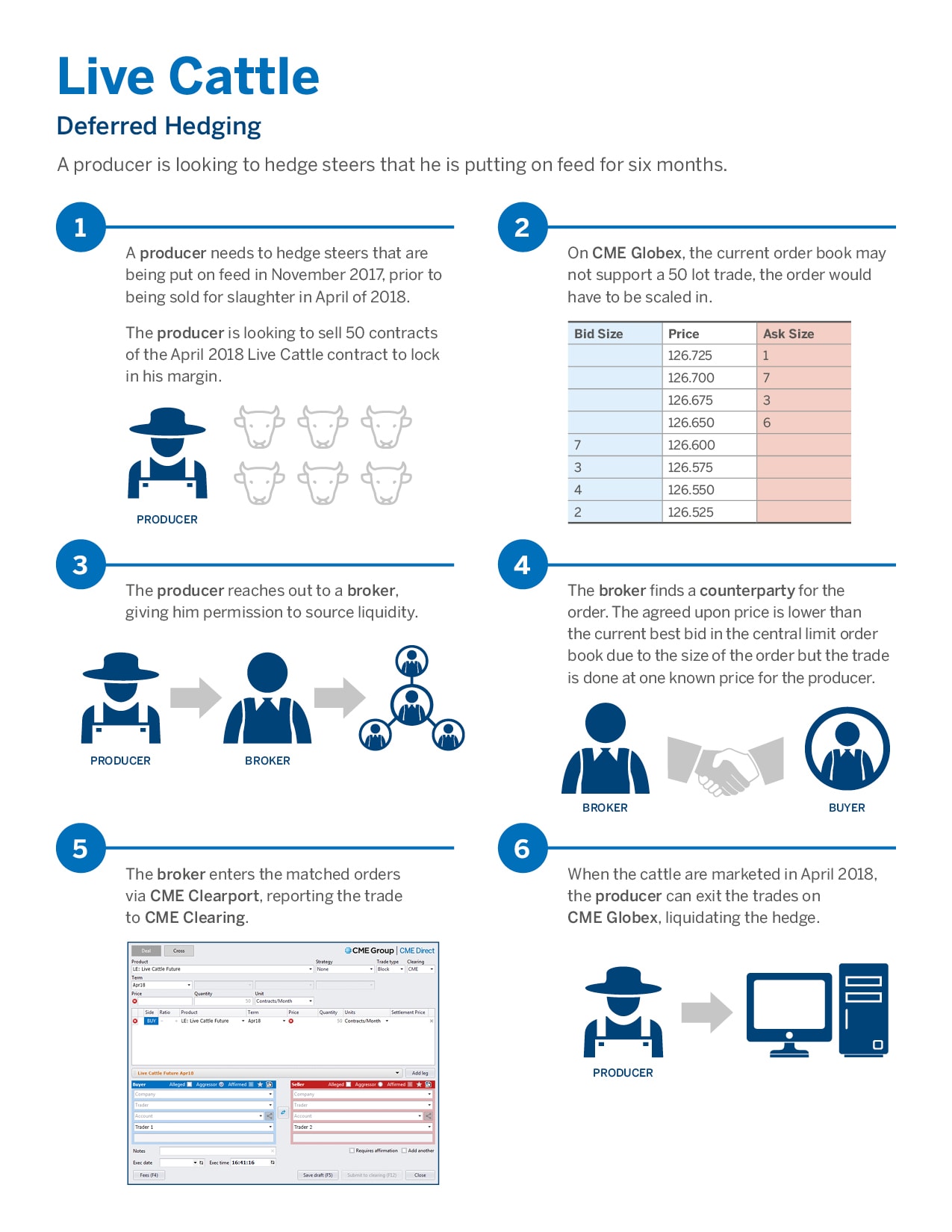

{kind=link}

Understanding Block Trades

What are Block Trades?

Block trades are privately negotiated futures, options or combination transactions that are permitted to be executed apart from the central limit order book (CLOB) or the pit and are subsequently submitted to CME Clearing via CME ClearPort or CME Direct. Block trades must be submitted to CME Clearing for price reporting purposes within a prescribed time after execution.

Rule 526 (“Block Trades”) governs block trading in CME, CBOT, NYMEX and COMEX products. Block trades are permitted in specified products and are subject to minimum transaction size requirements which vary according to the product, the type of transaction and the time of execution. Block trades must be transacted at prices that are “fair and reasonable” in light of the size of the transactions, prevailing market prices in the futures and other related markets, and other relevant circumstances.

Block trades offer large commercial firms and institutional traders the convenience of privately negotiating a futures or options transaction with a select eligible counterparty. In particular, institutions often seek to execute large transactions at a single price while enjoying the benefits imparted by the financial sureties associated with the CME centralized counterparty (CCP) clearing system.

Once executed and cleared, the resulting futures/options contract is indistinguishable from any other futures/options transactions recorded in that product. Thus, these transactions may subsequently be liquidated by an offsetting transaction executed through more conventional means such as the CME Globex electronic trading system or in a pit via open outcry

The Exchange imposes certain restrictions on block transactions. Only “Eligible Contract Participants” or ECPs are permitted to transact blocks. ECPs may generally be thought of as exchange members and member firms registered as floor brokers and floor traders, broker/dealers, government entities, pension funds, commodity pools, corporations, investment companies, insurance companies, depository institutions and high-net worth individuals. The qualifications are formally defined in Section 1a(18) of the Commodity Exchange Act (CEA).

Block Trades for Agricultural Products

In the past, CME Group allowed block trades for most asset classes. Agricultural products, however, were an exception. More recently, customers have requested more efficient ways to trade less liquid options and back-month futures. As a result, CME Group is planning to offer block trades for agricultural products beginning on January 8, 2018.

Generally speaking, markets with high liquidity have higher minimum block thresholds and shorter reporting times. For example, Corn futures, the most liquid grain market, will have a 300-contract block threshold during regular trading hours and a 150-contract block threshold during European and Asian trading hours. Corn futures block trades must be submitted to the Exchange within five (5) minutes of execution. As a contrast, Rough Rice futures, a market not as liquid as corn, will have a block threshold of 10 contracts during regular trading hours and a block threshold of 5 contracts during European and Asian trading hours. Rough Rice futures block trades must be submitted to the Exchange within fifteen (15) minutes of execution.

How to Transact?

A block trade may be transacted at any time and at any fair and reasonable price agreed upon by the two counterparties. Two customers transacting a block must have the resulting futures/options position(s) subsequently submitted to CME Clearing via CME ClearPort or CME Direct.

More commonly, however, a customer establishes a relationship with a broker who is able to make a market, i.e., shows a bid and an offer, in the particular instrument in question. There are a variety of firms which may make markets in blocks although the Exchanges assume a neutral posture and do not offer recommendations in this regard. After the trade is executed, the futures or options position must be reported to CME Clearing via CME ClearPort or CME Direct. Access to CME ClearPort and CME Direct requires registration. Additional information on access to CME ClearPort and CME Direct is available here: CME Direct / CME ClearPort.

CME Group has implemented a registration process in order to provide firms with market maker contact information for the purpose of engaging in block trade negotiations.

Who Trades Blocks and Why?

Block trades are generally executed by large commercial firms and institutional traders with particular purposes in mind.

Block trading is often practiced by institutions with large lot sizes to transact. Frequently, these institutional traders may prefer block trading over execution in a pit or via the CME Globex electronic trading system to ensure that the transaction is executed at a single price. In other words, a participant may be concerned about the prospect that a large size order entered into the CME Globex electronic trading system may be executed in smaller increments at multiple prices. Thus, the decision to trade blocks is frequently driven by an assessment of marketplace liquidity relative to the size of one’s order.

There are many ways to measure liquidity, notably including the “depth of book” and order size. Liquidity typically ebbs and flows as a function of market volatility. But CME Group markets generally offer tremendous depth. As a result, conventional execution methods are generally more than sufficient to address normal demand for liquidity. Thus, for most block-eligible products, we tend to find that the volume and the number of transactions executed via block trades tends to be small relative to the total volume and number of transactions. Also, the average size of a block transaction is quite high relative to the average transaction size for most block eligible products.

Value of Transparent Pricing

Block trades are allowed by the CME Group Exchanges as an accommodation to traders who find this a convenient and expeditious way of conducting business. They are not intended to represent the mainstream way of trading. Rather, the Exchanges expect that the plurality of trading of agricultural products will be conducted in the Exchanges’ open, competitive trading venues – via open outcry or on CME Globex. Price discovery represents a primary function of futures markets. Thus, it is important to promote a transparent trading venue as the primary trading venue where values may readily be referenced. Liquidity being a necessary prerequisite for the efficient discovery of equilibrium prices will unlikely divert any significant volume of trade from the mainstream competitive marketplace for agricultural products. In fact, only a small proportion of volume is transacted as blocks in most other asset classes. Still, blocks often represent a useful and convenient outlet for some traders and, therefore, remain consistent with the Exchange’s mission of providing customers with an efficient source of price discovery as well as hedging utility.

{kind=link}