{kind=link}

Relationship Between Global Soybean Prices

As Brazil emerged as a predominant exporter of soybeans over the last two decades, commercial entities with physical exposure in both Brazil and the United States have had to learn how to properly manage their risk. Historically, Brazilian soybeans were hedged using the benchmark CBOT Soybean futures contract and/or the Paranagua paper market. However, under some market conditions, the CBOT Soybean futures contract and the Paranagua paper market did not perform as an effective hedging instruments for certain participants. Production mismatches between the northern and southern hemispheres can affect the relationship between CBOT Soybean futures and the price for Brazilian soybeans. The Paranagua paper market is primarily a tool used to manage basis risk, but as a paper market, it can be difficult to trade for all market participants. Over time, the correlation between Brazilian soybeans and CBOT Soybean futures has been high, but this relationship can break down periodically ‒ increasing price risk in South America. Episodes of reduced correlation may be increasing in frequency as macro-shifts in trade flows have created differing market dynamics between Brazil and the US.

Highlighting the growing need for a South American-based price risk management tool, this paper addresses the relationship between the prices of soybeans in major importing and exporting countries and demonstrates the usefulness that a cleared South American futures contract could bring for managing global soybean price risk.

Brazilian & US correlations

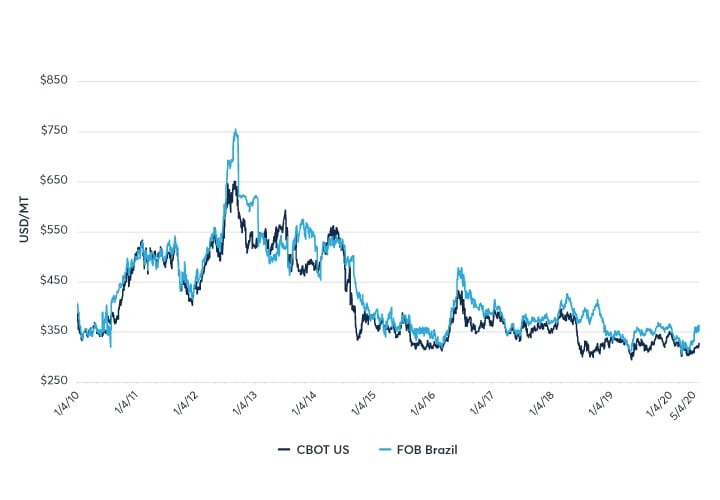

As stated previously, without a specific instrument for managing Brazilian price movements, most entities with global soybean exposure use the benchmark CBOT Soybean futures contract to hedge. In general, Brazilian soybean prices move in sync with CBOT Soybean futures prices to effectively manage South American risk. Figure 1 shows the relationship between Brazilian soybean export prices at the port of Paranagua1 and the nearby CBOT Soybean futures price over the last ten years.

Figure 1: FOB Brazil vs. CBOT Futures

{kind=link}

Source: CME Group & Bloomberg

In commodity export markets, the Law of One Price assumes price equalization in the long run for identical commodities (such as soybeans) sold in different locations under certain conditions, including the absence of trade frictions. This means that, over time, there typically exists a stable relationship between the prices of major commodity export hubs that allow traders to make and execute decisions based on these relationships. Today’s soybean export markets are evolving beyond the law of one price. The price relationship between free on board (FOB) Brazil export prices and the prevailing US-based CBOT Soybean futures price has become less stable over time. While the causes for this are likely multifactorial, the relationship has become especially tumultuous due to US-China geopolitics and the lasting impacts of the Trade War as can be seen in Table 1 below.

Table 1. Two-year Correlations (R-squared) from 2010-Current2 :

| Time period | R-squared (correlation) |

| 2010-2011 | 0.95 |

| 2012-2013 | 0.57 |

| 2014-2015 | 0.87 |

| 2016-2017 | 0.79 |

| 2018-2020 | 0.35 |

Table 1 shows the correlation between Brazilian export prices and nearby CBOT Soybean futures diminishing over the past ten years. It is crucial to note that the correlation, while variable, appears to decline before the US-China trade dispute, starting around 2012. This can be attributed to fundamental supply and demand factors disrupting a relationship that had previously been highly linked.

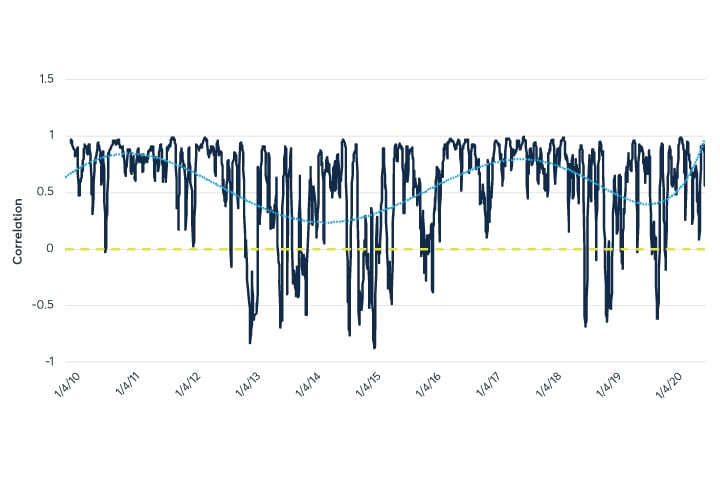

Another way of observing the disruption of the historically strong correlation between FOB Brazil and CBOT Soybean futures is shown by the 20-day moving average correlation in Figure 2 using price levels. While at times the correlation is trending towards one, this graph also shows there is a historic pattern and a tendency for the correlation to vary and lose effectiveness for short durations of time. In effect, this highlights the need for a derivative that directly reflects the prevailing price of soybeans in South America.

Figure 2. 20-day Moving Correlation (Levels), FOB Brazil vs. CBOT Soybean Futures:

{kind=link}

Source: CME Group & Bloomberg

Seasonality

The relationship between US and Brazilian soybean prices seems to fluctuate depending on which country is in its export season. The correlations in Table 3 between CBOT Soybean futures and FOB Brazil prices during each country’s respective export season suggests that price correlation between the two strengthens from March through August (Brazil export season) relative to September through February (US export season).

Table 2. US-Brazil Seasonal Correlations (R-squared):

| US export months (Sept-Feb) | Brazilian export months (Mar-Aug) | |

| 10-year | 0.899 | 0.920 |

| 5-year | 0.368 | 0.683 |

| 3-year | 0.180 | 0.541 |

The strengthening correlation during Brazil’s export season suggests CBOT Soybean futures do a good job pricing the marginal ton of soybeans on the global market. However, the data also show, as above, that the recent in-season relationship is not as strong compared the five- and 10-year relationships.

Similarly, observing the three-year correlations between Chinese and Brazilian prices during the US and Brazilian export seasons suggests that the landed Chinese soybean price has a stronger correlation to the FOB Brazil price during the Brazilian export season, relative to the US export season. This can be attributed to the Brazilian physical price exposure that Chinese importers face from March through August. As the largest buyer of soybeans in the world year-round, during this time period, most of China’s supply is sourced from Brazil.

Table 3. China-Brazil Seasonal Correlations (R-squared):

| US export months (Sept-Feb) | Brazilian export months (Mar-Aug) | |

| 3-year | 0.289 | 0.4737 |

Basis volatility

Basis represents the difference between spot cash prices and the nearby futures. Basis volatility is one method of evaluating basis risk, or the chance the underlying cash price and the offsetting hedge becomes unstable. Lower basis volatility is indicative of a stable relationship between cash and futures, while higher basis volatility is indicative of the opposite. The less stable the relationship between cash and futures, the greater the potential for excess gains or losses in a hedging strategy - thus adding more risk to the position.

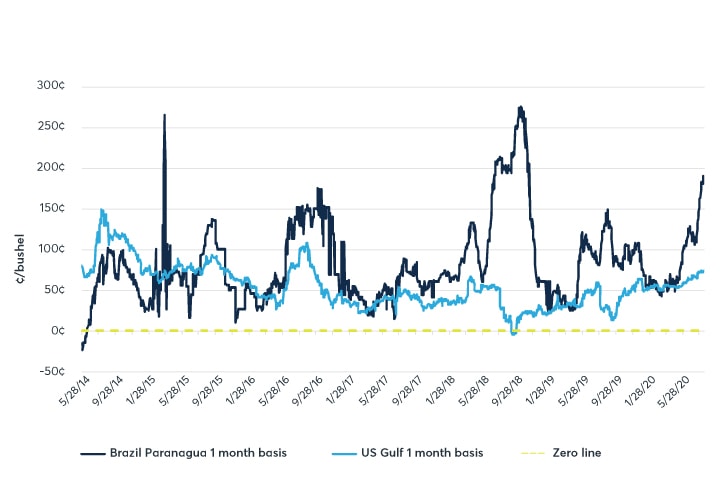

Figure 3. Basis Volatility: FOB Brazil vs. FOB US Gulf

{kind=link}

Source: CME Group & Bloomberg

Figure 3 above looks at the basis in two cash markets – the Paranagua port cash price minus nearby CBOT Soybean futures and the US Gulf cash price minus nearby CBOT Soybean futures. This chart clearly demonstrates that the Brazil basis is more volatile relative to the US Gulf basis.

Table 4. 1-Standard Deviation from Mean, FOB Brazil Basis vs. FOB US Gulf Basis (May 2014-Current)

| All dates | Trade war removed | |

| FOB Brazil | 51¢ | 39¢ |

| FOB US Gulf | 26¢ | 25¢ |

Table 4 shows that the variability in the historic FOB Brazil basis is almost double that of the FOB US Gulf basis. Removing the trade war dates to account for non-fundamental market information shows similar findings, with basis variability falling for the FOB Brazil basis. Combing the information from Figure 3 and Table 4 shows the historical relationship between FOB US Gulf and the CBOT Soybean futures price has been much more stable relative to its Brazilian counterpart.

Brazilian basis volatility speaks to the growing need for regionalized tools specific to Brazilian price risk and signals while also providing an interesting trading opportunity for financial participants.

South American Soybean correlations

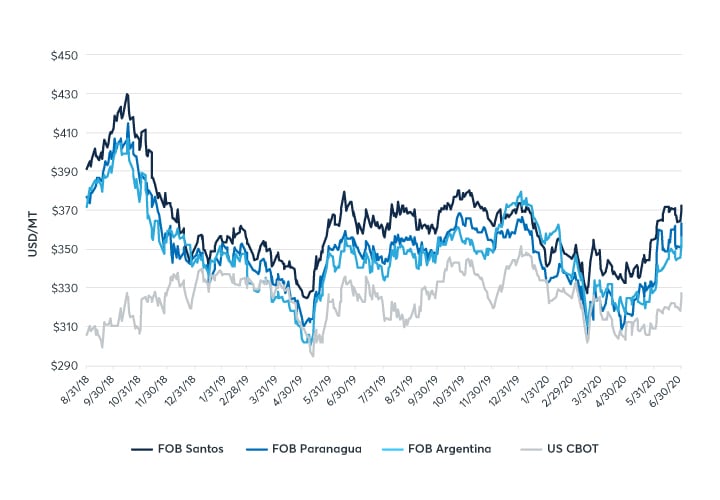

Although the South American soybean futures product will follow the export price at the Brazilian port of Santos, it is representative of the price of beans in other significant South American soybean producing countries. The Platts Santos price is highly correlated with soybean prices at the Paranagua port, as stated earlier, but is also highly correlated to soybean prices in Argentina –since its inception, the correlation between the Platts Santos assessment and Argentine cash soybean prices is 80 percent.

Figure 4. FOB Santos vs. South American Soybean Prices vs. US CBOT

{kind=link}

Source: Platts, Bloomberg & CME Group

Comparatively, the US-based CBOT Soybean futures price correlations to both Paranagua and Argentina during this period were below 10 percent ‒ suggesting that a South American Soybean futures contract will be a valuable tool for better managing regional price risk.

Relationship to China

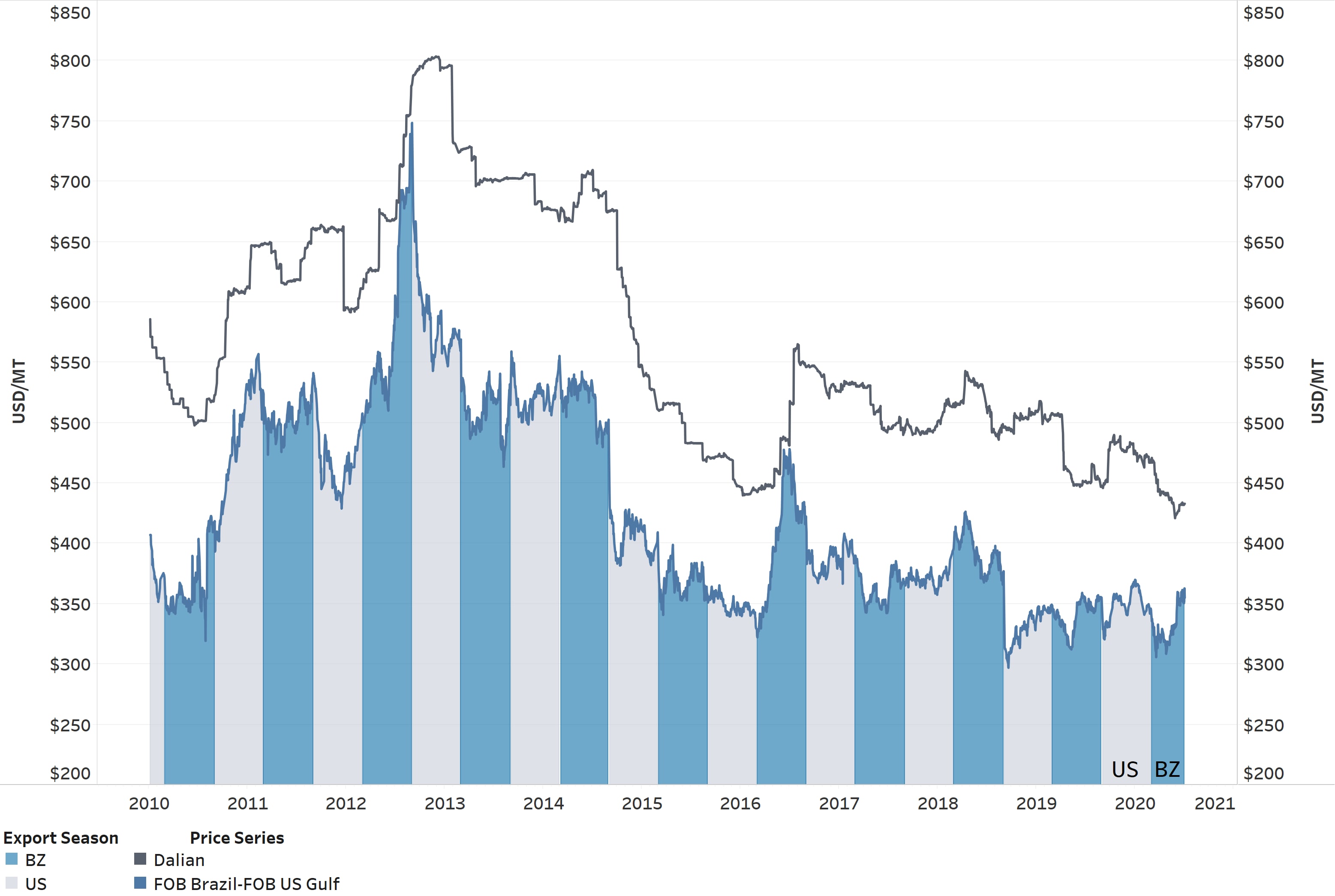

The long-term relationship between the Dalian Spot Cash price and a combined FOB U.S. Gulf/FOB Brazil price3 suggests, in the absence of non-fundamental trade frictions or supply/demand shocks, the Chinese benchmark is strongly tied to the prices in the predominant export origin. Over the last ten years, the correlation between Chinese prices and seasonally-adjusted export prices is nearly 82%.

This strong correlation suggests that Chinese imports can be effectively hedged with two risk management tools over the course of an entire calendar year. Depending on the marketing season, a Chinese importer could use a US-based risk management tool during US export season and a Brazil-based risk management tool during Brazilian export season. Figure 5 shows this relationship between the US and Brazil export seasons and how this relationship remains consistent over the long term.

Figure 5. Chinese Spot Cash vs. Origin Price

{kind=link}

Source: Bloomberg

In summary, the introduction of the regional Platts Santos Soybean futures contract fills a market need to increase hedge effectiveness for South American soybean risk. With the correlation between Brazilian prices and CBOT Soybean futures becoming less certain, a Brazilian based contract allows for a more direct risk management tool with an added benefit of high correlations with other South American cash prices. Lastly, with two derivatives that cover both major soybean exporters over the course of an entire calendar year, global soybean participants have the necessary tools to manage most of their exposure.

1 The South American soybean futures contract will be based on a Platts assessment of exports from the port of Santos. However, Platts only began publishing this assessment in 2018, and longer-term data was warranted for this analysis. The Paranagua export price is highly correlated with the Platts Santos assessment (94% correlation), so it was used as a proxy for many calculations.

2 Ordinary least squares (OLS) was used to regress price levels. The results presented in Tables 1, 2, 3, and 4 were cointegrated based on Engle-Granger two-step method. Ultimately, using an Augmented Dickey Fuller (ADF) to test for stationarity helped determined price level data could be used. Cointegration of two nonstationary series indicates a non-spurious relationship. If two nonstationary series are cointegrated, OLS regression statistics may be done on price levels and still hold true.

3 This continual price series was formed using a combination of FOB U.S. Gulf and FOB Brazil prices, depending on the which origin was in export season. For the months of March through August (Brazilian export season), the Brazilian price was referenced, and for the months of September through February (US export season), the US price was referenced.