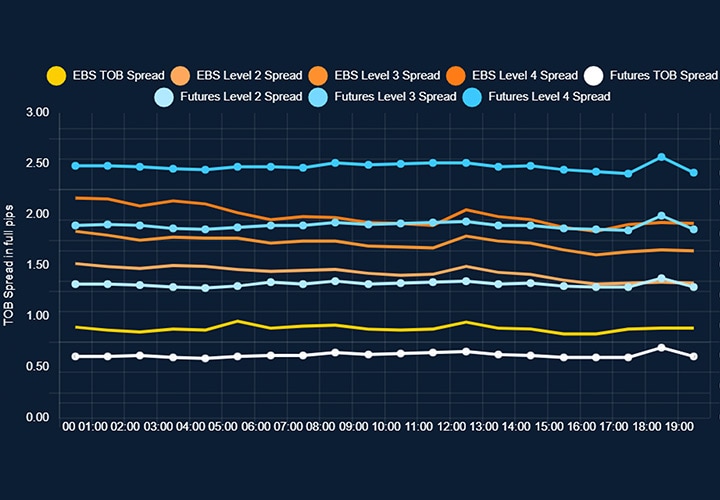

The chart of the spread widths for the top 4 orderbook levels for EUR/USD in June 2021 is as follows.

{kind=link}

At the top of the book, outright FX futures have the tightest pricing (white line), at an average of around 0.6 pips. However, deeper in the book, EBS shows comparatively tighter pricing (as evidenced by the orange-colored lines lower on the axis).

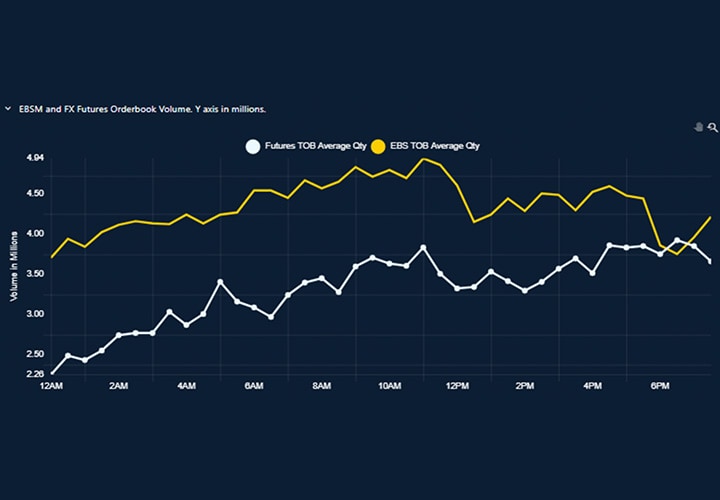

This is in part due to the larger size available on EBS Market. Available orderbook order volumes are highlighted on Chart 3 below. For the top of book, futures order size is low and rising through the trading day, while EBS Market order size is consistently high. Typically, around 33% more volume is available on EBS at the top of book until later in the day.

{kind=link}

Traders seeking immediate fills for larger size orders may prefer the larger size available on EBS Market, whilst many customers using FX futures will typically work an order or use an algo to break a larger trade down in to smaller constituent parts.

The FXMP tool now provides order book data along with transacted volumes for FX Link. FX Link is an all-to-all central limit orderbook for the spread or ‘basis’ between OTC spot FX and CME FX futures. As such, FX Link can be described as a liquid and transparent pool of cleared liquidity for FX swaps that is underpinned by ‘hard’ credit, enabling firm pricing with no last look.

With the inclusion of FX Link data, traders can now better see the relationship and interplay between OTC spot FX, the spot / futures basis, and CME FX futures and with granularity down to five-minute intervals throughout the trading day.

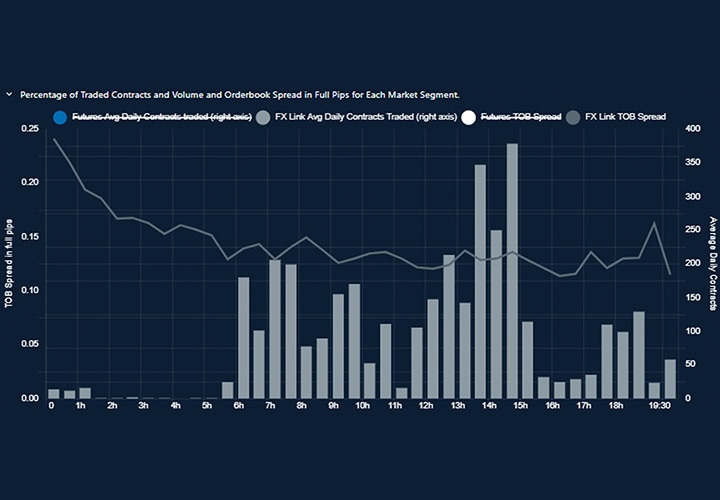

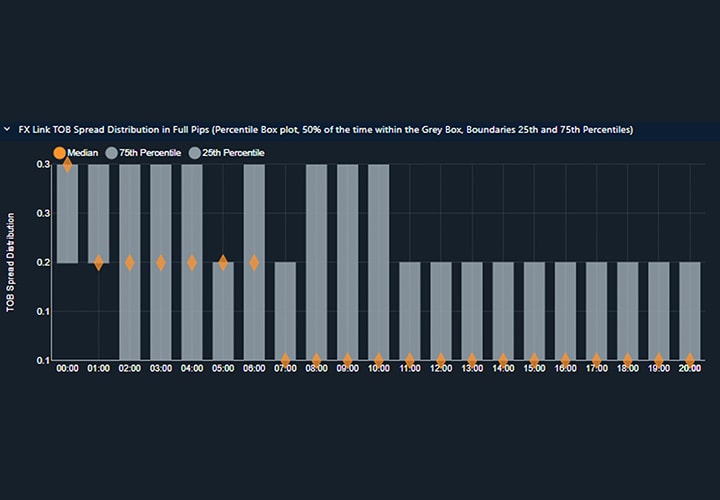

For the month of June 2021, the intraday profile of TOB spread and traded volume in the EUR/USD FX Link market is as follows.

{kind=link}

EUR/USD FX Link activity is clearly focused on the London and New York trading sessions (6:00 to 16:00). During these times, the average spread is around 0.12 pips. Further detail on the TOB spread is shown in the FX Link TOB Spread Distribution in Full Pips box whiskers chart, which shows the distribution of the TOB spread, highlighting the median spread and the 50th percentile range between the 25th and 75th percentiles.

{kind=link}

With the median spread at 0.1 pips during the bulk of the trading day – the tightest available – this means that at least half the time the market is at a 0.1 pip spread. This spread data needs to be considered in the context that the bulk of the activity in FX Link is typically OTC Spot versus the front quarterly contract, which means that the contract starts off as akin to spot versus a three-month forward FX swap, which gradually then reduces in maturity as the futures contract approaches its expiry.

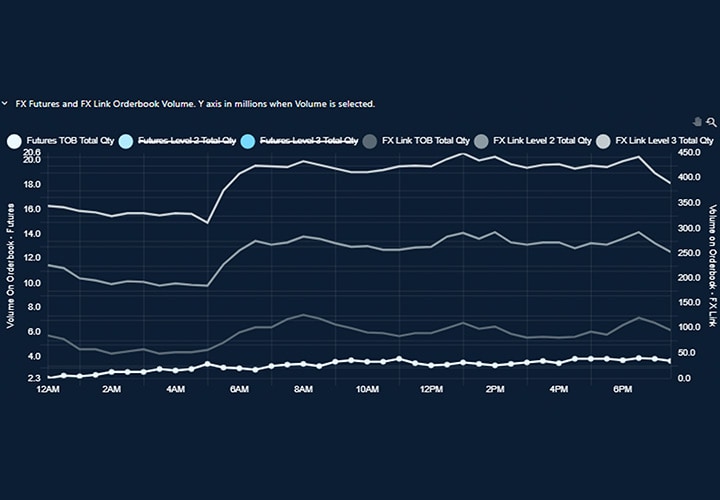

The orderbook size for EUR/USD FX Link and outright futures during June is shown below. This shows a typical TOB size for FX Link of around $90 million. Whilst this can be compared to the TOB size for futures of around $3.5 million, it must be remembered that the price volatility for the FX Link spread is considerably lower than the outright.

{kind=link}

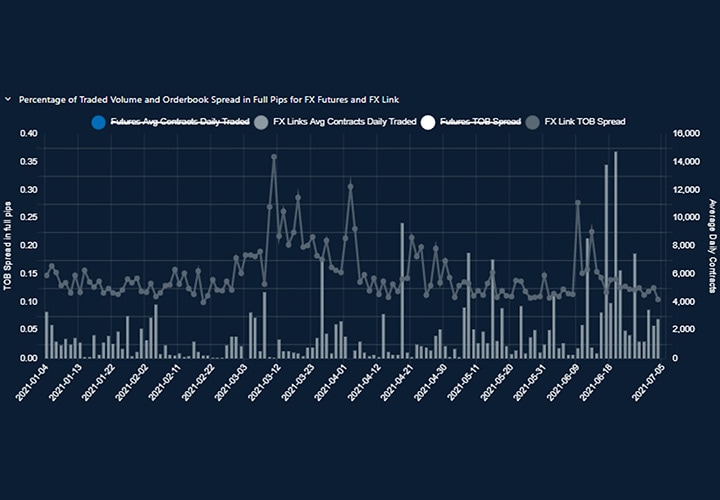

The historical chart for FX Link adds more colour to the data. This shows that spreads widened slightly in March around the time of the futures roll, but have since returned. This chart also shows increasing trading activity in FX Link during the month of June.

{kind=link}

New to this version of the FXMP Tool is the historical analysis tab. The user can choose to see either daily, weekly, or monthly averages over a historic period of up to six months, which enables traders to see how liquidity and volumes have changed (or remained constant) over their chosen time horizon.

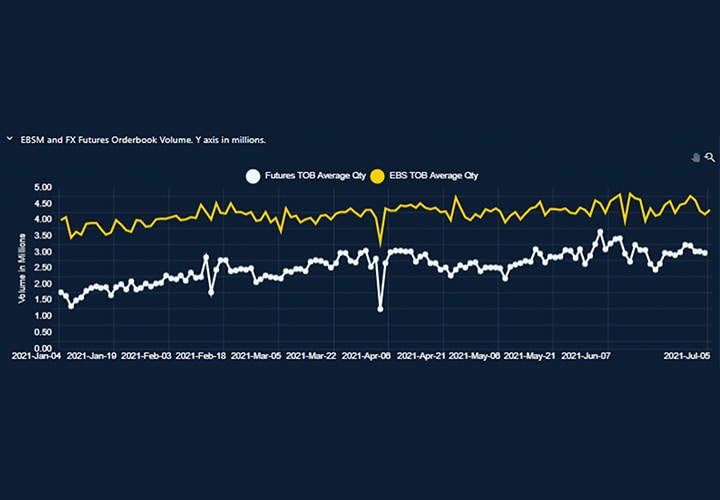

Looking at top of book volumes in particular, there has been a growth in orderbook volume for EUR/USD in both EBS Markets and CME Futures, with futures seeing the greatest rate of growth rising from around $1.8 million at TOB in January to $3.0 million in June. EBS Markets has risen from $3.8 million at TOB in January to $4.5 million in June.

{kind=link}

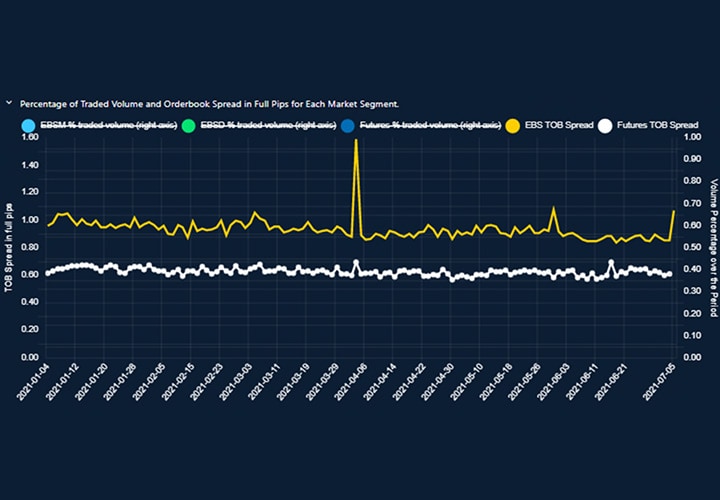

The historical analysis also shows how the average top of book spreads have improved over the period, particularly on EBS Market (yellow line), where the TOB spread has reduced from around 1.0 pip in January to nearer 0.85 pips in June.

{kind=link}

Combined with the data on orderbook size this indicates substantial improvements to liquidity on the central limit orderbook venues in the first half of 2021.

Bottom Line

The FX Market Profile tool contains insightful data from the EBS and CME FX futures markets that can help inform execution decisions. The tool includes data for 18 currency pairs, 10 levels of market depth, and can be configured to view a wide variety of time frames.

The above analysis provides a snapshot of EUR/USD liquidity and activity during the month of June 2021. The data from the FX Market Profile tool visualises the quality of the markets in both OTC spot FX and FX futures, and helps to illustrate that these two market places offer complementary liquidity that can be accessed and used in different ways depending on the currency pair, size of order and time of day to trade.