{kind=link}

Trading Micro E-mini Options

Micro E-mini S&P 500 options and Micro E-mini Nasdaq-100 options can provide more precise hedging and risk management tactics for traders with exposure to the underlying indices. Whether a trader is looking to hedge market-moving events or perform daily transactions, Micro E-mini options can give the flexibility to execute strategies with a comprehensive listing cycle and around the clock trading. These unique options products can give traders the opportunity to access or express a view on the largest and most actively traded equity indices, while benefiting from the granularity of smaller-sized contracts. Micro E-mini options have shown strong growth, with over 26,000 contracts in total volume and over 50,000 contracts in open interest since their launch, a promising start for the newest additions to the Micro E-mini complex.

Underlying futures market

Micro E-mini S&P 500 futures (MES) and Micro E-mini Nasdaq-100 futures (MNQ) were introduced to the market on May 6, 2019, with a contract value equal to 1/10th that of the classic E-mini contracts.1 The fractional value of the Micro E-mini futures contracts makes them a more approachable contract for market participants to access the most active global equity index benchmarks, while affording greater precision when managing risk or expressing a view on the market.

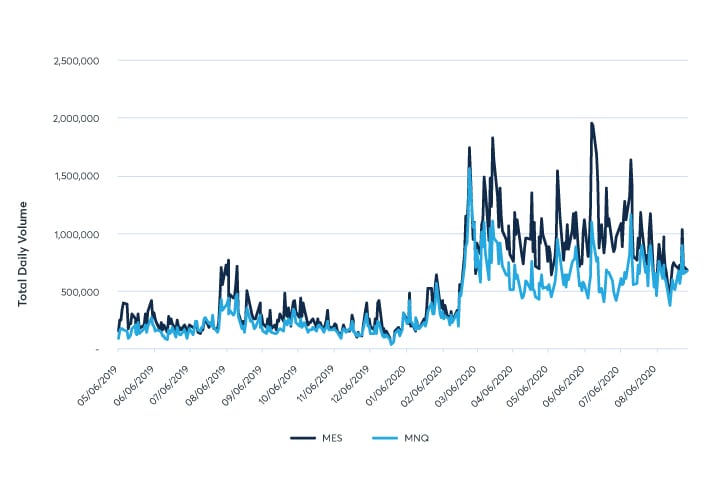

Over the past 15 months, both the MES and MNQ futures contracts have shown significant growth with daily volumes reaching heights of nearly two million contracts for the Micro E-mini S&P 500 and just over a million and a half contracts for the Micro E-mini Nasdaq-100, as the chart below illustrates.

{kind=link}

Source: CME Group

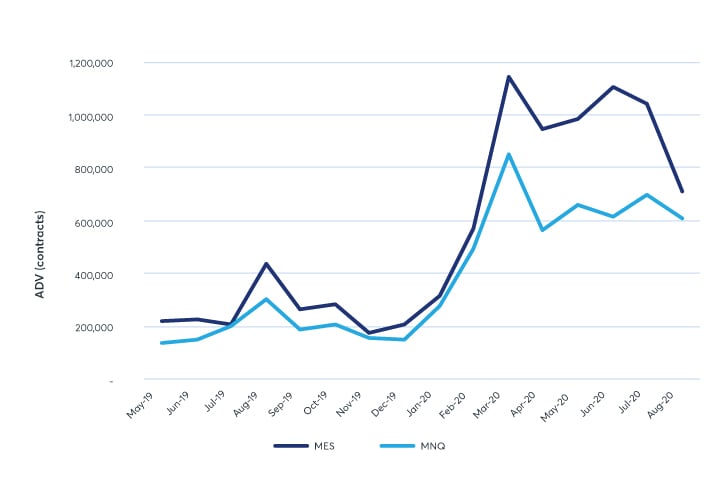

Beginning in March 2020, volumes surged in both futures products. The chart below illustrates how Micro E-mini futures monthly average daily volume (ADV) has gained momentum at the start of 2020.

{kind=link}

Source: CME Group

Heightened volatility from the COVID-19 global pandemic created record-setting ADV for both Micro E-mini S&P 500 futures and Micro E-mini Nasdaq-100 futures. In March, MES and MNQ futures ADV reached a high of 1,141,164 and 849,208, respectively. These record-breaking months were followed by the second-highest monthly ADV observations in June for MES with 1,107,677 and in July for MNQ with 698,991.

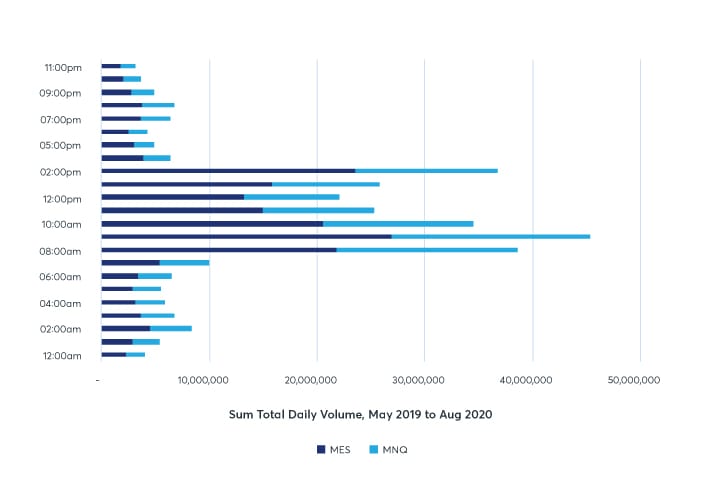

Additionally, Micro E-mini futures have performed extremely well during extended trading hours (ETH), which occur from the hours of 4:00 p.m. to 8:30 a.m. Central Time (CT). Micro E-mini S&P 500 futures have experienced 25% of their total daily volume occurring in ETH; similarly, Micro E-mini Nasdaq-100 futures have experienced 30% of their total daily volume occurring in ETH. With around the clock trading, liquidity is robust in these products across the globe, allowing traders to meet their hedging needs and strategies.

The chart below illustrates the summed total daily volume of trading in both futures products from May 2019 through August 2020, broken down by hour in CT. It is evident that most trading takes place during regular trading hours (RTH), between the hours of 8:00 a.m. and 3:00 p.m. CT; however, volume in ETH hours remains at least a quarter of all total volume in both products.

{kind=link}

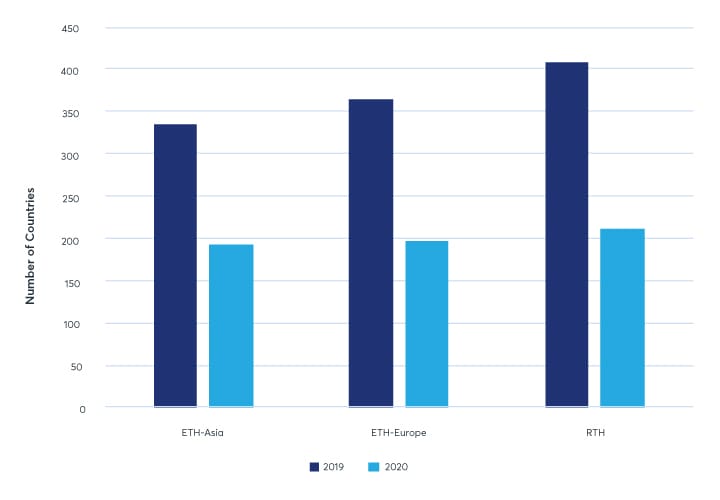

Further elaborating on the significance of ETH for MES and MNQ futures, country of origin evidences consistent global adoption of these products since their inception. Depending on the time of trade, countries can be bucketed into three different zones: ETH in Asia, ETH in Europe, and RTH.

It is common for countries, say Canada, to trade in all three zones; on the other hand, there are instances of a country only trading in a singular zone. Whatever the trader’s preference, MES and MNQ futures offer the ability to flexibly trade around the world at any time. This is evidenced by comparing the number of countries trading MES and MNQ futures in the three different zones since May 2019.

{kind=link}

In 2019, 168 countries traded in the ETH-Asia zone, 182 in the ETH-Europe zone, and 205 in the RTH zone. Furthermore, in 2020, adoption has been consistent across the three zones, with 96 countries trading in ETH-Asia, 98 in ETH-Europe, and 106 in RTH.

These metrics imply significant strength and global adoption in Micro E-mini futures, paving the way for the introduction of options on these products.

Contract specifications

Micro E-mini options on the S&P 500 and the Nasdaq-100 are available in a variety of maturities. To offer full risk management, the listing cycle will be comprised of weeklies, monthly and quarterly contracts. Find the full contract specs on the website.

Trading options around market events

When analyzing how best to implement an equity index trading strategy, it is important to understand the key features and capabilities of trading options, and why they might be the more appropriate product choice.

Options can provide position and risk management flexibility, where depending on the strategy, options can limit downside risk, manage event risk in a more targeted manner, and more efficiently deploy capital. CME Group’s centrally-cleared futures and options on futures contracts both offer the additional ability of mitigating counterparty risk and the potential for overall lower transaction costs.

In the specific case of Micro E-mini options there are multiple features afforded to market participants. These smaller-sized options not only offer more precise risk management with the ability to easily scale positions up and down with a fraction of the capital outlay, but they also offer a variety of expiration date listings. Micro E-mini options are comprised of weekly, monthly, end-of-month, and quarterly options contracts—this variety in expiries aims to cater to all traders and all strategies, with a goal of offering a plethora of ways to manage calendar risk.

Example 1: Using a protective put strategy around the US Presidential election

In the build-up to the American Presidential election in November, traders may start thinking about hedge equity index exposure depending on which candidate is expected to win, and the differing market reactions that the final results may deliver. The speculation on the potential outcome of the election can change frequently in the days and weeks leading up to the actual event, offering opportunities for different types of trades. To hedge the risk of the election, trading strategies such as protective puts and covered calls can be deployed. The justification for hedging the lead up to, and the results of, the US election can be further amplified when combined with the precision and flexibility afforded by Micro E-mini options.

For example, an asset manager believes the S&P 500 index might trade lower following the election results, and she currently manages client equity portfolios that include positions in Micro E-mini S&P 500 futures. Despite conviction in the current portfolio construction and wanting to keep some exposure to the upside, she is still concerned about the election and its potential impact on the market. To guard her clients from potential losses if the index declines, she can utilize protective put options on Micro E-mini S&P 500 futures.

Since Micro E-mini options have a variety of expiration dates listed, the asset manager can choose which contract listing best fits the needs of the portfolio. She decides to utilize weekly options to protect against the short-term risks of how the November election could affect markets. Since the election is on November 3, the first Tuesday of the month, the asset manager chooses protective put options that expire on the first Friday in November, otherwise known as Week 1 options.

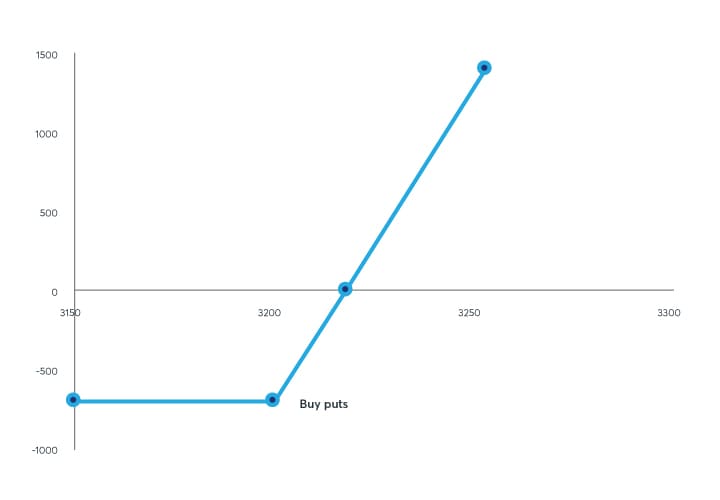

The asset manager has $65,000 of equity exposure in need of protection, represented by 4 Micro E-mini S&P 500 futures contracts, where the futures contracts are trading at 3218. The asset manager decides to buy slightly out-of-the-money protective put options with a strike price of 3200.

With a multiplier of $5, each Micro E-mini S&P 500 option will hedge $16,000 of exposure ($5.00 x 3200 = $16,000). Therefore, the asset manager will need to buy 4 put options to hedge the $65,000 portfolio exposure. The put options are offered at 35 index points per contract on Globex; therefore, the potential maximum loss for this protective trade would be the $700 premium paid for the 4 put options (35 index points/contract x 4 contracts x $5.00/index point = $700), illustrated in the diagram below.

{kind=link}

Since she paid $700 for the protection, the portfolio needs to earn $700 to break-even, where the break-even point is equal to the premium paid for the put options (35 index points/contract) plus the current price of the futures (3218). In this scenario, the futures will need to rally 35 points to 3253 for the asset manager to recoup the cost of the puts and to break-even.

While the asset manager’s trade may or may not reach the break-even point, the goal of the Micro E-mini protective put strategy is to protect the existing assets in the portfolio from potential losses in the days following the election, without completely forgoing the ability to participate in upside appreciation. The premium for the options is a relatively small price to pay to have the insurance and peace of mind that her investments are protected.

Example 2: Using a covered call strategy around the US Presidential election

Another investor has been using Micro E-mini Nasdaq-100 futures for some time to gain exposure to technology companies, but he believes that technology stocks might stagnate and limit the return of the portfolio in the month after the election. The investor can utilize a covered call option strategy on Micro E-mini Nasdaq-100 futures to generate income in the portfolio during this potential period of non-growth.

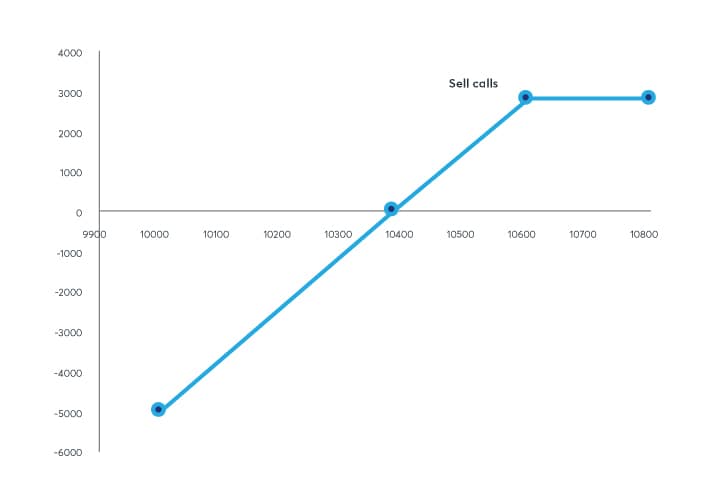

The investor holds 7 Micro E-mini Nasdaq-100 futures that are trading at a price of 10,580, worth $148,120 in exposure ($2.00 multiplier x 7 contracts x 10,580). He decides to deploy the covered call strategy using the December quarterly Micro E-mini Nasdaq-100 options and sells slightly out-of-the-money call options struck at 10,600 that are bid at 200 index points on Globex.

This strategy provides the trader with income on his portfolio in the event of market stagnation; namely, the $2800 premium collected on the 7 call options (200 index points/contract x 7 contracts x $2.00/index point = $2,800), illustrated in the diagram below.

{kind=link}

Since the investor sold the call options for a $2800 premium, the futures in the portfolio would need to lose $2,800 to break-even. The breakeven point per contract is equal to the current futures price of 10,580 minus the 200-point premium received, which means the futures would have to trade lower to 10,380 in order to break-even.

If the futures price at December expiration is below 10,600, the options will expire out-of-the-money and will not be exercised, which allows the investor to keep the $2,800 of premium previously collected as income in his account, thus enhancing the portfolio’s return for the period.

Using Micro E-mini Nasdaq-100 options in a covered call strategy, investors can generate income in their portfolios via collecting option premium if they are of the opinion that the Nasdaq-100 will stagnate for a period of time after the US election.

These single-leg strategies are just two examples of how individuals can hedge risk or express an opinion using Micro E-mini options around the potential impacts of the US presidential election. There are a multitude of ways that Micro E-mini options can provide individuals with the flexibility and precision needed to hedge or express views on potential market-moving events, as evidenced in these examples.

Example 3: Using a collar strategy amidst US-China trade tensions

Furthermore, single-leg strategies can also be combined to create more complex multi-leg strategies. For example, a protective put and a covered call can be combined to create a collar on a pre-existing futures position. A collar will typically involve the selling of a covered call that forgoes some upside price movement, but the collected premium is then used to partially offset the cost of purchasing the protective put that provides the downside protection. Collars can work well when the goal is to limit losses, specifically losses related to market-moving events, like the uncertainty surrounding trade talks between the US and China.

China is the world’s largest exporter, exporting close to $2.6 trillion in 2018,2 with trade comprising 19% of China’s GDP.3 The top recipient of these exported goods is the United States, who imported close to $500 billion in 2018.2 Despite ongoing trade discussions, the threat of tariffs on the goods traded between the two countries is a reality that could have a lasting effect on both economies. Furthermore, tariffs and other possible protectionary policies resulting from trade negotiations may present market participants with the need to hedge positions or express views during periods of increased uncertainty. If an investor believes equity markets will be impacted by new tariffs, one could use Micro E-mini options to protect from potential downside risk.

For example, persistent trade tensions might invite an investor to believe that tariffs will be placed on US imports of Chinese electronic goods, which could negatively impact his futures positions on the tech-focused Nasdaq-100 index. To hedge against this uncertainty the investor may seek to protect his pre-existing holdings in this index while hedging any volatility.

This trader has $170,000 worth of exposure to the Nasdaq-100 index through Micro E-mini Nasdaq-100 futures; he therefore already holds 8 Micro E-mini Nasdaq-100 futures. To hedge potential risk from US-China trade negotiations, this trader decides on a collar strategy, which will protect his existing 8 contracts from downside moves in the Nasdaq-100.

In this example, let it be assumed that a decision on the tariffs will be made in late October during the next hypothetical round of negotiations. Understanding that any decisions made during this meeting may take weeks and, possibly, months to take effect, the investor believes the market will correct for these policies by the end of the year. Therefore, options contracts with a December end-of-month expiration make the most sense if the investor is looking to limit losses as a result of trade negotiations. Since the investor holds 8 futures contracts, he subsequently sells 8 out-of-the-money Micro E-mini Nasdaq-100 call options and buys 8 out-of-the-money Micro E-mini Nasdaq-100 put options. As is typical with collar strategies, this allows the investor to generate cash by writing options to help finance the cost of protection against downside moves.

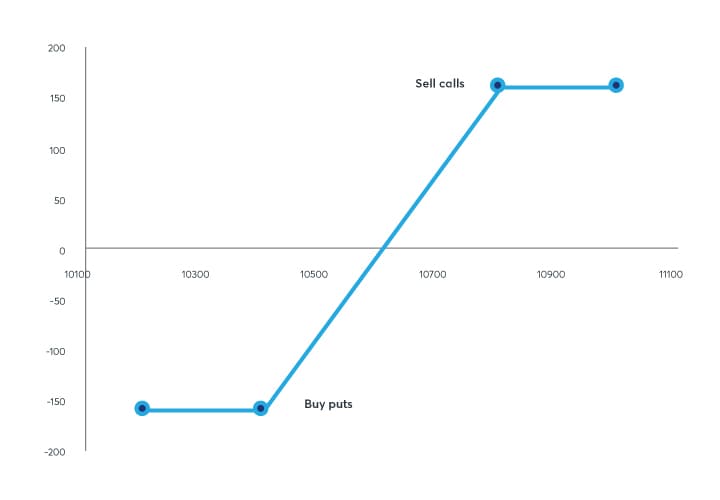

The futures are currently trading at 10,600. The investor sells the call options with a strike price of 10,800 for 200 index points per contract and in turn purchases the put options with a strike price of 10,400 for 210 index points each.

Therefore, the investor will receive $3,200 for the call options and pay $3,360 for the put options, which is a net expense of $160 to collar his futures position. In terms of break-even, the investor can recoup the cost of the collar if the Micro E-mini futures rally 10 points. As a reminder, with a $2 multiplier, the 8 Micro E-mini futures contracts will generate a $160 of profit on a 10-point move (8 contracts x 10.00 index points x $2 multiplier).

In lieu of paying $3,360 for the outright protective put options, this investor deployed a collar strategy for the small price of $160, after collecting the $3,200 in premium for the upside call options. This makes the desired downside protection below the put strike of 10,400 more affordable for the trader, but at the cost of forgoing any additional upside of the Micro Nasdaq-100 futures position above the 10,800 strike price of the calls.

{kind=link}

As further demonstrated in the above figure, the collar strategy allows the trader to limit his losses below 10,400 if tariffs are indeed implemented during the next round of negotiations; and if negotiations go well, it still allows him some limited upside potential up to 10,800. The impacts of trade negotiations are often unpredictable, but by utilizing the flexibility and precision of Micro E-mini options, this investor can ensure that his holdings are protected during periods of heightened volatility.

Example 4: The US Presidential election, volatility, and Micro E-mini options

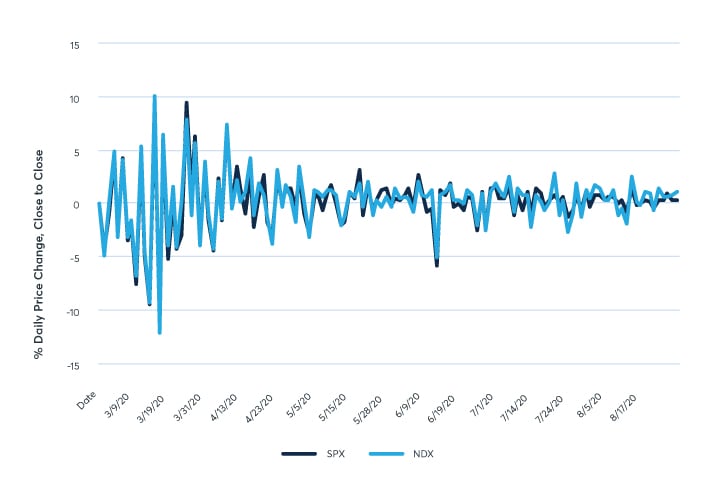

Options on equity index futures can be valuable tools to use when the market is experiencing heightened volatility. In March 2020, equity markets experienced increased volatility that was mainly driven by the COVID-19 global pandemic. As a result of this uncertainty, investors utilized futures and options on futures to both hedge risk and actively trade the opportunities presented by the market dislocation.

The S&P 500 and Nasdaq-100 indices saw daily price changes as low as negative 12% on March 12, 2020, indicating how volatile this period was for equity markets and the need for hedging tools.

{kind=link}

Source: Bloomberg L.P.

Markets can become volatile for numerous reasons, but, in many cases, the volatility is a reaction of other pressures in the marketplace. Particularly when there is a specific market event that may trigger volatility, CME Group’s Micro E-mini options can facilitate strategies that can be implemented by investors to protect against steep price movements.

To completely comprehend volatility, it is important to distinguish between two types: implied and realized. Implied volatility is the collective market expectation of how a financial product or security will behave in the future based on current option prices, while realized volatility is the measurement of the actual historical returns of the underlier. When volatility affects equity indices, like the S&P 500 and the Nasdaq-100, bite-size Micro E-mini options can provide the trader greater precision to fine-tune risk management.

Assume it is October and an investor knows the American Presidential election will have an impact on markets. To protect against sharp moves in either direction, an investor decides to utilize a calendar spread using Micro E-mini S&P 500 options. A calendar spread can be a useful tool when an individual wants to trade around a market event that has the potential to create significant price movements, and when the direction of these price movements is uncertain. Previously, a protective put and a covered call were described in the context of the Presidential election; however, it is pertinent to outline a more complex trading strategy using options on Micro E-mini S&P 500 futures to illustrate how options products can help investors navigate expected changes in volatility resulting from an election or another significant market event.

Assume it is October 27 and Micro E-mini S&P 500 futures are trading at 3500. In one week, the United States will have its presidential election, likely ushering in market volatility. This investor decides to sell a calendar spread, using weekly Micro E-mini S&P 500 options. The investor buys 1 weekly 3500 call expiring on November 6 for 72.00 points, or $360, and sells 1 3500 call expiring on December 18 for 122.00 points, or $610,4 netting a premium of $250. The implied volatility for the purchased call, when priced at 72.00, is 30.0. Similarly, the implied volatility for the written call, when priced at 122.00, is 25.0.5 This trade permits the investor to limit losses when markets are quiet, while still allowing for profit from large movements, whether up or down.

| Underlying futures: 3500 | Long call | Short call |

| Price (in points) | 72.00 | 122.00 |

| Implied volatility (in points) | 30.0 | 25.0 |

| DTE (days to expiration) | 11 | 46 |

Three scenarios could occur depending on the results of the presidential election: the market could rise, fall, or stay the same. The investor waits until the election results are publicized, likely on November 4, to see how the market is impacted, in which case one of the three scenarios will occur.

First, assume there is a significant market rally after the results of the election, leading Micro E-mini S&P 500 futures to rise to 3700. The day after the election, implied volatility moves to 18.0 for both call options. Since the market level exceeds the strike price of the options, the investor can sell the November options and buy back the December options to close the position and receive a net credit on the spread. In this scenario, the investor would pay 17.00, or $85, to unwind the position, and, when netted with the credit of $250, would collect a profit of $165.

| Underlying futures: 3700 | Long call | Short call |

| Price (in points) | 200.00 | 217.00 |

| Implied volatility (in points) | 18.0 | 18.0 |

| DTE (days to expiration) | 2 | 37 |

Second, assume the market falls after the election so that futures are now trading at 3300 and the implied volatility for both call options has moved to 18.0. The day after the election, the November calls are near zero, so the investor will allow these options to expire worthless and buy back the December options for 15.00. In this case, the investor would only have to pay the 15.00, or $75, to re-purchase the short call, and, when netted with the credit of $250, would collect a profit of $175.

| Underlying futures: 3300 | Long call | Short call |

| Price (in points) | 0.05 | 15.00 |

| Implied volatility (in points) | 18.0 | 18.0 |

| DTE (days to expiration) | 2 | 37 |

Lastly, assume the market stays the same in the aftermath of the election with futures still trading at 3500. The certainty of the election outcome has reduced the implied volatility from 30.0 for the long call and 25.0 for the short call to 18.0 for both calls, now that the market has calmed down. The investor will have to pay 60.00, or $300, to close the position, and, with his $250 credit, the investor will lose $50 on the spread. Although unhappy, the investor was willing to take the risk of losing $50 for the chance to gain a profit as high as $175 on this trade.

| Underlying futures: 3500 | Long call | Short call |

| Price (in points) | 19.00 | 79.00 |

| Implied volatility (in points) | 18.0 | 18.0 |

| DTE (days to expiration) | 2 | 37 |

In this scenario, the investor understands that there will most likely be volatility in the S&P 500 after an event as impactful as the US Presidential election; however, the uncertainty of which way the volatility will go, is why the investor may decide on a short calendar spread trade.

While an individual can trade Micro E-mini options under all market conditions, these products can be especially important tools for investors wanting precise risk management during periods of market uncertainty. With the upcoming Presidential election in the United States and the likely impending volatility around the event, investors will be poised to protect holdings from a potentially volatile reaction.

For more information on Micro E-mini options and how to trade them, visit cmegroup.com.

References

- Contract multipliers for the futures contracts are as follows: E-mini S&P 500 futures (ES): $50, E-mini Nasdaq-100 futures (NQ): $20; Micro E-mini S&P 500 futures (MES): $5; Micro Nasdaq-100 futures (MNQ): ($2)

- “China Profile,” The Observatory of Economic Complexity, https://oec.world/en/profile/country/chn

- “China Exports,” World Integrated Trade Solution, https://wits.worldbank.org/CountryProfile/en/Country/CHN/StartYear/2014/EndYear/2018/Indicator/NE-EXP-GNFS-ZS

- Micro E-mini S&P 500 options have a multiplier of $5; Micro E-mini Nasdaq-100 options have a multiplier of $2.

- Where an implied volatility of 30.0 means there is a 30% implied standard deviation move for one year.

Micro E-mini futures and options

See how Micro E-mini futures and options can help you precisely manage equity index exposure.