{kind=link}

Relationship between Major Grain Commodity Benchmarks and Equities Prices During Economic Downturns

It is widely accepted that the principal benefit of including commodities in investment portfolios includes low correlation with other asset classes (equities and fixed income) and positive returns over time. What is less known and looked at is how economic downturns impact the correlations between equities and major grain commodity benchmarks such as CBOT Corn, Wheat and Soybeans futures. This brief will attempt to uncover and unpack some of the nuances that emerge between these dynamic relationships during recessions.

In February 2020, the US economy officially fell into recession, according to the National Bureau of Economic Research (NBER), the official arbiter of recessions in the US. This ended what was officially the longest recorded expansion of the US economy, which lasted 128 consecutive months. In a statement the committee concluded “…the unprecedented magnitude of the decline in employment and production, and its broad reach across the entire economy, warrants the designation of this episode as a recession, even if it turns out to be briefer than earlier contractions.”

While this recession bears unique and differing characteristics to past recessions due to the pandemic and public health response, the theories and literature proposed by economists such as Irwin and Sanders (2010) and Cheng and Xiong (2014) can help us better understand the mechanism which connects and influences the correlations between these key commodity benchmarks and equities.

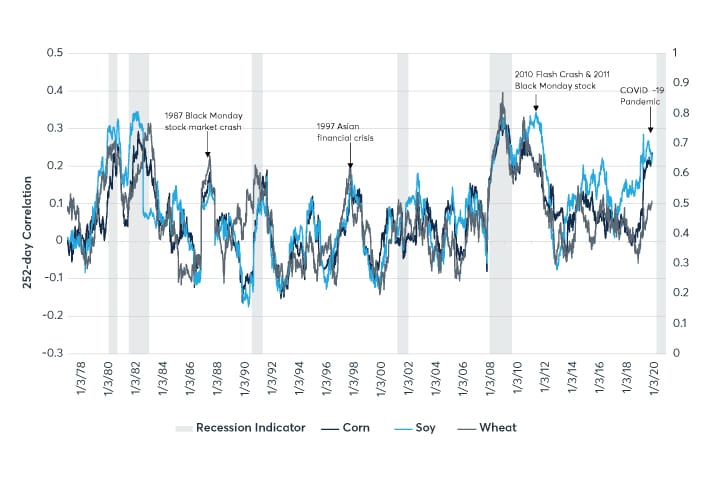

Figure 1 shows a 252-day lagged correlation of real returns between CBOT Corn, Wheat, and Soybean futures’ prices and the S&P 500 Index going back to 1977. The prices, and thus returns, have been adjusted using the US Bureau of Labor Statistic’s Consumer Price Index (CPI 1982-1984).

Figure 1. Trailing 252-day correlation of returns: S&P 500 vs. Grain futures (CPI Adjusted)

{kind=link}

Source: Federal Reserve Bank of St. Louis and CME Group

Apparent from Figure 1 is the tendency for heightened correlations of returns between these key agricultural commodity benchmarks and their equity-based counterpart index during times of financial distress. So, what is connecting these seemingly unattached markets?

While many point to the “financialization” of commodities through the creation of Commodity Index Funds starting in early 2000, data and economic literature such as Bjornson and Carter (1997) suggest commodity futures markets have long been integrated with financial markets for decades. Examining seven commodity futures markets from 1969-1994, the authors concluded commodities provide a natural hedge against business cycles with lower returns expected during times of high interest rates, expected inflation, and economic growth.

In their work, Irwin and Sanders (2010) highlight several potentially contributing factors to heightened correlation between equities and commodities, including: demand growth from China and other developing countries, biofuel policies, monetary policy, trade restrictions, and supply shortfalls.

Cheng and Xiong (2014) propose the three following preponderant economic mechanisms of commodity markets which explicitly and implicitly connect them to global financial markets:

- Theory of storage – Basis in futures markets are directly related to the cost of storing said commodity, including financing and warehousing. This is known as the cost of carry, which creates an arbitrage mechanism in commodity futures markets. If the spread between futures’ delivery months is greater than theses accumulated costs, a trader may buy the commodity in the spot market, short a futures contract, and “carry” the commodity to delivery for a profit. Through this concept the factors that influence the costs of carry/inventory, including nominal interest rates and monetary policy, impact commodity prices.

- Risk sharing – Part of the advent of commodity futures markets was to facilitate the allocation of commodity price risk between those with exposed price risk (farmers and producers) and those willing to take on risk as an investment (hedge funds and liquidity providers). Several studies have shown this relationship to be dynamic during times of financial distress, with market participants demonstrating time-varying risk appetite behavior. Whoever has the strongest incentive to trade, is typically the ones driving price movement at any given point in time. During times of financial distress, risk-bearing capacity is often reduced and has the potential to cause investment traders to unwind positions.

- Information discovery – Commodity futures markets typically act as aggregators of information which reflect on the global supply and demand of their underlying commodity markets. However, due to the informational frictions that exist within supply chains that stretch across multiple continents and countries, commodity futures markets also act as bellwether for global economics. A strengthening of commodity prices may be indicative of increased demand and thus global/regional growth, and vice versa.

In general, and as demonstrated in Figure 1, commodity futures returns can create diversification with an often-negative correlation to stock returns. However, during times of financial distress, the theories and mechanisms examined above can help us understand how and why these markets integrate and interact. The onset of the global pandemic and public health care response will add a new chapter to this ongoing saga, one that will require and inspire updates to the research cited above.

Sources:

Bjornson, Bruce, and Colin A. Carter. 1997. New Evidence on Agricultural Commodity Return Performance under Time-Varying Risk. American Journal of Agricultural Economics 79(3): 918–30.

Cheng, Ing-Haw and Xiong, Wei. 2014. Financialization of Commodity Markets. Annual Review of Financial Economics 6: 419-441.

Irwin, Scott H. and Sanders, Dwight R. 2010. Index Funds, Financialization, and Commodity Futures Markets. Applied Economic Perspectives and Policy 00(00): 1-31.