{kind=link}

Renewable Fuels Demand Stimulates Hedging Opportunities

Europe’s energy markets are entering a period of significant change as new low carbon intensity feedstocks become much more actively traded. At the same time, some of the more traditional hydrocarbon and vegetable oil feedstocks may fade into the background as member states strive to achieve the targets laid out by regulators.

The Renewable Energy Directive (RED) ensures that all European member states fulfil at least 20% of their total energy needs with renewables by the end of 2020. Additionally, a 10% renewable fuels mandate for road transport fuels was also implemented, boosting demand for renewable biofuel products. The Renewable Energy Directive II1 (RED II), is set to come into force from January 1, 2021 (to the end of 2030) and further increases the road transport blending target from renewable fuels to 14%. A higher overall binding renewable energy target of 32% has also been set by RED II which includes sectors like electricity, heating and cooling. These volumetric targets are now being overtaken by net zero pledges on carbon emissions made at the corporate and national government levels across Europe as governments seek to stay on track to their Paris climate commitments. Pursuit of a transition to a “circular economy” prioritising the repurposing of waste products as energy feedstocks is the key pillar of Europe’s new “Green Deal” commitment to funding a post coronavirus recovery.

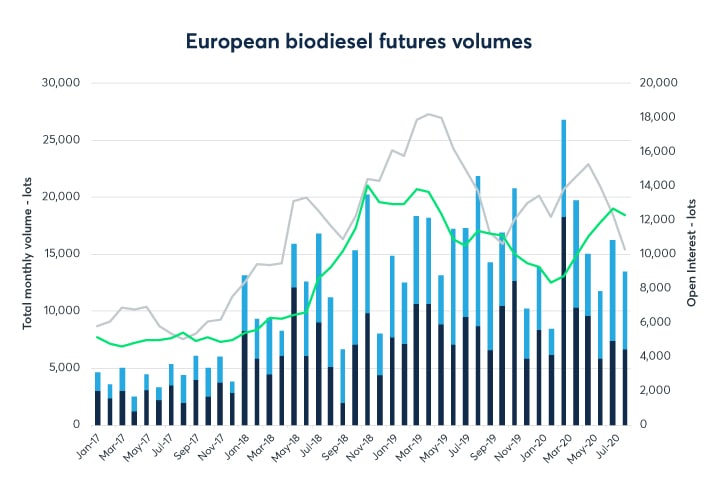

European biodiesel futures show robust growth

The current European benchmarks for biodiesel are Rapeseed Methyl Ester (RME) and Fatty Acid Methyl Ester (or FAME 0). Traded futures volumes year to date August 2020 were 125,000 lots or 12.5 million tons, about 7% lower than the same period 12-months earlier. It remains unclear how much of the current volumes in both FAME 0 or RME might transition to alternative renewable fuel-based products such as waste oils as the RED II implementation period gets underway from 2021.

{kind=link}

Source: Exchange data

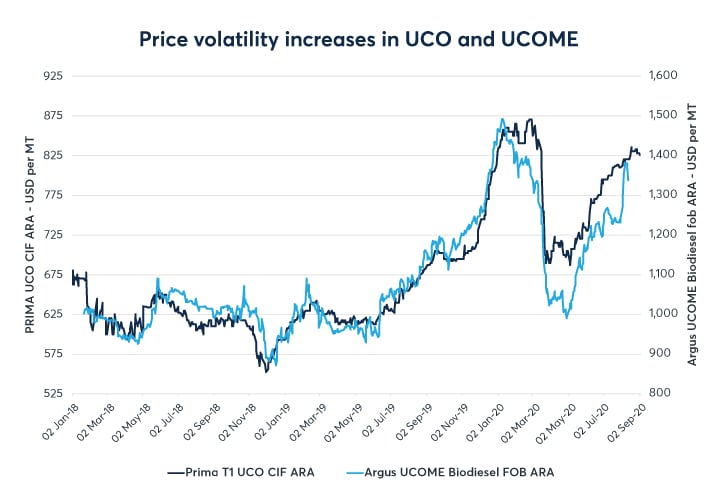

Renewable fuel price volatility increases

To manage heightened levels of volatility, new lower carbon benchmarks are being developed by exchanges like CME Group to avoid unnecessary basis risk for hedgers looking to manage price risk between the new low carbon products and the long-established futures benchmark products.

European Used Cooking Oil Methyl Ester (UCOME) prices and the underlying feedstock prices have remained volatile, in part due to the uncertain supply. Shortages have been caused, in part due to the large number of restaurants and other fast food outlets that have been forced to close due to the coronavirus pandemic. These government-imposed shutdowns have particularly impacted used cooking oil (UCO), the underlying feedstock to UCOME. Supplies are expected to remain volatile as governments struggle to deal with the impact of the coronavirus pandemic with different locations re-opening at different times. UCOME prices have also not been immune from the collapse in demand for road transport fuels directly resulting from the impact of the coronavirus pandemic.

As traders look to cover these price risks, a greater role for these new feedstocks seems likely. Larger interest in new low carbon-based products may also help support pledges by European governments to ensure compliance with tougher RED II targets.

{kind=link}

Source: Prima markets (UCO) and Argus Media (UCOME)

Biofuel markets, a boost for waste oils

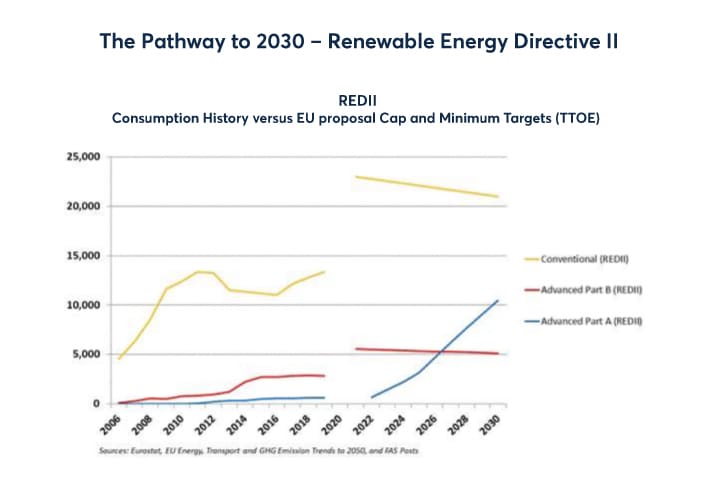

The size of the European biofuels market was about 15.2 million tons in 2019, an increase of 3% versus 2018, according to the U.S. Department of Agriculture2. European governments have already committed to increase the use of renewable fuels under RED but much more stringent targets have been laid out from 2021 onwards due to RED II. This will potentially mean less use of traditional agricultural feedstocks such as rapeseed oil or soybean oil and increased demand for second generation biofuels such as algae and waste-based fuels. As the renewable directives evolve through the advent of RED II, non-food and waste-based oils are expected to play a more significant role in Europe’s changing energy mix.

Importantly, RED II places a cap on the share of food-based biofuels for each member state to one percent above the total consumption level in the year of 2020 to an overall cap of seven percent of final consumption of road and rail transport for each member state. This will limit the amount of rapeseed oil methyl ester and palm and soy based fatty acid methyl ester than can be used in the biofuel sector.

{kind=link}

Source: USDA EU Biodiesel report 2019

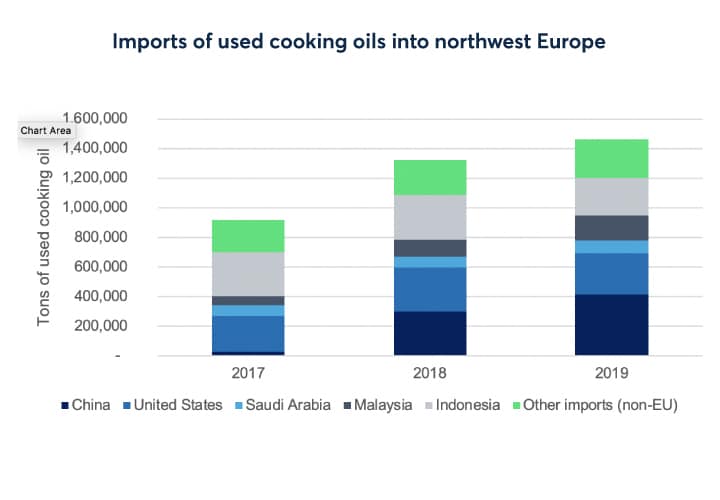

Waste oils count double

RED II requires all member states to increase the volume of waste oils in road transport fuels to 1.7% for the first time. This is expected to boost demand for products like used cooking oils (UCO). Therefore, the import dependency from countries such as China is expected to increase as it is the world’s largest supplier of the feedstock.

Under RED II, traditional food-based feedstocks are expected to be capped at around 7% with the remaining volumes achieved by using so-called double counting feedstocks, listed under Part A of Annexe IX of RED II3. These are typically products like palm oil mill effluents, algae, tall oil pitch and glycerine provided they contain sufficiently high greenhouse gas savings (GHG) of around 65% for transport fuels and 70% for electricity, heating and cooling4. The term double counting refers to the usage benefits meaning that countries that allow for it can permit companies to use halve the volumes of certain feedstocks that “double count” towards the stated targets.

A selection of advanced feedstocks listed under Annexe IX part B5 will double count towards both the 3.5% advanced biofuel target and the 3.5% double count target for fungible streams of UCO and other animal fats. These products are also double counted to increase their monetizability versus vegetable oil-based biofuels. In the biodiesel markets, the USDA estimated that around 22% of the feedstocks was used cooking oil. China, Indonesia, Malaysia, and the United States are the largest suppliers of UCO with the collectors exporting volumes into northwest Europe for the biofuel producers. UCOME has much higher GHG savings of around 87% compared with the traditional FAME 0 and RME biofuels where the GHG savings are closer to 60%. Countries like Germany and Sweden measure the renewable content of feedstocks based on their GHG savings therefore this becomes an important factor for countries that adopt it.

Conventional European renewables mandates calibrated by the percentage of the biofuel blend required are being supplemented by greenhouse gas mandates. These are likely to eventually supersede volumetric mandates in a world where all energy products are valued according to how little carbon they emit. This again advantages waste feedstocks such as UCO. These developments plus net zero carbon pledges at oil majors are driving a stampede to build new refinery scale assets capable of converting waste feedstocks into direct low carbon substitutes for diesel called HVO. These assets are increasingly driving demand for used cooking oil and other waste fats.

Some traders believe that demand for used cooking oil could rise to as much as 11 million tons per year by 2030. These higher volumes will have to be met from rising imports from outside the European Union combined with higher domestic production.

{kind=link}

Source: Eurostat data

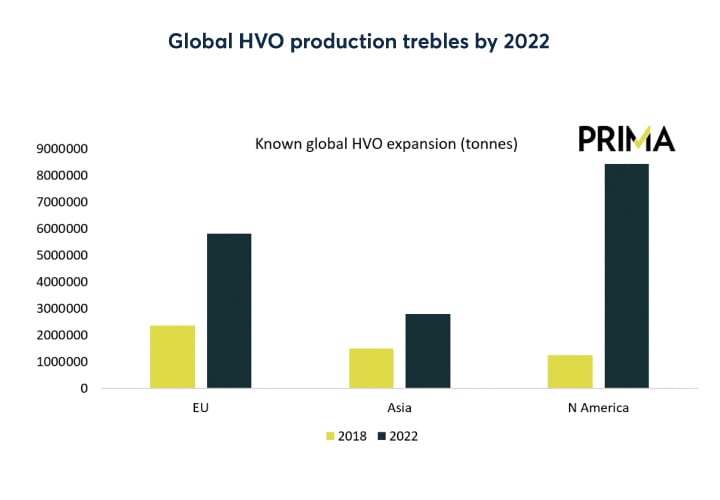

Hydrotreated Vegetable Oils to grow?

Hydrotreated Vegetable Oil (HVO) can be produced from any vegetable oil, animal fat, or used cooking oil and can be fully substituted for petroleum products such as kerosene or diesel. Transport companies have been looking at HVO as a way of increasing their green credentials since it produces very low carbon emissions.

The USDA report on European biofuels6 shows that HVO production in 2019 was around 3 billion litres, up from 2.8 billion litres in 2018. Some estimate that production for 2020 and beyond may rise but this depends on the demand for road transport fuels post the coronavirus pandemic. Whilst some producers have committed to increasing production volumes, others may face cash constraints and therefore may pare back their ambitions. Capacity is still expected to grow by multiples over the next several years as new units are brought on line. However, this may lead to further price volatility in the years ahead therefore further underlying the need to manage these price risks appropriately.

{kind=link}

By the end of 2021, total HVO production could reach 4.5 billion litres, an increase of 150% on 2019 levels, the USDA report claimed.

As many international governments have publicly stated their aims of reducing carbon emissions to net zero by 2050, renewable fuels look set for a bright future. A combination of traditional biofuels and less conventional feedstocks such as used cooking oils and others are one part of the solution towards achieving net zero carbon emissions by 2050. The launch of lower carbon benchmarks for these growing markets will likely further support the development of the sector. Futures can provide greater price transparency beyond the short-term physical trading. With a greater degree of price transparency on the futures curve, companies may see greater opportunities for price risk management. These changes should further assist the energy transition towards the previously stated aim of net zero carbon emissions by 2050.

1 European Renewable Energy Directive II https://apps.fas.usda.gov/newgainapi/api/report/downloadreportbyfilename?filename=Biofuels%20Annual_The%20Hague_EU-28_7-15-2019.pdf

2 USDA EU Biofuels Annual 2019 https://apps.fas.usda.gov/newgainapi/api/report/downloadreportbyfilename?filename=Biofuels%20Annual_The%20Hague_EU-28_7-15-2019.pdf

3 RED II Part A and B of Annexe IX (page 11) https://apps.fas.usda.gov/newgainapi/api/report/downloadreportbyfilename?filename=Biofuels%20Annual_The%20Hague_EU-28_7-15-2019.pdf

4 USDA Report – Biofuel mandates in the EU by member state in 2019 https://apps.fas.usda.gov/newgainapi/api/report/downloadreportbyfilename?filename=Biofuel%20Mandates%20in%20the%20EU%20by%20Member%20State%20in%202019_Berlin_EU-28_6-27-2019.pdf

5 Renewable Energy Directive II (RED II) Annexe IX Part A and Part B https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2018.328.01.0082.01.ENG&toc=OJ:L:2018:328:TOC

6 USDA Report – European biofuels https://apps.fas.usda.gov/newgainapi/api/report/downloadreportbyfilename?filename=Biofuels%20Annual_The%20Hague_EU-28_7-15-2019.pdf