{kind=link}

Spread Trading Opportunities with Precious Metals

Spread trading is a widely-used trading strategy in futures markets and offer some key advantages over outright futures trading (i.e., going long or short a single futures contract). These include capital efficiencies with lower margin outlay and potentially superior risk-adjusted returns. This is particularly true for precious metals markets, where the underlying commodities demonstrate strong correlations with each other due to close economic links but also distinct fundamental drivers that can create profitable spreading opportunities using the associated futures contracts.

A spread trade using futures is created by buying a futures contract and simultaneously selling another futures contract against it. The futures spread trade acts as a hedging transaction altering the trader’s exposure from an outright price fluctuation, to the price differential between the individual legs of the spread trade. The profitability of a futures spread trade will depend of the price direction or differences in price movement for the legs of the strategy. Spread trades may be executed across many markets but traders often look at similar contracts, or related markets, for spread trading opportunities. A closer relationship between the spread markets means the individual legs are more likely to move in tandem enabling relatively stable price changes governed primarily by the pace of price moves between the legs (i.e., the relative performance of the legs), thereby reducing the level of risk for the trader. These strategies are referred to as relative value strategies.

Benefits of Spread Trading

Spreads may be broadly classified as intra-market spreads and inter-market spreads. Intra-market spreads, also known as calendar spreads are where a trader opens a long or short position in one contract month and then opens an opposite position in another contract month in the same futures market. Given the popularity of these spread trades as well as their contribution to futures rollover activity, dedicated calendar spread markets are available on the CME Direct platform which allows spread execution with no legging risk.

Inter-market spreads, involve two separate, but related, futures markets with the legs having the same maturity time frames. Inter-market spread strategies may have legging risk but can be mitigated by using dedicated inter-market spread contracts where available or by selecting liquid underlying contracts for each leg in conjunction using auto-spreading functionality offered by some software vendor trading screens.

The main advantages of spread trading are reduced volatility and lower margin requirements as the legs are generally in related markets at the same exchange. Compared to outright futures which can exhibit significant price swings, spreads can demonstrate extended trending price moves making it easier for traders to visualise patterns and thereby take a directional view or implement a technical trading strategy.

Spread Trading with Precious Metals

The precious metals complex includes gold, silver, platinum and palladium and offers trading opportunities to a global market through a wide variety of instruments available in the market such as the futures. These markets not only provide highly correlated commodities, but also each with some unique price drivers that can create many attractive spread trading opportunities. While market participants can choose from the range of instruments available for trade execution once they have identified their preferred strategies, the precious metals futures markets at CME Group offer highly liquid and deep markets that enable the fast, efficient execution of spread strategies with the additional benefits of considerable margin savings (as all trades are centrally cleared through CME Clearing) and much alleviated legging risk. More importantly, these futures contracts are predominantly electronically traded (over 90%) on CME Globex allowing easy access for participants across the world and high-quality trade executions virtually 24 hours a day.

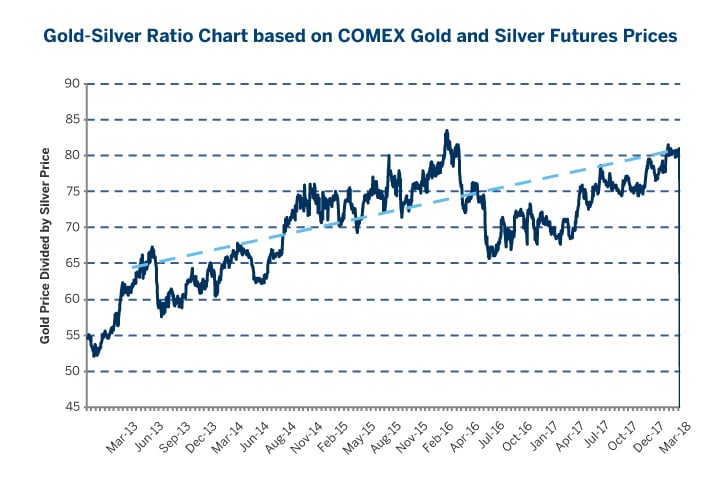

Gold-Silver Ratio Trade

The Gold-Silver Ratio, or GSR, indicates the price of gold relative to silver and is calculated as the price of gold divided by the price of silver on a per troy ounce basis. It reflects how many ounces of silver a single ounce of gold fetch. Since 2013 the ratio has widened out from 55 to 75, reaching a high of 83.5 in March 2016. In the last 2 years, the GSR traded within the range 65.5 and 83.5. Whilst both metals are considered precious and may trend together, gold is viewed as a global currency and often used as an inflation hedge and safe- haven asset in times of market uncertainty. Silver has more industrial applications and 50-60% is consumed in industrial end use compared with 10% of gold. Silver prices are sensitive to the economic cycle. The gold-silver ratio widens if gold prices experience a larger percentage gain relative to silver prices in times of economic or geopolitical uncertainty. Silver prices outperform gold in times of economic recovery as industrial demand picks up and puts the ratio under pressure. The ratio may be viewed an indicator of the health of the global macro economy.

Figure 1. Gold-Silver Ratio Chart based on COMEX Gold and Silver Futures Prices

{kind=link}

Silver prices are generally more volatile compared with gold prices (at time of writing, 20d historical volatility for gold and silver were around 9% and 19% respectively). When gold prices fall, silver prices are likely fall to a greater extent and vice-versa. Consequently, the gold-silver ratio tends to be driven on numerous occasions principally by moves in the price of silver.

Trading the gold-silver ratio a technical trader would look to determine a preferred point to enter and exit the spread. Fundamental traders, would assess the supply-demand imbalances and the macro conditions for each metal to take a directional view on the ratio before initiating a trade. Irrespective of the trading approach or a mix of both, the gold and silver futures contracts at COMEX offer cost-effective and highly liquid instruments for the GSR trade. The following screenshot for the most active COMEX gold and silver futures contracts on CME Globex shows extremely tight and liquid markets for the metals. The top of the order book is generally about 1 tick wide and there is abundant depth in the book beyond the top level for both the contracts.

| Contract | Gold Futures | Silver Futures |

| Product Code | GC | SI |

| Exchange | COMEX | COMEX |

| Contract Size | 100 oz | 5,000 oz |

| 2016 Average Daily Volume (lots) | 228,432 | 72,297 |

| Open Interest (lots, as of August 21, 2017) | 505,829 | 188,627 |

COMEX Gold and Silver Futures Order Book on CME Globex (at 12:00 pm ET on 21 August 2017)

Gold-Silver Ratio P&L Example – on March 1, 2017 a trader believes that gold prices will outperform silver prices in the short term. The trader decides to go long the gold-silver ratio by buying one April-17 gold futures contract (GCJ7) at $1,248.90/oz and simultaneously selling one May-17 silver futures contract (SIK7) at $18.445/oz thus keeping the notional amounts for the legs nearly similar ($124,890 and $92,225 respectively). The trader has thus initiated the GSR trade at 67.71. The following tables show the trader’s realised P&L should the GSR move in their favour (i.e., firms up).

- GSR edges higher by 1% when position is closed by selling one GCJ7 and buying one SIK7 simultaneously on March 30, 2017

| GCJ7 | SIK7 | |

| Trade Exit Prices | 1245.00 | 18.185 |

| Liquidate GSR @ | 68.46 | |

| Notional Amounts | $124,500 | $90,925 |

| Strategy Leg P&L | -$390 | $1,300 |

| Total P&L | $910 |

Margin Requirements – The strong correlation between gold and silver prices enables CME Clearing to provide significant margin offsets for opposite positions in COMEX gold (GC) and silver (SI) futures contracts. The margin offset applicable at present for GC and SI is 67% on a 1:1 basis that translates to an initial margin requirement of just 33% of the combined gross margin. At the time of writing, maintenance margin per contract for GC and SI was $4,250 and $5,400 respectively. Thus, for a long position in one gold futures contract and a short position in one silver futures contract, the total maintenance margin requirement will be $3,185 (($4,250+$5,400)*(1-0.67)) instead of $9,650.

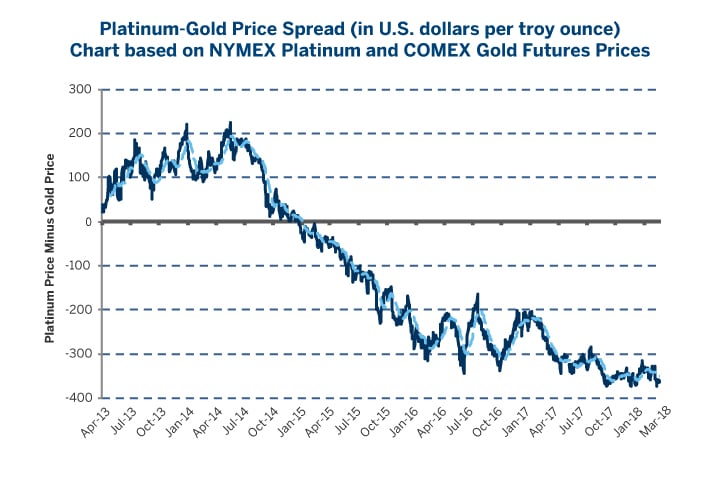

Platinum-Gold Spread Trade

Platinum is both a precious and industrial metal. It is widely used in catalytic converters in the automotive industry but also in jewellery and as an investment asset. The price relationship and the price spread between gold and platinum may be useful as an indicator of shifts in the macro environment. Historically, platinum has been more expensive than gold since the white metal is about 15 times rarer than gold and has a number of industrial uses compared to the yellow metal. However, gold can become pricier during times of economic distress and political uncertainty when the yellow metal sees increased demand as a safe-haven asset. Conversely, during a positive economic cycle with increasing automobile sales, platinum’s premium over gold prices can rise even further as the metal will see increased industrial use. Since 2015 Gold has been trading at a premium to Platinum and the spread has been widening.

Figure 2: Platinum-Gold Price Spread (in U.S. dollars per troy ounce) Chart based on NYMEX Platinum and COMEX Gold Futures Prices

{kind=link}

CME Group offers one of the most liquid platinum futures making it a very convenient instrument for the market to manage risk and instantly capture trading opportunities such as the platinum-gold price spread strategy.

| Contract | Gold Futures | Platinum Futures |

| Product Code | GC | PL |

| Exchange | COMEX | NYMEX |

| Contract Size | 100 oz | 50 oz |

| 2016 Average Daily Volume (lots) | 228,432 | 15,849 |

| Open Interest (lots, as of August 21, 2017) | 505,829 | 71,971 |

Platinum-Gold Spread P&L Example – On March 2, 2017 a trader expects platinum demand due to higher car sales to increase in the short term and the platinum-gold spread to narrow. The trader buys two April-17 platinum futures contracts (PLJ7) at $988.40/oz and simultaneously sells one April-17 gold futures contract (GCJ7) at $1,231.90/oz (the platinum contract is half the size, 50 oz of the 100 oz gold contract). The resulting notional amounts for the legs are $98,840 and $123,190 respectively. The trader has thus entered the spread trade at -$243.50 and is long the spread. The tables below show the trader’s realised P&L as negative spread widen further as both gold and platinum fell.

- Platinum-gold (negative) spread widens by 8% when position is closed by selling two PLJ7 contracts and buying one GCJ7 simultaneously on March 30, 2017

| GCJ7 | PLJ7 | |

| Trade Exit Prices | $1,233.60 | $971.40 |

| Liquidate GSR @ | -$262.20 | |

| Notional Amounts | $123,360 | $97,140 |

| Strategy Leg P&L | -$170 | -$1,700 |

| Total P&L | -$1,870 |

Margin Requirements – As with the gold and silver contracts, CME Clearing also offers a significant 58% margin offset for opposite direction positions in platinum and gold futures on 2:1 basis. The maintenance margin requirements per contract for platinum and gold futures are $1,600 and $4,250 respectively at present. With the offset accounted for, the maintenance margin would come to a total of $3,129 (($4,250+($1,600*2))*(1-0.58)) instead of $7,450 for a long position in two NYMEX platinum futures contracts and a short position in one COMEX gold futures contract.

Other Precious Metals Spread Trade

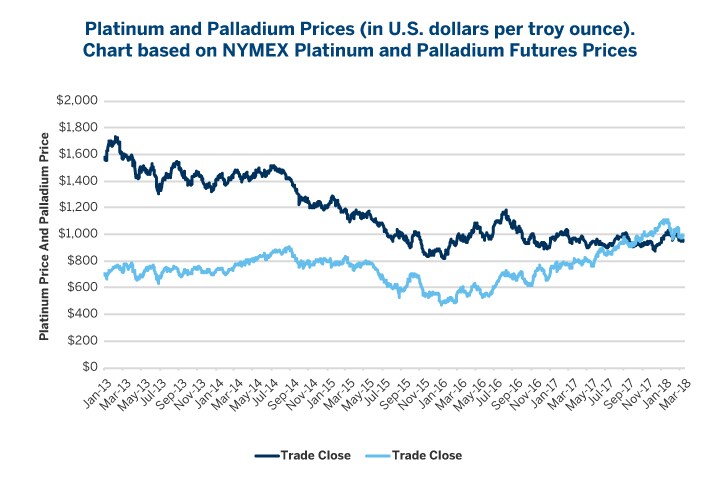

Palladium like platinum is also a precious metal widely used in the automobile industry as an auto catalyst. The difference being palladium is predominantly used in petrol engine vehicles whilst platinum is used in diesel engine vehicles. In the recent past, platinum has traded at a premium to palladium but as the chart below illustrates, the premium has narrowed. The spread may cross but the last time this happened was approximately 20 years ago. Traders can express a view on the platinum-palladium spread through trading individual outright futures contracts in a spread strategy like the ones demonstrated above.

Figure 3: Platinum and Palladium Prices (in U.S. dollars per troy ounce). Chart based on NYMEX Platinum and Palladium Futures Prices

{kind=link}

Outside of the metals complex, precious metals are frequently traded as a spread against other commodity futures contracts such as Crude Oil but also financial instruments such as Interest Rates and Foreign Exchange.

A complete list of CME Group Metals margins and offsets can be found at cmegroup.com/gold-margins.