{kind=link}

SOFR Futures for Risk Management: Growing by Leaps and Bounds

As adoption of SOFR-linked instruments accelerates, futures take the lead in risk management utilization.

SOFR futures expand access to Repo Rates

As the financial community moved toward consensus on a new benchmark for short-term borrowing costs, SOFR (recommended by the Alternative Reference Rate Committee (ARRC)) became appealing due to the tremendous size of the underlying transaction set, averaging nearly a trillion dollars daily notional with little variation. The market itself is generally the domain of the largest institutions, with major banks and money market funds as the main participants, and everyday customers gaining exposure to these markets indirectly through their personal holdings.

For the US Treasury market, CBOT Treasury futures have allowed those with hedging needs to participate without having to manage a portfolio of individual CUSIPs or worry about the tax or accounting implications of periodic coupons – all of these are priced into an instrument that can be exited from or rolled into the next expiry with relative ease.

Likewise, CME Eurodollar futures greatly expanded access and reduced costs of participation to those who needed to manage ICE LIBOR exposure without direct participation in the interbank lending market, and Federal Funds futures allowed participants to position themselves for changes in target rate policy.1

Risk transfer potential

For those looking to gain exposure directly to overnight financing rates, it can be helpful to see how large the liquidity pool is in terms of risk shifted between risk-averse hedgers and risk-seeking market makers. One popular measure is DV01, the dollar value impact of a single basis point move in interest rates (0.01%). In the same way that open interest is a proxy for potential trading partners, DV01 measures how much risk counterparties are exchanging and therefore how much potential for speculative or hedge trading.

The overnight repo market itself, while extremely large in notional trade activity, by definition has a term of one day which limits the risk involved for a shift in the annualized rate. So far in 2021, with an average daily notional of $918 billion, its DV01 is $255,000.2 CME SOFR futures by comparison average $3.3 million DV01 over the same time period, or around 13 times greater.3

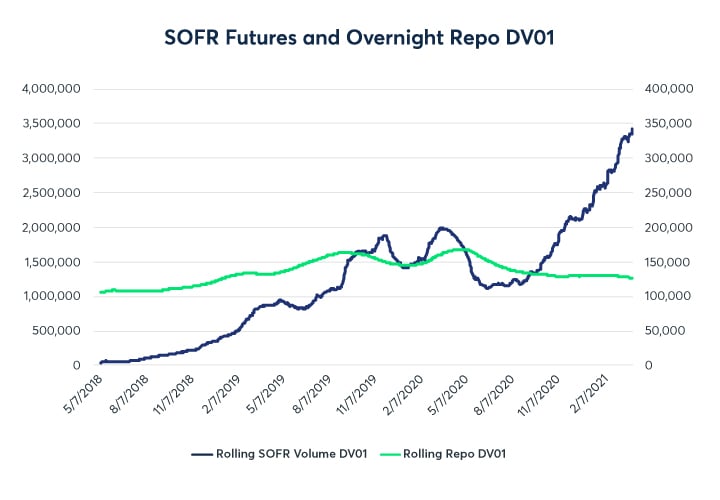

A three-month rolling average for SOFR futures and overnight Repo DV01 is shown in the below chart, since the inception of SOFR in May 2018. While the futures started out modestly, by late 2018 they had surpassed the repo market in risk transfer. In the graph below, note the righthand Repo axis is scaled down by a factor of ten to make the trend visible:

{kind=link}

Source: CME Group and NY FRB

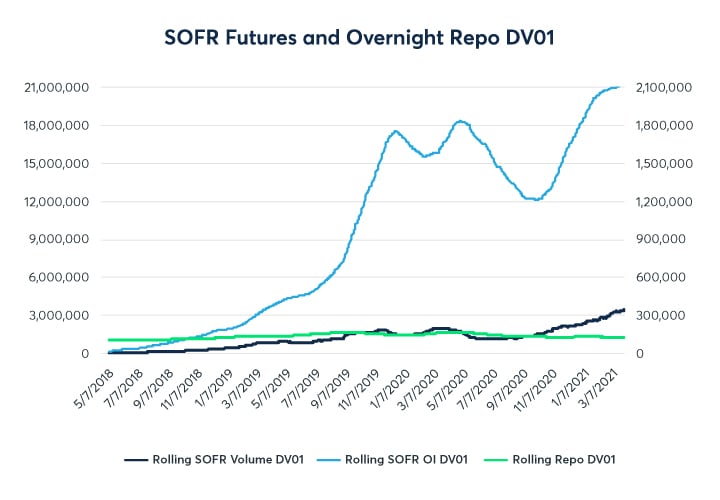

Because most repo positions are rolled from day to day, it may also be instructive to look to the risk transfer tied to SOFR futures open interest. Though overnight repo transactions are closed out each day, versus futures positions that can be exited or rolled, it gives some idea of the ratio of ongoing risk exposure.

By this measure, SOFR futures have averaged $21 million in DV01 for Q1 2021, a figure nearly 83 times greater than that of the overnight repo market. Placing it alongside the daily volume and repo numbers, even with the latter scaled by 10x, demonstrates just how significantly the futures contracts have grown as a tool for risk management.

{kind=link}

Source: CME Group and NY FRB

The future of futures

Because the pool of direct repo participants is relatively stable, as are funding needs, the transaction notional is unlikely to change very rapidly. This ensures a solid foundation for a benchmark, but also makes it unlikely its total risk managed will grow rapidly. CME SOFR futures, on the other hand, are in a period of rapid adoption and have a much broader audience of participants.

In fact, should ICE LIBOR’s cessation trigger a fallback to SOFR, an estimated $2.6 trillion in futures daily volume (as of March 29, 2021) would immediately be converted to SOFR futures, further accelerating their growth. In the absence of a fallback, most of this volume is nonetheless expected to migrate as ICE LIBOR’s use winds down, so it is highly likely that the DV01 will continue to climb, making SOFR futures the leading tool for risk management of overnight financing rates.

References

- CME Group Interest Rate products: /content/cmegroup/en/markets/interest-rates.html

- NY Federal Reserve Bank SOFR rates: https://www.newyorkfed.org/markets/reference-rates/sofr

- CME Group SOFR futures: /content/cmegroup/en/trading/interest-rates/secured-overnight-financing-rate-futures.html