{kind=link}

The ever-shifting Shanghai gold market landscape

Launched in October 2019, Shanghai Gold futures - listed on COMEX and available from CME Group, have now been tradable for two full years. The contracts are available both in dollar and offshore renminbi denomination. Activity in the contracts is continuing to grow. This can be seen in improved market liquidity as well as an increase of open interest to all-time record levels. At the same time, the effects of the global pandemic triggered new trading dynamics, with Shanghai Gold now often quoted at a discount to the Gold futures benchmark (GC) listed on COMEX.

Spread dynamics impacted by shifting fundamentals

In the years leading up to the launch of Shanghai Gold futures, the premium for Shanghai Gold over GC futures was a positive number that fluctuated narrowly around $5-10 per troy ounce. The premium was due to higher local demand for physical material in China, which had become the world’s largest physical gold market. Importers needed to pay over the global reference price to satisfy local Chinese demand, which is often linked to jewelry buying. Gold buying from the jewelry sector is by far the largest demand factor, often accounting for more than combined investment demand (investments in ETFs and in physical bars or coins)1.

The onset of COVID-19 changed this equation. Local demand for jewelry collapsed when the country went into lockdowns prior to the rest of world. This led to a Shanghai discount over global pricing. At its lowest point in Q3’20, Shanghai Gold was priced at a discount of more than $50 versus GC. Since then, however, the Chinese price has steadily recovered in strength, breaking into a premium environment again by the second half of 2021.

However, changing fundamentals during the summer months have had a negative impact, pushing Shanghai Gold premiums back into negative territory. Market watchers attributed this change to regional COVID outbreaks in China, weaker economic data, as well as devastating floods and its effects on investor sentiment. As we entered the fourth quarter of 2021, Shanghai gold prices have now strengthened again and trade broadly at the same level as GC (see chart 1).

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/q4/shanghai-gold-market-update-fig01.jpg

Source: CME Group

{kind=link}

It is noticeable how both the demand for jewelry in China and Chinese gold imports mirrored the evolution of the Shanghai Premium. China was the first country to be hit by COVID, which led to a collapse in jewelry demand and, at the same time, a precipitous drop in the Shanghai premium. After Q1’20, the country managed to increase demand for jewelry each following quarter right until Q1’21, when jewelry fabrication was particularly strong – this is also the time frame when the premium leapt into positive territory again. Q2’21 saw a drop in jewelry fabrication, and the premium switching into a discount again. Chinese non-monetary gold imports, which mostly include bullion gold, show a similar trend – a precipitous drop in Q’1 2020 that is now reversing (see chart 2).

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/q4/shanghai-gold-market-update-fig02.jpg

Source: MetalFocus (Jewelry fabrication data), Bloomberg (GLCNIM GACC Index)

{kind=link}

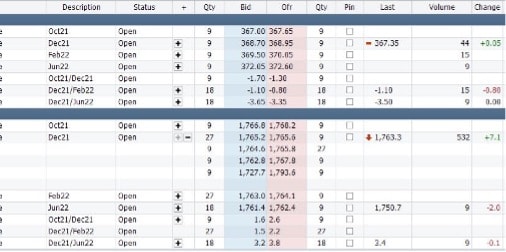

Improved market liquidity

Transparent liquidity during APAC and European trading hours provides participants the ability to execute desired volume across time zones. Market activity on CME Globex routinely provides access to 20+ lot markets at 0.30 CNH bid/ask, and 25+ lot markets at $0.6 bid/ask or better, on the USD-denominated contract during APAC hours.

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/q4/shanghai-gold-market-update-6.jpg

Source: CME Direct at 1030 SGT/HKT on October 13, 2021

{kind=link}

Similar liquidity is available during European trading hours as well.

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/q4/shanghai-gold-market-updatefig07.jpg

Source: CME Direct at 1545 BST on October 12, 2021

{kind=link}

Historic trading data also shows that liquidity and order book width has improved both for the USD and CNH denominated futures. During the main market hour in Asia (2pm Beijing time), the active month SGU contract was traded at an average top of book spread of 1$/oz. during September, with an average of 30 contracts available across the first three top levels of the order book (chart 3).

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/q4/shanghai-gold-market-update-fig03.jpg

Source: CME Group

{kind=link}

SGC data also shows a comparable market liquidity, with more than 20 lots available across the top three levels of the order book. The top of book bid/ask spread is slightly less tight than SGU at an average of 1.75 $/oz equivalent over the past three months (see chart 4).

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/q4/shanghai-gold-market-update-fig04.jpg

Source: CME Group

{kind=link}

Open Interest on the rise

Open interest (OI) is on the ascendency in both the USD- and the CNH-denominated contracts. For the first time, the total open interest of both contracts briefly surpassed 1,400 contracts in late August ‘21, equivalent to a notional value of $80M. The growth in OI is well balanced, and each contract accounts for about half of open positions held at the exchange. As of mid-October, total open interest stood at 1,100 contracts (640 SGU and 460 SGC contracts), equivalent to about $60M notional value (see chart 5).

https://www.cmegroup.com/content/dam/cmegroup/education/images/2021/q4/shanghai-gold-market-update-fig05.jpg

Source: CME Group

{kind=link}

Summary

Shanghai Gold futures listed on COMEX and offered by CME Group continue in their path towards maturity. The contracts have found good support by market participants, as demonstrated by deeper market liquidity and an increase in open interest. The Chinese market remains a fundamental part of the global gold trading landscape. More and more, investors are embracing Shanghai Gold futures as an efficient instrument to access this region and unlock trading opportunities around the world’s largest physical market for gold.