{kind=link}

U.S. Petrochemical Market Highlights

America’s chemical industry has undergone a dramatic transformation from high to low-cost producer as petrochemicals derived from crude oil and natural gas have seen a resurgence of capacity additions and investment over the last five years. 2017 was marked by growing US capacity in natural gas liquids (NGLs), primarily ethane production, and continued exports of propane and ethane to markets in China, India and Europe.

Petrochemicals currently make up 25% of the demand for liquid petroleum gases (LPG).1 The US is becoming one of the largest producers of petrochemicals, accounting for 30% of global production in 2017. Continued global demand for plastics and polymers in the form of resin, coupled with low feedstock prices, has contributed to increasing investment in propane dehydrogenation (PDH) units in China, and ethylene crackers in the US.

NGLs, which include pentanes, ethane and LPG (propane, butane) accounted for 29% of the liquid fuels growth between 2009 and 2016. Most growth in NGL production occurred at natural gas processing plants. A byproduct of growing supply of natural gas from shale and tight oil formations.2

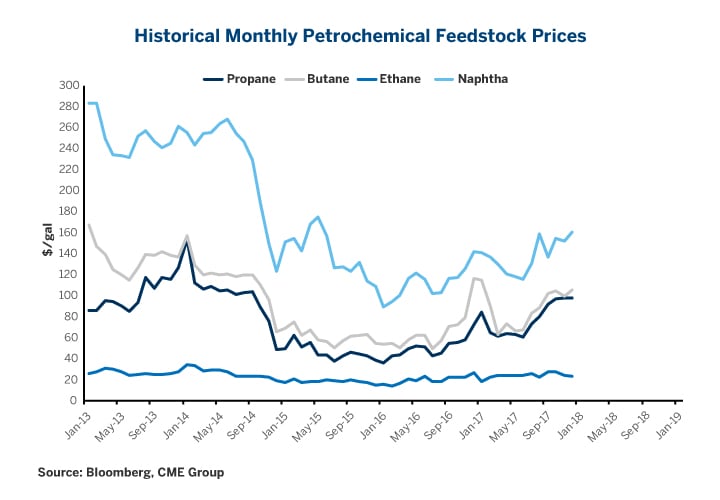

Prices rallied over the summer of 2017 in butane, propane, and naphtha, collapsing the US-to-Asia arb in propane as prices became more competitive in the US versus China. Ethane prices were attractive relative to the other liquids, and it remained the “light” feedstock of choice when compared to propane.

{kind=link}

Globally, LPG is oversupplied with production between 300-310 million tons. On the demand side, the world requires about 290 million tons.3

India is now the second largest consumer of LPG world-wide. New government subsidies have increased consumption by 10-11 million tons in the last three years. India’s total consumption is approximately 23 million tons, with half of the demand met by local supply, and the balance met by imports of 12 million tons a year. India has become an important market for excess US and Middle East supply.4

China is the largest consumer of LPG, and a large importer of US propane, as local supply specs are not suitable for PDH units there. While propane prices were higher, and the market has seen margin tightening, running PDH units was still economic in 2017.

According to the Energy Information Agency’s (EIA’s), Short-Term Energy Outlook, ethane production is expected to increase from 1.25 million b/d in 2016, to 1.7 million b/d in 2018.5 One of the challenges with ethane as a primary feedstock is that ethane only produces ethylene, while propane and naphtha products can be more diverse. This dynamic has created a near-term shortage of propylene, which is used in over two-thirds of automobile plastics.6

New ethylene capacity, as forecasted in the chart below, will absorb some ethane supply. The first ethane cargoes were sent to Europe in 2016, and last year marked the first-time cargoes were headed to India. EIA forecasted exports to increase by 180,000 b/d from 4Q16 to 1Q18.7 Given the massive quantities of natural gas available in the Permian Basin, Utica, and Marcellus shale plays, it is expected that ethane exports will continue.

| North American Ethylene Capacity Growth | |||

| Starting | Company | Location | Total Growth* |

| Q1-17 | Dow | Plaquemine, LA | 250 |

| Q2-17 | Equistar | Various sites | 401 |

| Oxy/Mexichem | Ingleside, TX | 550 | |

| Q4-17 | ChevronPhillips | Cedar Bayou, TX | 1,500 |

| Dow | Freeport, TX | 1,500 | |

| Q1-18 | ExxonMobil | Baytown, TX | 1,500 |

| Q3-18 | Indorama | Lake Charles, LA | 420 |

| Q4-18 | Formosa | Point Comfort, TX | 1,150 |

| Q1-19 | Shin-Etsu | Plaquemine, LA | 500 |

| Sasol | Lake Charles, LA | 1,550 | |

| Q1-20 | LACC | Lake Charles, LA | 1,000 |

| Q2-22 | Shell | Monaca, PA | 1,500 |

| Total Additions | 11,821 | ||

*1000 metric tons

source: IHS Markit

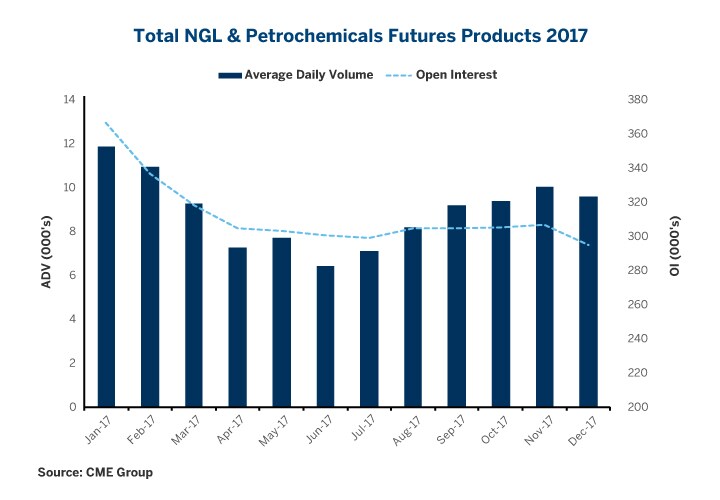

Looking ahead into 2018, CME Group expects volumes to increase in its NGL and petrochemical futures contracts given better 2H17 volume growth. As the market matures, the Exchange expects more participants to implement risk management strategies into their portfolios. With over 50 NGL and petrochemical trading products, more participants are utilizing CME Group contracts to hedge price risk.

{kind=link}

The outlook in 2018 for petrochemical end-markets overall should be positive, with continued growth in downstream applications, such as plastics, synthetic rubbers, including manufactured fibers like nylon and polyester.

Demand for these products tends to grow alongside GDP growth.8 As economies improve and consumers demand more choices, plastics, for example, will not only need to increase in volumes, but innovation, as the global food trade will require improved freshness over long hauls to new markets. Investment in infrastructure and crackers enables markets to develop with added capacity and feedstock supply to meet this growing demand.

North America, as a major exporter and producer of NGLs, is redefining supply-chains and shipping channels worldwide. Ultimately these movements may introduce new markets, new participants, and as a result continue to offer new trading opportunities in 2018 and beyond.

- Argus Consulting: http://view.argusmedia.com/rs/584-BUW-606/images/Argus looks ahead with new LPG analytics service - WLPGA July 2017.pdf

- https://www.energy.gov/sites/prod/files/2017/12/f46/NGL Primer.pdf

- IHS Markit http://www.lpgc.or.jp/corporate/information/program1_keyspeach.pdf

- Ibid

- https://www.eia.gov/todayinenergy/detail.php?id=29572

- https://www.icis.com/resources/news/2007/11/06/9076455/propylene-uses-and-market-data/

- https://www.eia.gov/todayinenergy/detail.php?id=29572

- https://ec.europa.eu/energy/sites/ener/files/documents/OPEC presentation.pdf