{kind=link}

The Future Role of Derivatives in Banking

Introduction

This is the final installment of a three-part report aimed at examining patterns of use of rate-based derivatives at US banks, determining how the more active utilization of derivatives to manage risk has made an impact on bank performance, and the role that derivatives can play going forward as an instrument for interest rate risk (IRR) management for US banks.

"…pending implementation of the new swap margin rules will significantly increase the operational complexity and transaction costs of OTC swaps and will likely result in a movement toward exchange-traded instruments…"

This paper reviews the current economic environment in which banks operate in relation to the management of interest rate risk, examines the role that derivatives will play in allowing banks to manage IRR in the future, and suggests IRR management best practices that will serve banks well in the future.

One of the major lessons of the 2007 banking crisis was the reality of counterparty risk in unsecured over-the-counter (OTC) interest rate swaps. When Lehman Brothers filed for Chapter 11 bankruptcy protection in September 2008, the firm defaulted on what was said to be more than 66,000 trades representing $9 trillion in interest rate swaps1, putting the term “counterparty risk” in the working vocabulary of bank treasurers globally.

In October 2015, US banking regulators jointly adopted new rules imposing margin requirements on participants in OTC interest rate swaps2 (“uncleared” swaps in the vocabulary of the regulators). The new margin rules are to be phased in over a four-year period beginning on September 1, 2016, with an initial compliance threshold of $3 trillion and ratcheting down to a threshold of $750 billion by September of 2020 (the thresholds are based on the notional value of a bank’s OTC swap portfolio). The OTC swap margin thresholds are subject to a minimum and maximum margin level set in accordance with the global Basel III framework for bank system capitalization.

The pending implementation of the new swap margin rules will significantly increase the operational complexity and transaction costs of OTC swaps and will likely result in a movement toward exchange-traded instruments, where counterparty risk is greatly reduced by the role of the exchange in guaranteeing performance risk and enforcing ongoing margin requirements on market participants.

Regulator Concerns

As context for this discussion, we examine the FFIEC’s statement entitled “Advisory on Interest Rate Risk Management” (FFIEC Advisory) concerning the importance of IRR management for US banks. The FFIEC statement was issued on January 6th 2010 and coincided with an article appearing in the FDIC’s Supervisory Insights newsletter entitled “Nowhere to Go but Up: Managing Interest Rate Risk in a Low-Rate Environment.”

The main concern raised by the FDIC newsletter in 2010 was the temptation for banks to “chase yield” by funding long-term fixed-rate assets (primarily residential and commercial loans) using very cheap short-term deposits. This was a real concern to the regulators, as at the time of publication 1-month Treasury bills were yielding 0.03% per annum (pa) compared with the yield on 30-year Treasury bonds of 4.7% pa.

The regulators’ concerns were underpinned by the risk that rising short-term rates (a response to a recovery economy) would squeeze the profitability of any fixed rate long-term loans that had been funded using these cheap demand deposits, which in turn would erode the capital base and long-term stability of the banking system. This risk is known as repricing risk and managing this risk is a key objective of interest rate hedging programs.

1London Clearing House (http://www.swapclear.com/why/case-studies.html)

2https://www.federalreserve.gov/newsevents/press/bcreg/20151030b.htm

The Future of IRR

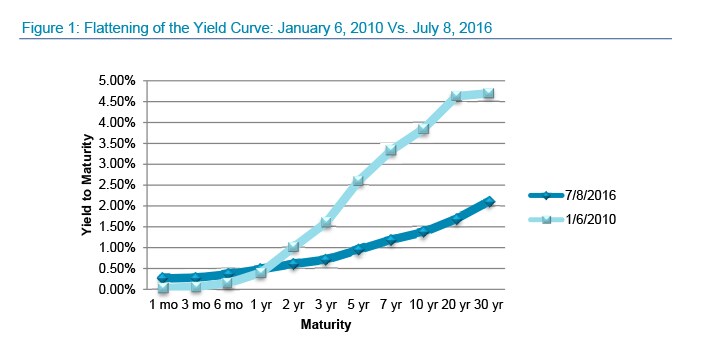

Accessing today’s interest rate environment and looking toward the future, short-term rates continue to drift along a long and historic bottom, with 1-month Treasury bills yielding 0.26%, a mere 23 basis points more than the low rates that prompted the FDIC and FFIEC to issue their guidance in 2010.

What is different today is that long-term rates have also collapsed, flattening the yield curve with rate declines of 200 basis points or more for bond maturities in the 5 through 30 year range. In essence, the concerns of the regulators in 2010 have been turned on their head: rather than seeing short-term rates increase, the market has seen long-term rates decrease, resulting in today’s rather flat yield curve in comparison with 2010.

Figure 1: Flattening of the Yield Curve: January 6, 2010 Vs. July 8, 2016

{kind=link}

Source: US Department of Treasury (Daily Treasury Yield Curve Rates)

While concerns about repricing risk remain, today’s flattening yield curve has introduced a second risk known as yield curve risk, which is the impact that changes in the structure of the yield curve have on the value of long-term assets. For example, a bank making a long-term fixed rate loan based on today’s relatively low long-term rates would experience a decrease in value should long-term rates revert to their historical premium over short-term rates.

From the perspective of IRR management, a flattening yield curve in a low-rate environment can represent a double whammy to banks. If, as many market observers believe, a flat yield curve portends an imminent rise in short-term rates, then a subsequent normalization of the yield curve through a rise in long-term rates would further reduce lending spread for banks, perhaps even driving returns into negative territory.

The good news here is that banks have the ability to limit the potential damage to their profitability and capital base by implementing an IRR program that includes the use of financial hedging. An example of a simple rate hedge is shown in the following section of this report to illustrate the benefits of hedging in protecting the bank’s loan portfolio from IRR.

An Interest Rate Hedging Use Case

To illustrate how active hedging utilizing derivatives can help banks manage IRR, imagine that the CFO of a large regional bank is attending the summer meeting of the bank’s asset-liability committee (ALCO) to review the bank’s recent financial performance.

During the second quarter, the bank had made $200 million in 5-year corporate loans, funded in equal amounts from matching fixed rate deposits (i.e., 5-year Certificates of Deposit) and from the bank’s floating-rate core retail deposits. The corporate loans were structured as “bullet” loans, meaning that while interest was payable monthly during the life of the loan, principal was to be paid in a single lump sum at maturity (hence the duration of the loans were close to their 5-year term).

During the ALCO meeting, the committee expressed concern about the possibility of rising rates impacting the profitability of the loans made during the quarter, and asked the CFO to hedge the bank’s exposure arising from its use of core deposits as partial funding for the portfolio. The CFO considered the use of a standard interest rate swap, its usual instrument for hedging rate risk, but current pricing in the swap market was not considered attractive, and furthermore there was a lingering concern regarding the credit risk of the counterparties with whom the bank had done business in the past.

Table 1: Overview of CBOT Treasury Futures Contacts

| Tier | 2-YR Note Futures | 10-YR Note Futures | 10-YR Note Futures | T-Bond Futures | Ultra T-Bond Futures |

| Face Amount | $200,000 | $100,000 | $100,000 | $100,000 | $100,000 |

| Maturities | 1 ¾ to 2 years | 4 1/6 to 5 ¼ years | 6 ½ to 10 years | 15 to 25 years | 25 to 30 years |

| Contract Months | Quarterly cycle in March, June, September, and December | ||||

Source: CBOT

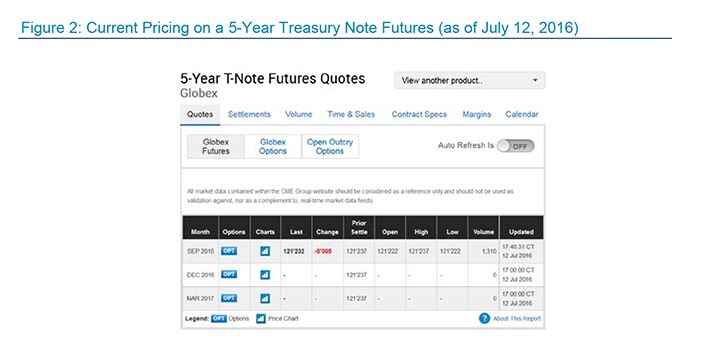

After some investigation, the bank decided to utilize the interest rate futures market to hedge the IRR of this loan portfolio. The bank scanned the current products available at the CBOT (Table 1) and selected the 5 year T-Note futures product.

Figure 2: Current Pricing on a 5-Year Treasury Note Futures (as of July 12, 2016)

{kind=link}

Source: CME

The bank sold 1,000 contracts (with a notional value of $100 million) of September 2016 5-year Treasury Note futures at the current quoted price of 121 2/32 (Figure 2: Current Pricing on a 5-Year Treasury Note Futures (as of July 12, 2016)Figure 2). The bank’s concern about a rise in interest rates due to a recovering US economy proves to be prescient, as rates indeed rose (in this fictional example) by 200–225 basis points across the entire yield spectrum before stabilizing at what the bank believed to be a long-term sustainable level.

The bank’s profit on the hedge is based on the difference between the value the contracts were originally sold and the value the contracts were at when the transaction was closed out, in this case:

(121 2/32 – 119 2/32) x 1,000 contracts x $1,000 = $2,000,000

The profit from the bank’s hedge in this example more or less completely offset the impact that the 200–225 basis point rise in short-term deposit rates had on the $100 million portion of the commercial loans originated in Q2 2016 that had been funded using the bank’s core deposits.

Of course, real life is seldom so clean and simple, and so the precise selection of the size, type, and tenor of a hedging instrument, as well as the timing of a decision to close out a hedged position, will all play a part in the performance of the hedge against an ever changing economic environment. Additionally, the time value of money invested today and profits earned in the future need to be considered, but the point is nevertheless made that a bank can utilize the futures market for US Treasuries to protect itself from the risk of financial loss due to adverse changes in interest rates.

Best Practices in IRR Management

Reflecting on the pending implementation of the new margin requirements for OTC swaps and the increased attention that regulators have on IRR management, the FFIEC created additional training for bank examiners specifically on the topic of IRR as part of its 2016 training program. The new FFIEC workshop is conducted over a three-day period and focuses on balance sheet analysis, IRR modeling, and the evaluation of a bank’s IRR management strategies.

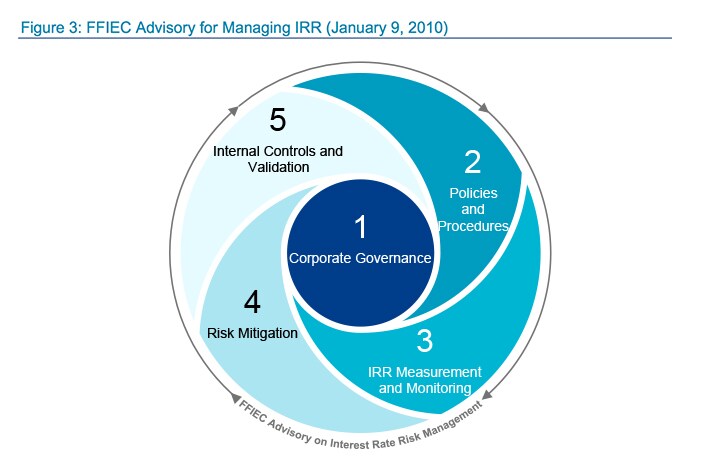

As the regulators prepare for increased scrutiny of IRR, the banks themselves need to step up their own game in regard to monitoring IRR and ensuring that the appropriate steps are being taken to manage and mitigate their investment portfolios from IRR. The 2010 FFIEC Advisory on managing IRR is a good starting point for banks looking to retool their internal IRR management practices, focusing on five elements shown in Figure 3.

Figure 3: FFIEC Advisory for Managing IRR (January 9, 2010)

{kind=link}

Source: FFIEC

Accordingly, banks can create an IRR readiness campaign that is based on three fundamental best practices that together encompass the five elements of IRR compliance that will drive regulator audits in the future; these best practices are education, the use of technology, and the diversification of interest rate hedging instruments beyond traditional swaps.

Role of Director Education

The FFIEC’s Advisory made it clear that IRR management begins and ends with a bank’s Board of Directors, with responsibility for ensuring that the bank has a well formed IRR management policy, that appropriate IRR limits are in place, and that the Board is routinely monitoring the executional success of the bank’s IRR policies. However, with the traditional emphasis on professional diversity in establishing a well-rounded Board, many bank directors are ill-equipped to pass judgment on issues of IRR management that are complex and constantly in flux.

Similarly, the bank’s executive management is charged with devising systems to execute Board-approved strategies, policies, and procedures and to report on the operational results from these systems over time. In addition to formalizing the process of assessing risk through the creation of a cross-functional ALCO committee within the bank, bank management is tasked with designing and implementing internal controls to ensure that the policies and tools of managing IRR are not circumvented by actual business practices.

In regard to the role of the Board in particular, education of the Board members is clearly important in ensuring that the full Board is engaged in setting the agenda for effective IRR management. As such, banks should implement director training programs to ensure that directors have a basic understanding the cause and consequences of IRR, the role that a bank’s ALCO plays in monitoring IRR, and the need for active participation of individual Board members in overseeing the active engagement of the bank’s senior executives in IRR management.

Use of Technology

While corporate governance leads the regulatory agenda in regard to proper IRR management, two of the FFIEC’s remaining four focus points relate to the use of technology in managing IRR: they are the measurement and monitoring of IRR, and the implementation of internal controls and validation of IRR forecasts to ensure the success of IRR management programs.

The resulting complexity of analytic requirements has taken most of the banking industry past the point where traditional reliance on Excel spreadsheets can continue to serve evolving needs. While the global banks and most superregional banks have been relying on dedicated treasury management systems (TMS) for many years, many midsize regional banks and smaller community banks continue to rely on the manual creation of IRR forecasts and reports through Excel spreadsheets.

The operational components of embedding sound IRR management into a bank’s daily funding and lending decisions is complex and subject to constant flux due to economic and market conditions. Furthermore, regulators require banks to establish robust reporting mechanisms to support the proper functioning of a bank’s ALCO sessions, including reporting on the bank’s loan portfolio, its sources of funding, and the resulting interplay that interest rates play on the bank’s pro-forma profitability and capital adequacy.

The FFIEC Advisory suggests that banks perform quarterly stress tests to evaluate the impact of changing interest rates on bank earnings. To support the effectiveness of these tests, banks are to revalidate annually their financial models including the key economic assumptions used in performing their stress tests. The essence of this requirement is to improve the bank’s ability to prepare pro-forma IRR reports by ongoing measurement of the bank’s past performance against forecasts.

The expected movement towards TMS systems by regional banks will be good news for vendors like FIS/Sungard, Misys, Reval, and Wall Street Systems, all of whom offer robust risk management system to monitor and manage financial risk. The additional benefit to banks that utilize a dedicated TMS platform is that internal controls including counterparty and trade limits can be embedded in the trading system, creating transparency for the regulators in the existence and effectiveness of the bank’s policies and procedures.

Diversification of interest rate hedging instruments

The impending implementation of the new margin rules governing OTC swaps will increase the complexity and transactional cost for banks that rely heavily on these traditional instruments for managing IRR, and will in time create additional interest in exchange-traded instruments including interest rate futures and options.

In addition to the advantage of utilizing a central clearing agent to eliminate counterparty risk, the liquidity offered by exchange-traded instruments provides flexibility to banks to augment or unwind their hedged positions on a daily basis in response constant changes in the markets. When paired with the use of a modern TMS platform, a bank that implements a new exchange-traded strategy for portfolio hedging can monitor its asset and liability structure in real-time and make immediate adjustment to its position based on changes in the rate environment.

It is clear that futures and options play an important part of the global banks’ strategy for managing IRR, and to a lesser extent the superregional banks, and so the biggest beneficiary of the advantages of an IT-enabled exchange-traded derivatives program are the regional banks who continue to lag behind their larger peers in the use of these derivatives.

While the benefits of exchange-traded derivatives are clear, it is also clear that OTC swaps will continue to be an important foundational element of most banks’ IRR management strategy. In this context, the impact of the new margin requirements on OTC swaps will not completely undermine the traditional IRR hedging market, but rather will encourage regional banks to seek a more balanced portfolio of OTC and exchange-traded instruments.

Path Forward

This report has focused on the financial implications of the Tier 3 and Tier 4 banks’ reliance on conventional OTC swaps to manage IRR. The element of counterparty risk that was made obvious by Lehman Brothers’ bankruptcy in 2008 has not escaped the notice of bank regulators, who have introduced new margin requirements on OTC swaps to bring the underlying risk of these instruments more in line with exchange-traded futures and options.

Bank regulators have been paying close attention to IRR since early 2010, when the persistence of sub-0.50% short-term rates created the concern that some yield-chasing banks were funding long-term retain and commercial loans utilizing cheap core retail deposits. The recent flattening of the yield curve has created a potential double-whammy of repricing risk and yield curve risk for banks that have been participating in this risky game of managing new lending spread.

In this context, IRR management has become more important than ever and accordingly banks of every size need to step up their game in devising risk strategies and implementing new technology-based solutions to more actively manage IRR. The path to success will start with stepping up the education level of the Board of Directors in regard to the key drivers of IRR management.

To support the consistent implementation of the bank’s IRR management program, regional banks need to upgrade their risk management tools from old Excel-based systems to modern TMS platforms, a step that will also provide enhanced real-time reporting capabilities to support a more active approach to managing the bank’s derivatives portfolio.

Finally, as the ears of the bank regulators tune into the counterparty risk that is inherent in the use of traditional OTC interest rate swaps, the increased complexity and cost of OTC swaps will require regional banks to take a closer look at the opportunities provided by the large and liquid markets for exchange-traded rate-based derivatives.

Copyright Notice

Prepared By

Celent, a division of Oliver Wyman, Inc.

Copyright © 2016 Celent, a division of Oliver Wyman, Inc. All rights reserved.

This report may not be reproduced, copied or redistributed, in whole or in part, in any form or by any means, without the written permission of Celent, a division of Oliver Wyman (“Celent”) and Celent accepts no liability whatsoever for the actions of third parties in this respect. Celent and any third party content providers whose content is included in this report are the sole copyright owners of the content in this report. Any third party content in this report has been included by Celent with the permission of the relevant content owner. Any use of this report by any third party is strictly prohibited without a license expressly granted by Celent. Any use of third party content included in this report is strictly prohibited without the express permission of the relevant content owner This report is not intended for general circulation, nor is it to be used, reproduced, copied, quoted or distributed by third parties for any purpose other than those that may be set forth herein without the prior written permission of Celent. Neither all nor any part of the contents of this report, or any opinions expressed herein, shall be disseminated to the public through advertising media, public relations, news media, sales media, mail, direct transmittal, or any other public means of communications, without the prior written consent of Celent. Any violation of Celent’s rights in this report will be enforced to the fullest extent of the law, including the pursuit of monetary damages and injunctive relief in the event of any breach of the foregoing restrictions.

This report is not a substitute for tailored professional advice on how a specific financial institution should execute its strategy. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisers. Celent has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified, and no warranty is given as to the accuracy of such information. Public information and industry and statistical data, are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information and have accepted the information without further verification.

Celent disclaims any responsibility to update the information or conclusions in this report. Celent accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages.

There are no third party beneficiaries with respect to this report, and we accept no liability to any third party. The opinions expressed herein are valid only for the purpose stated herein and as of the date of this report.

No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof.

This report was commissioned by CME Group ("CME") at whose request Celent developed this research. The analysis, conclusions and opinions are Celent's alone, and CME had no editorial control over the report contents.

No responsibility or liability is accepted by CME for the contents of this report (including any errors of fact or omission or for any opinion expressed herein), for any reliance placed upon it, or for any loss or damage arising out of the use of all or part of this report.

View this article in PDF format.