https://www.cmegroup.com/content/dam/cmegroup/education/images/2019/gold_984x137.jpg

{kind=link}

Synthetic Income from Precious Metals

A CME Group Options based Strategy

While gold and other precious metals such as silver, platinum and palladium have held investor’s interest over the last several decades, one of the primary disadvantages is that metals themselves do not produce any kind of income. Stocks pay dividends and bonds pay interest, but in the words of Warren Buffett, the metal “just looks at you!” This doesn’t have to be the case. Although physical gold bars (and other metals) and coins fail to pay dividends or interest, using options, an investor with a good background in option writing strategies (or an investor working in conjunction with an FCM that has options expertise) could create income.

By using CME Group options on gold futures (or silver, copper, platinum, palladium), one can sell or write options thereby “synthesizing” a stream of income from their metals holdings. The strategy is similar to covered writing with stocks. You purchase 100 shares of stock and sell a call option against your shares and collect a premium. Sometimes premiums can be quite large, and the resulting income could be significant to the option seller.

The premium is the seller’s to keep no matter what happens. If the stock has a decline, the premium provides a cushion against the decline in the share price. If the stock remains unchanged you have de facto collected a dividend of sorts. If the stock advances beyond the strike price of the call you sold, you may have your shares called away but, the premium remains yours to keep. The mechanics of selling options on gold futures would work in a similar fashion. We will use options on Gold futures to illustrate different scenarios but as mentioned above, the strategy can be done on any CME Group precious metals product that has options. Options on gold futures have several advantages to an investor/hedger that is trying to create an income stream from metals:

• Options on Gold futures are the most actively traded options in our metals complex trading over 40,000 contracts per day. See table below for leading precious metals and copper volume and open interest data for 2018

Figure 1: Volume and Open Interest Summary Table

| 2018 Futures ADV | 2018 Year End Open Int. | 2018 Options ADV | 2018 Year End Options Open Int. | |

| Gold Futures | 326,188 | 462,628 | 48,745 | 1,184,907 |

| Copper Futures | 129,891 | 238,023 | 1,398 | 17,990 |

| Silver Futures | 95,639 | 177,555 | 7,514 | 221,725 |

| Platinum Futures | 21,662 | 82,682 | 180 | 4,413 |

| Palladium Futures | 5,689 | 26,773 | 117 | 1,124 |

- In terms of open interest, options on gold futures are one of the largest option products in the world with over 1,200,000 contracts open.

- Options on Gold futures trade around the clock on CME Group’s Globex trade matching engine. Given the global nature of the gold market, good liquidity exists in non-US time zones as well.

- The CME Group clearing house risk management expertise minimizes counterparty risk.

- This strategy is not limited to gold and can be done in Silver, Platinum, Palladium and Copper. It can be done by dealers, miners, fabricators, producers, hedge funds,

- high net worth investors, pension funds and speculators— anyone holding physical metal or futures contracts.

Illustration

A gold fabricator with an excess of inventory of 1000 ounces, believes that gold will remain locked in a narrow trading range between $1,275/oz and $1,300/oz for the next few months. At current prices –about $1,290/oz—the fabricator can make a profit. However, he is looking to produce additional income (thereby increasing his effective selling price) by selling options on gold futures. He decides

to sell slightly out of the money options. The exact premium obtained from selling the options depends on which option strike price he sells. Figure 2 below displays the premiums for various March gold options. March gold futures are currently trading at $1,290/oz.

After careful consideration, the fabricator decides to sell the March 1290 call option. Since his inventory is 1000 ounces, he will have to sell (sell to open or sell short) 10 March 1290 call options (each COMEX gold futures options calls for 100 ounces thus 10 contracts will be necessary)

Figure 2: Options on Gold Futures Settlements (1/22/19)

| Strike | Type | Open | High | Low | Last | Change | Settle | Estimated Volume | Prior Day Open Interest |

| 1270 | Call | 22.30 | 26.50B | 21.80A | 25.70A | -0.80 | 25.50 | 18 | 1,335 |

| 1275 | Call | 22.90 | 23.00B | 18.70A | 22.20A | -0.90 | 22.00 | 5 | 3,974 |

| 1280 | Call | 16.40 | 19.80B | 15.90A | 19.00A | -0.90 | 18.90 | 31 | 5,042 |

| 1290 | Call | 14.50 | 14.50 | 11.30A | 13.70A | -1.10 | 13.50 | 171 | 1,466 |

| 1295 | Call | 12.10 | 12.30B | 9.40A | 11.50A | -1.10 | 11.30 | 125 | 1,291 |

| 1300 | Call | 10.00 | 10.30 | 7.80A | 9.70A | -1.10 | 9.50 | 263 | 5,908 |

| 1305 | Call | 8.90 | 8.90 | 6.50A | 8.10 | -1.00 | 8.00 | 242 | 1,662 |

The premium for the 1290 call is 13.50. Since each underlying future is a 100-ounce contract, the $13.50 premium is multiplied by 100—giving you a dollar amount of $1,350 per contract. $1,350 X 10 contracts would mean the options seller receives $13,500 in premium.

Potential Scenarios at Expiration:

- Spot Gold and Gold futures decline $40/oz to $1,250 by expiry—The inventory of 1000 ounces declines in value by $40,000 ($40 X 1000). With gold futures at $1,250, 1290 call expires worthless. The seller keeps the premium of $13,500 which partially offsets the decline in value of his inventory.

- Gold and gold futures remain at current prices—This scenario results in no loss on the gold inventory. Assuming gold futures are at 1290 or lower, the option expires worthless and the entire premium is kept by the seller.

- Gold advances to $1,320/oz. at or near expiry—While this scenario values the fabricator’s inventory higher by $30,000, it presents some minor obstacles to his short options on futures position. The seller of a call option on a future is at risk of having the underlying futures called away from him if gold futures are above the 1290 strike.

The problem is he has no futures contract position but instead holds physical gold in inventory. To get around this logistical issue, the fabricator has a couple of choices:

A) At expiration with futures at $1,320, the 1290 call options would be worth 30.00 ($3,000). He sold an option for 13.50 that is now worth 30.00 (1320-1290) for a loss of 16.50. Anytime prior to expiration, he could buy back (“buy to close”) his short position and take the loss on the options leg. He would still have a gain on his gold holdings of $30,000 but the loss on the option position of $16,500 (16.50 x 100 x 10 contracts) would result in a total position gain of $30,000 - $16,500 or $13,500.

Choosing “A”, relieves the fabricator of his obligation to deliver a futures contact. He could subsequently sell another options with a different strike price and expiration date and start the process over again.

B) The fabricator could also go into the futures market and buy (go long) a gold futures position thus satisfying his obligation should the futures be called away. Note that all in-the-money futures contracts (i.e. futures trading above the call option strike) are automatically exercised.

To calculate return on strategy in percent is simple math.

- $13,500 in premium divided by $1,290,000 value of excess inventory of 1000 ounces = 1.04 % return to expiry.

- The March Options on futures expire on February 25, 2019 or 1 month from now. So, the 1.04% 1-month return would be 12.48% annualized (assuming he could do this transaction each month).

- Fabricator realizes additional $13,500 in income—raising his effective selling price.

- The effective selling price at $1,290/oz considering the options premium is 1290 + 13.50 = $1303.50/oz

- Should gold fall in price, he is partially protected (hedged— by the premium taken)

Additional Considerations

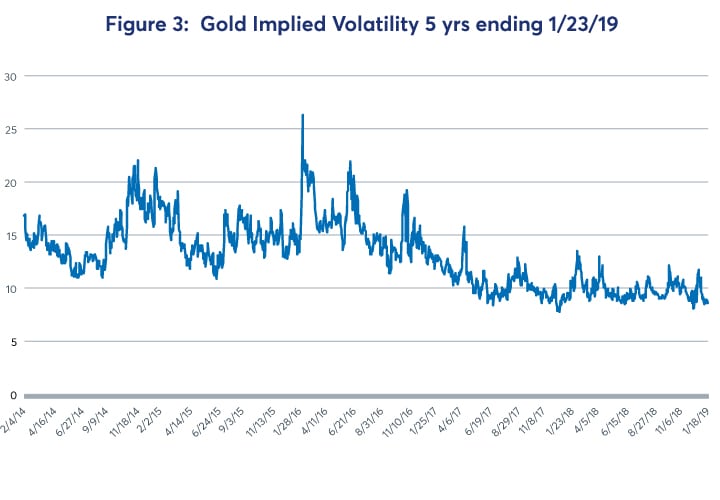

When trading options from the long or short side, one must pay particularly close attention to levels of implied volatility. Because options are four dimensional, you must focus on more than just the up and down price movement of the underlying futures. Implied volatility is a critical variable in how an option is priced. In the current environment, implied volatility is near the lower end of the spectrum for gold options and has been for much of the past two years. See figure 3 below for a 5-year history of gold volatility. Higher implied volatility generally leads to higher options premiums with lower volatility leading to lower options premiums. This is because during high volatility environments, you have a greater chance of moving through a given strike whereas, lower volatility environments have less of a chance of moving beyond a given strike. If you are going to sell options for income, it makes sense to sell at higher levels of volatilities. The rate of return will be dramatically higher. To illustrate how volatility impacts the 1290 call option in our example, figure 4 shows the premium levels at different volatility levels. At the 10th percentile level of volatility, the 1290 call is priced around 13. At the 90th percentile, its price is substantially higher—24.90. Selling at the higher volatility would have nearly doubled the fabricator’s income from the strategy. While percentile rankings are not perfect indicators, they can give the options trader a better appraisal regarding cheap vs. expensive options. And as we mentioned before, options are four dimensional instruments. You need to focus not only on the ups and downs of the underlying gold futures, but also consider changes in volatility and time to expiration.

{kind=link}

Figure 4: Implied Volatility and Impact on 1290 call premiums

| Implied Volatility | March 1290 Call Premium | |

| High | 26.39% | 26.35 |

| 90th%tile | 17.39% | 24.90 |

| 75th%tile | 15.23% | 21.80 |

| 50th%tile | 13.10% | 18.60 |

| 25th%tile | 10.28% | 14.00 |

| 10th%tile | 9.29% | 13.00 |

| Low | 7.80% | 10.80 |

Final Remarks

Options have long been used as instruments that can provide retail and institutional investors with additional streams of income as well as a myriad of other strategies. CME Group precious metals options have many advantages including around the clock liquidity and can help fabricators, dealers, miners and speculators alike take advantage of market opportunities. For more information visit cmegroup.com/education. We have a great deal of educational information on gold futures and options and stand ready to answer any questions you may have. You may also contact your FCM for additional information on options.