{kind=link}

Understanding and Analyzing Year-End Effects in the FX Swap Market

Responding with FX Link

Get ready for the turn

FX swap activity that bridges from one calendar year to the next is sometimes described to be including “the turn” or trading “the turn”. The end of the year typically sees a bump in funding rates as cash is repatriated and applied to corporate and banking balance sheets. While this is true around the world, the demand for U.S. dollars over this period is often hugely more pronounced – creating strong supply and demand forces that impact FX swap pricing, potentially taking market prices away from where the interest rate differentials suggest they should be.

Get a clear view

Given the largely OTC nature of FX forwards and FX swaps, clients are typically somewhat reliant on prices obtained from their dealers to help form a clear picture of where the market is trading. Tools such as the CME Group FX Swap Rate Monitor can act as a complement to bilateral dealer relationships to provide firm, transparent and credit-agnostic pricing for FX swaps as well as a clear view about where the market currently believes the implied interest rate differentials to be. This freely available data can assist clients in identifying potential investment opportunities and optimizing their trading activity.

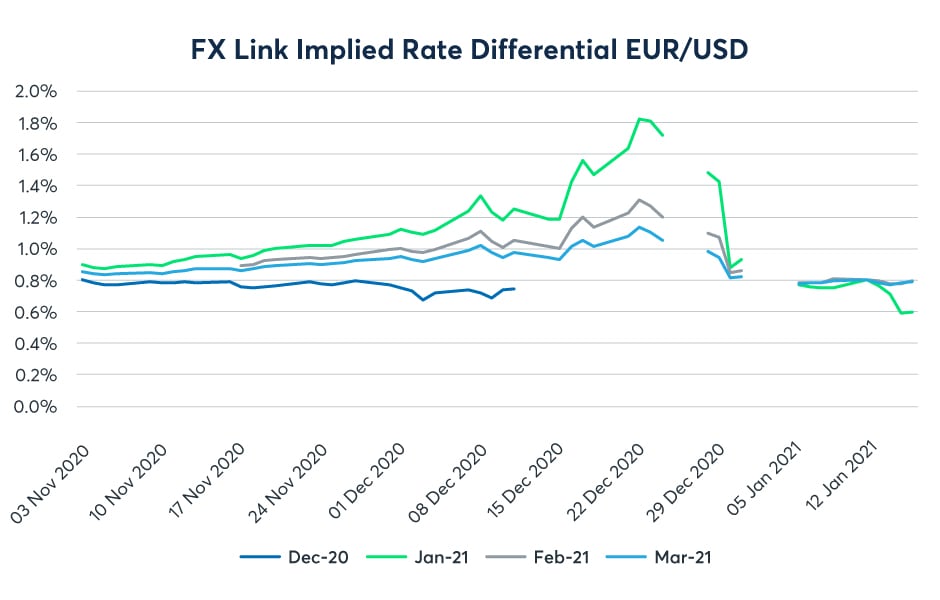

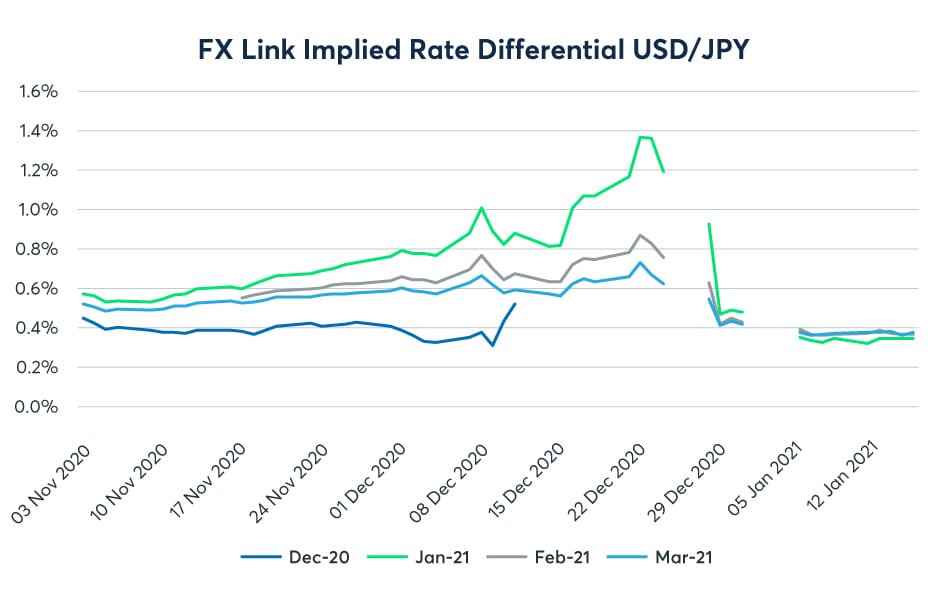

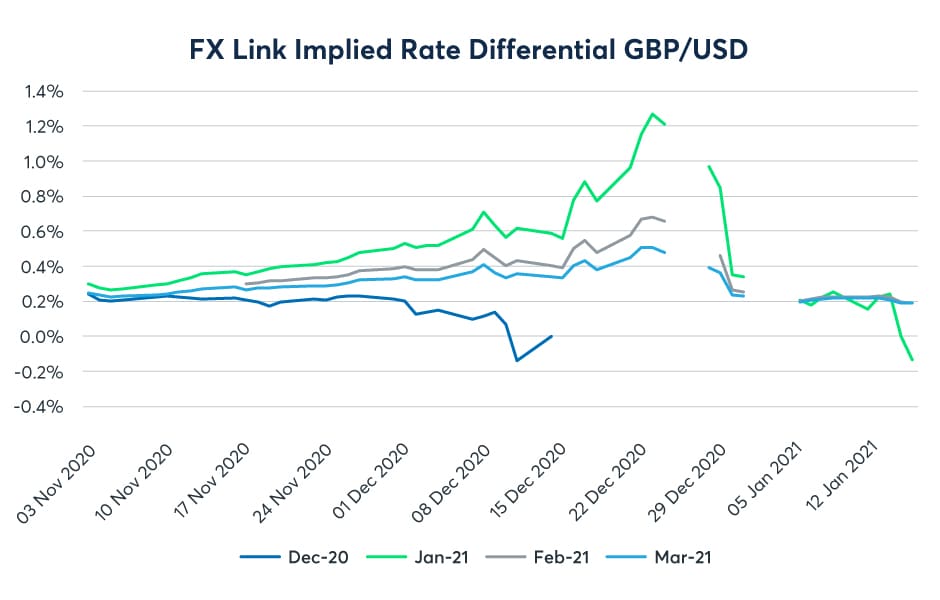

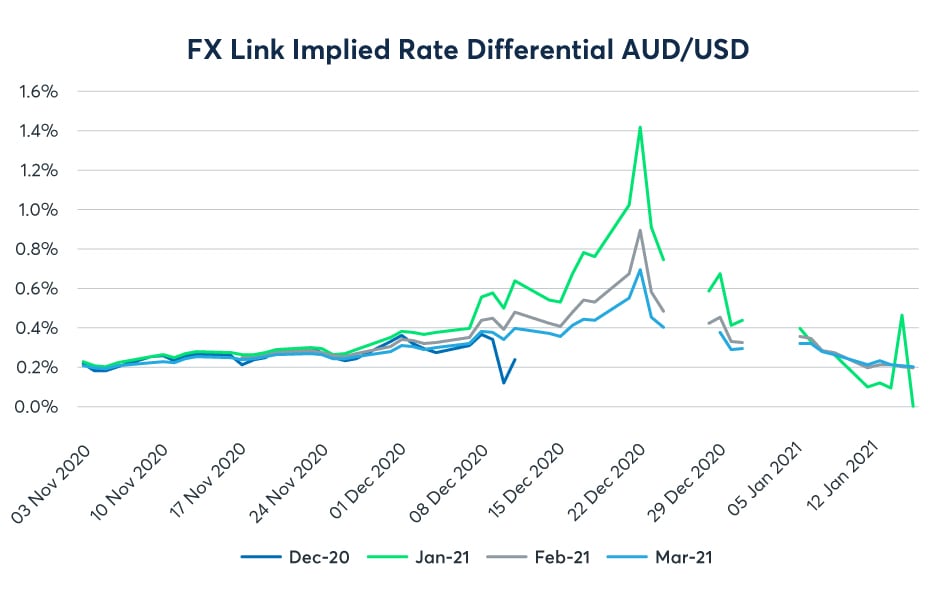

CME FX Link is the spread between OTC FX spot and listed FX futures traded on the CME Globex electronic platform. As such, it provides a cleared, all-to-all and firm liquidity pool for managing FX swap risk in eight currencies. Prices in this market reflect the differential in interest rates in the currencies for the period to expiry of the futures contract, as well as include any overarching supply and demand factors in the wider market. Differentials quoted by the FX Swap Rate Monitor are the amount the implied USD interest rate exceeds the implied interest rate of the other currency.

Looking at the data for the past two year ends, there is a decisive bump in rate differentials over the year end. A similar uptick is not seen at the other quarter ends during the year. Looking at the data from the FX Swap Rate Monitor over a period of time shows the extent to which the end of year has an impact on funding costs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Source: All charts CME Group, November 2021

There are several points that can be made from this analysis – for which investors should be ready.

Impact on USD funding

Firstly, while there is likely to be a desire to hold cash across the year end in all currencies, the change in the implied rate differential shows how much more significant the impact is for U.S. dollar funding. Charts for all eight currencies in the FX Link system show an increase in the rate differential favoring the U.S. dollar. The rate differential is quoted as the excess of the U.S. dollar rate over the rate for the opposing currency – therefore an increase in the differential means an increase in the U.S. dollar rate compared to the rate in the other currency. It could be that rates in both currencies are expected to increase over the year end, but the U.S. dollar rate is expected to increase more.

Impact on futures maturities

Secondly, the impact can be shown to be related to the year-end period by looking at the implied rates for different futures maturities. Rate differentials increase more for the January expiry compared to the February or March expiries. There are fewer days to expiry for the January contract, therefore the higher rates over year end are less diluted by what may be thought of as the ‘background’ differential or ‘normal market conditions’. Similarly, there is no increase observed in the differential December contract.

By making further assumptions about the period over which the heightened rates apply during the year-end period (for example, in December 2020, these may have applied over the four-day weekend), an estimate can be made of the overnight rates that are being priced into the FX curve. From looking at SOFR and EFFR data, there is little evidence that the predicted U.S. dollar rate increases materialized in the overnight market across the end of the year, as a consequence of the Federal Reserve ensuring liquidity was available through to year end.

Already making an impact

Thirdly, the year-end effect is well known and anticipated by the market. The market can be seen pricing this in from a long way out. The implied rate differential from FX Link starts to rise several weeks out as the time to maturity declines. The Dec-Mar futures spread can be seen to contain this implied rate almost permanently.

Impact on returns

Finally, this pricing dynamic means that those in the fortunate position to be able to switch out of U.S. dollars over the year end may be able to use the FX Link market to lock in superior returns (see this link for an example of this type of trade). Clearly though, many institutions don’t have this luxury, which is why this pricing structure exists.

To discuss any of the themes in the article in more depth, please contact fxteam@cmegroup.com or visit cmegroup.com/fxlink for more use cases and how to get connected.