{kind=link}

Trading the spread between SGE Gold and COMEX

CME Group announced that it will list new gold futures contracts based on the Shanghai Gold Exchange’s Benchmark PM assessment. Subject to regulatory review, the Exchange will list both U.S. dollar and Renminbi denominated contracts in Q4 2019. In a prior article, we explored the global relevance of the Chinese gold market. In this article, we look at how the SGE price compares to COMEX prices and how customers can use “Exchange of Futures for Physical” transactions (EFPs) to seamlessly hedge their physical exposure using the new COMEX Shanghai Gold futures.

Trade the Spread between Shanghai and COMEX

In order to illustrate how the Shanghai/COMEX spread could be traded in the future, we first examine the spread between the two major trading hubs in the international gold markets - the COMEX 100oz Gold Futures (GC) market and the London OTC bullion market. A typically tight price difference between London spot gold (as measured by the LBMA Gold PM Benchmark) and concurrent GC prices reflects the mature market environment and an efficient connection between the two hubs via EFP transactions. Typically, GC will trade at a premium to spot gold in a contango environment. The spread between the two prices is a function of the gold term structure – the timing difference between spot and forward delivery - and of the supply/demand picture in the different delivery locations.

The spread between GC and the SGE PM benchmark is more volatile and is usually negative, meaning that SGE spot trades at a premium to the prevalent GC price. The Chinese gold market is not fully liberalized, and bullion banks require special licenses to import gold into the country. A premium for SGE gold could be warranted if tight import restrictions limit the supply of gold into the country. In addition, China is a net importer, and the price set locally needs to attract gold into China.

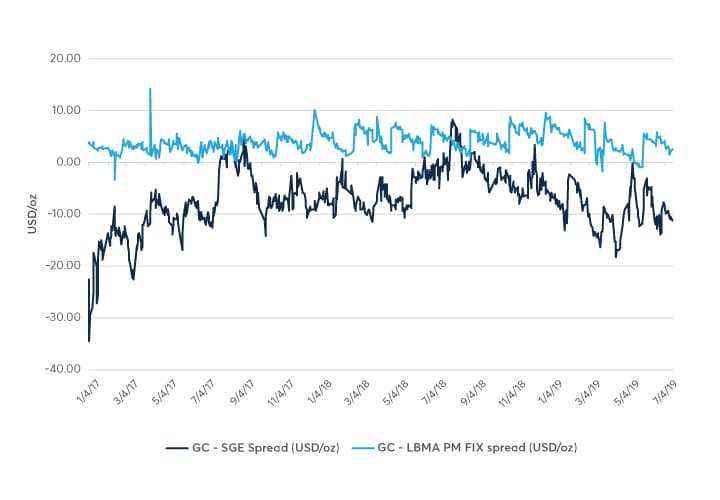

Chart 1 – COMEX Gold futures vs. SGE Gold and London OTC Gold

{kind=link}

Source: CME Group, Bloomberg

Across 639 trading days from January 2017 onwards, GC traded at an average premium of $3.84/oz to LBMA London spot gold. Across that same period, GC was quoted at an average discount of $7.12/oz to Shanghai gold. Compared to the OTC London/GC spread, the range of the Shanghai/GC spread is twice as wide, ranging from -$35 to +$8 (vs. -$3 to +$14 for OTC London/GC). The spread is also much more volatile, with a standard deviation of $5.58 vs. $1.96 for OTC London/GC.

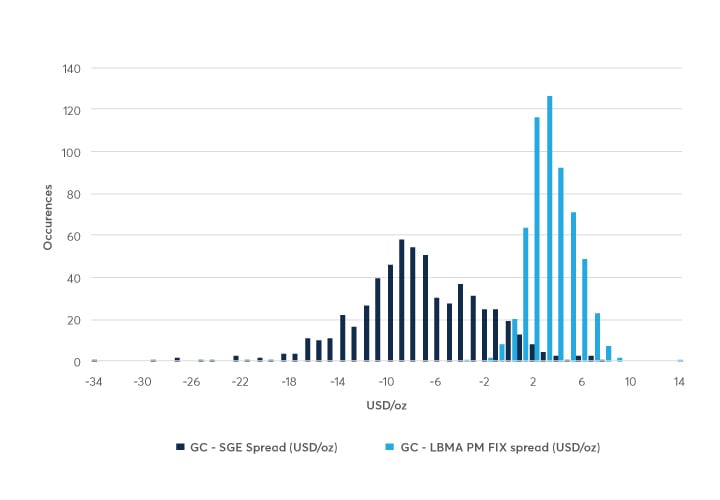

Chart 2– COMEX Gold futures vs. SGE gold and London gold histogram

{kind=link}

Source: CME Group, Bloomberg

Higher volatility and dispersion of the Shanghai/GC spread shows that the cross-market price discovery between onshore Chinese and international marketplaces is currently not as efficient as OTC London/GC. Many of the international market participants do not have direct access to the Chinese exchanges, and vice versa. By using both COMEX gold futures and the new COMEX Shanghai Gold futures contracts, customers can directly trade the price difference between the two locations on the same platform for the first time. As both GC gold and the new Shanghai Gold Futures are cleared via CME Clearing, margin offsets between the two products are applied and can make trading the spread capital efficient.

Manage the Spread Risks via EFPs

Customers who wish to hedge or arbitrage physical price exposures have an additional tool at their disposal: “Exchange of Futures for Physical” transactions (EFPs) can allow customers who have exposure to the spot gold price to simultaneously exchange a position in an Exchange futures contract against a corresponding physical transaction or forward contract on a physical transaction. In the case of GC contracts, EFP transactions are widely used by customers who hedge outright gold price risk on GC and then use EFPs to lock in the basis between the spot and the futures price. For example, a firm who bought 100,000 troy ounces of physical gold from a client could go short 1,000 lots of COMEX Gold futures to offset the gold price risk. To manage the basis between spot and the futures price, the firm would “sell the EFP” with a willing counterparty: in this transaction, the firm would exchange 1,000 lots of COMEX gold against 100,000 troy ounces spot, thereby eliminating all directional price risk and basis risk.

Similarly, for the new COMEX Shanghai Gold Futures, eligible firms would also be able to use an EFP to manage their OTC physical gold exposure. The physical component does not need to be directly linked to the Shanghai gold price. Other global locations such as Hong Kong, Singapore, London, or Zurich could also be used. EFPs can be transacted against spot gold, gold bullion, physically delivered OTC forwards, ETFs and ETNs, but not against positions in other futures contracts or options on futures contracts. The precise rules that govern the EFP process are found in CME Group Rule 538. Firms active in global gold markets may already be familiar with the use of EFPs, and that experience may be applicable to the Asian market. The EFP mechanism can bring the international futures liquidity pool on COMEX and the Shanghai physical gold market closer together.