{kind=link}

RBOB Gasoline in driving seat for global ethanol push

Global transport accounts for about 24% of carbon emissions and road transport represents nearly 75% of this total, according to the International Energy Agency (IEA).1 It is not surprising that governments are focused on reducing the overall level of carbon emissions. Renewable ethanol, made from corn, wheat, sugars and other cereal crops, is expected to play a key role in the realization of the European Union’s (EU) energy and climate ambitions.

Higher blends of ethanol in gasoline have been introduced in many countries across Europe, which has reduced the contribution of fossil fuels into the gasoline pool. For this to be fully realized, the chemical makeup of the blendstock may be adjusted to remove additional oxygenates to allow for a higher proportion of ethanol. Such moves throw open the possibility that the European gasoline market may become more compatible with the United States, which may expand the pricing role that RBOB gasoline futures has on the international stage. The US finished grade gasoline market already operates on a largely 10% or so-called E10 market.

A widespread transition to E10 in the international markets will make the transporting of cargoes into the United States much easier as the blendstocks arriving from markets such as Europe into the United States can be adjusted so that cargoes can be blended with the higher ethanol quantities on arrival. Traders have said that a broader move to E10 on a global scale is likely to see greater trading opportunities to be able to hedge in the liquid RBOB Gasoline futures markets (alongside some of the existing regional benchmarks).

The demand for ethanol looks set to increase alongside the tighter blending mandates, and a move to E10 will double the amount of ethanol being consumed compared to E5. As more countries transition to higher ethanol blending requirements, increased trading of ethanol futures and options is expected as traders look to manage any price risks in the physical market.

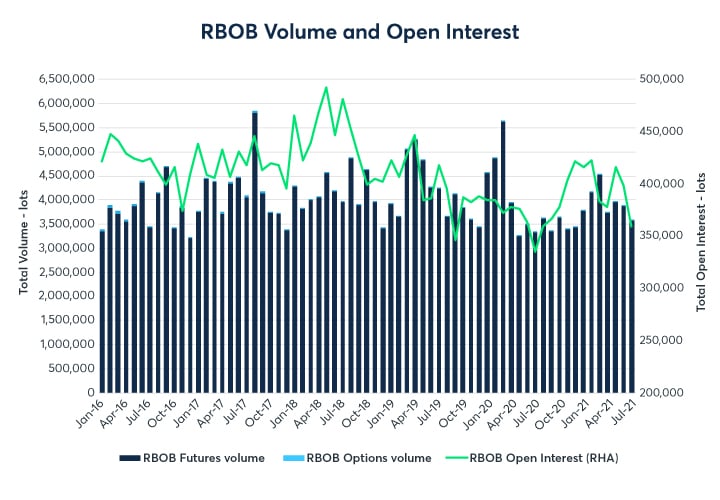

Chart 1: RBOB Gasoline futures trading interest remains robust

{kind=link}

Source: CME Group data

RBOB Gasoline is the world’s most liquid gasoline futures contract as it is the only gasoline futures contract to trade electronically around the clock. Average daily volume in RBOB Gasoline futures is around 200,000 lots per day or 3.6 million lots per month. Spreading RBOB futures against the regional cash markets in Europe for Eurobob or Singapore Mogas 92 is a common way to handle price risk in physical trade.

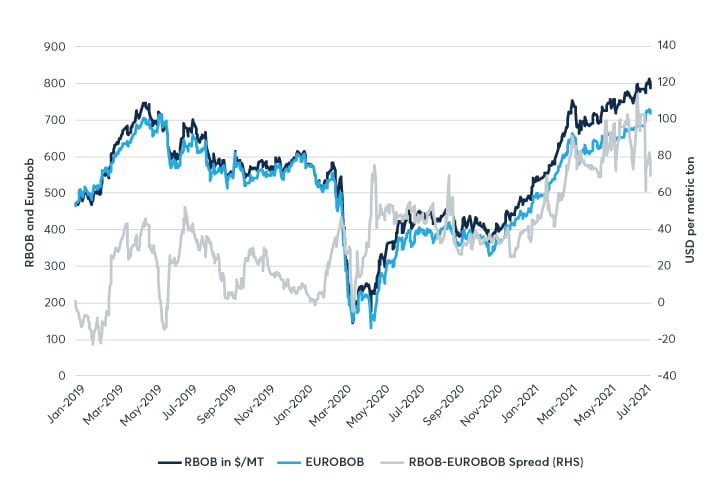

A more compatible market with the United States could become a major factor in influencing trading decisions about the role that RBOB futures may play in the global gasoline trade.

The correlation between European Eurobob gasoline blendstock and the US blendstock market was around 94% over the January to April 2021 period, broadly in line with the levels reached in 2020. Given the relatively high correlation between both markets, refiners and traders can hedge the underlying price in one market with the other whilst relying on the deep liquidity afforded to them by the RBOB futures and will drive additional capital efficiencies in the market by trading and clearing the spread on a single exchange.

Chart 2: European gasoline prices track RBOB increasingly closely

{kind=link}

Source: CME Group data

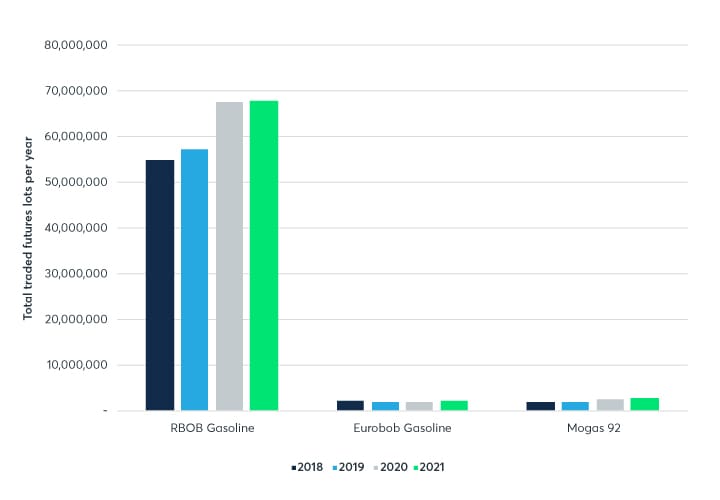

RBOB Gasoline is the largest gasoline futures market by volume traded, according to the latest CME Group data. For full year 2020, RBOB Gasoline futures traded just under 68 million contracts which represented around 93% of total gasoline derivatives activity. This level was broadly unchanged in January to June 2021.

Chart 3: RBOB Gasoline trumps other international benchmarks by volume

{kind=link}

Source: Exchange data

Ethanol – a pathway to reduce greenhouse gas emissions

European ethanol delivers 71% greenhouse gas emissions savings compared to fossil fuel-based gasoline. Any move to a higher ethanol content in the gasoline would have a positive climate impact on the road transport sector fuels as it would displace a greater quantity of fossil fuels in the blendstock mix.

The percentage of blended ethanol is expected to rise, especially in Europe. The European renewable fuels association ePure2 believes that ethanol produced sustainably from crops and agricultural wastes and residues could provide a decarbonised alternative. In some European countries, there is already a mix of 5% and 10% ethanol blended gasoline available and more countries look set to follow a similar path by either introducing it for the first time into the supply chain or further increasing the availability of higher ethanol blended fuels alongside existing gasoline blends.

Table 1: European countries transition more gasoline to E10

| Country | Introduced 10% (E10) gasoline or higher |

|

Europe* [text-align: center] |

|

| Bulgaria | E10 available since 2020 |

| Romania | E10 available since 2020 |

| The Netherlands | Rolled out E10 in October 2019 |

| Denmark | Been available since before 2019 |

| Hungary | E10 available since 2020 |

| Lithuania | E10 available since 2020 |

| Slovakia | E10 available since 2020 |

| Belgium | Been available since before 2019 |

| Finland | Been available since before 2019 |

| Luxembourg | Been available since before 2019 |

| France | Been available since before 2019 |

| Estonia | Been available since before 2019 |

| Germany | Been available since before 2019 |

| Sweden | Will transition to E10 August 2021 |

| UK | Will transition to E10 September 2021 |

| Czech Republic | Introduction of E10 expected in 2021 |

|

Asia-Pacific [text-align: center] |

|

| Indonesia | E10 is permitted but not fully implemented. |

| Thailand | E10 available since 2013 |

| Japan | Available since 2012 |

| Philippines | E10 been permitted since 2011 |

| India | Planned E10 introduction in 2022 |

| Australia | Mandates vary by state for bioethanol or biodiesel use. New South Wales and Queensland consumes the most ethanol blended fuel by mandate. |

| China | E10 rollout halted nationally, partial rollout only |

|

America's [text-align: center] |

|

| USA | Been available since the late 1970s |

| Argentina | Available since 2014 with higher blends available |

| Brazil | Higher ethanol blends are available |

*Supply does vary between countries – Belgium, Luxembourg, Finland, France, Estonia and Germany only partially switched to E10.

Source: ePure3 and Argus Media data

Since 2009, there are 14 EU countries that have already adopted E10 gasoline into the local gasoline supply. Some countries have switched completely to E10 while others have chosen to offer it alongside the existing E5 market. Germany was one of the first countries to adopt E10 but its take up has been slower, in part due to some compatibility issues with older vehicles although this is changing as the country looks to achieve higher greenhouse gas savings afforded by the higher ethanol based fuels.

Sweden and the United Kingdom will be switching the gasoline supply to E10 from August and September 2021, respectively. The UK government is confident of the benefits of higher ethanol blends following the announcement of 10% blended gasoline from September 2021. The government stated that the move would reduce carbon emissions by 750,000 tonnes per year or the equivalent of removing 350,000 cars off the road.4

In Asia, certain countries have taken significant steps in the transition to cleaner fuels. Thailand has been a proponent of change in the promotion of alternative transport fuel use. E-10 has been available since 2013 and, under the New Alternative Energy Development Plan approved in 2019, the country will phase out E10 and E85 in the long term with the sale of E-20. The Japanese government introduced E10 and ETBE 22 for vehicle use. The country has capped its blend rate at 3% with the exception for vehicles that specifically utilize E10. China mandated the use of E10 in their vehicles as part of their efforts to combat air pollution in September 2017. The government has since eased its original mandate to use E10 by 2020. This was partly attributed to unfavourable market conditions of ethanol.

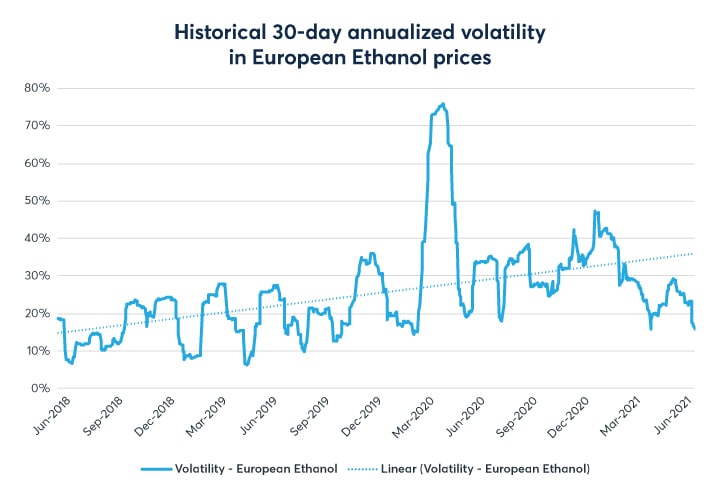

Volatility in European ethanol has steadily increased, partly reflecting growing EU demand as a blending component for gasoline. The 30-day historical annualized volatility data was 32% on average during the first quarter of 2021 compared with just 25% 12 months earlier. Increasing volatility tends to see higher hedging volumes and companies look to mitigate against price swings in the underlying market. The Netherlands switched to E10 gasoline in October 2019.

Volumes month to date (June 2021) reached 3,600 lots or 360,000 cubic metres of ethanol; this was lower than the same period 12 months earlier but the volumes during this period were boosted by the news that some countries in northwest Europe (Belgium and the Netherlands) had increased the overall usage of ethanol by increasing the blend from 5% to 10% in gasoline.

Chart 4: European Ethanol volatility prompts hedging demand

{kind=link}

Source: S&P Global Platts, CME Group data

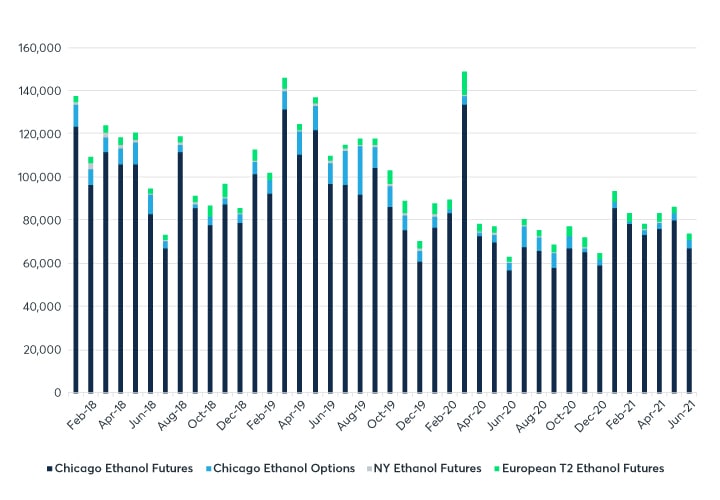

CME Group data shows that global ethanol futures remain robust, with a total of 82,000 lots (or 2.6 million barrels per day) traded per month in the January to June 2021 period, broadly flat with full year 2020 volumes. In the European markets, where the transition to higher ethanol blends is already underway, total traded volumes in 2020 were 4,082 lots or 408,000 cubic metres (or 85,000 barrels per day), up around 10% of the volumes seen in 2019. Year-to-date June 2021 volumes were 3,580 lots or 358,000 cubic metres (or 75,000 barrels per day).

Chart 5: Global ethanol futures and options remain robust

{kind=link}

Source: CME Group data, S&P Global Platts and Argus Media

US RBOB gasoline - a growing global futures benchmark

In the United States, there are two main formulations for gasoline: Reformulated Gasoline (RFG) and Conventional Gasoline (“CG”), as required by a complex network of federal and state regulations. RFG is produced by blending 10% fuel ethanol with Reformulated gasoline blendstock, called RBOB, which is the grade of gasoline deliverable against the NYMEX RBOB gasoline futures contract. Similarly, Conventional Gasoline is made with a blend of 10% fuel ethanol and Conventional Gasoline blendstock, which is referred to as CBOB. Over 98% of US gasoline contains ethanol (E10) which is used to oxygenate the fuel to reduce air pollution.5 Reformulated gasoline remains the most significant representing over 90% of the gasoline derivatives volumes traded globally (see chart 3).

The Renewable Fuels Standard program is the federal policy that mandates a certain volume of renewable fuel to reduce or replace the amount of petroleum that is found in transportation fuel. The US Environmental Protection Agency (“EPA”) administers the Clean Air Act (“CAA”) requirements, and various state agencies regulate their own specific air rules. Under the CAA, the urban areas with the highest levels of smog pollution are required to use clean-burning Reformulated gasoline blended with 10% ethanol. These urban areas include the entire Northeastern United States, California, Chicago, Atlanta, and Houston metropolitan areas. According to the EPA, it is estimated that 75 million people breathe cleaner air due to RFG.6

With the United States re-joining the Paris Agreement, the Biden Administration has made climate change a priority in efforts to move the country toward achieving net zero emissions from the power sectors by 2035 and economy-wide by no later than 2050. As a result, this could give rise to enhanced policies that will accelerate the decarbonization of the nation’s transportation fuels.

The EU sets out its grand plan to reduce emissions

Tighter revisions to the existing European Renewable Directive (RED II), were proposed in July 20217 calling for higher blends of biofuels from renewable sources to reduce the total volume of fossil fuels that are consumed within the transport sector. Around 70% of global greenhouse gas emissions are generated by the energy industry, with around 25% of that coming from the transportation sector. Overall Greenhouse Gas emission reduction targets are proposed to increase 40% to 55% by 2030 under the Fit for 55 legislation announced by the EU in mid-July 2021. To further support the green agenda for road transport, a new target for reducing greenhouse gas intensity of transport fuels by 13% by 2030 was proposed. This equates to an energy-based target of 28%, an increase of 14% points from the previous 2030 target revision. The EU proposed an additional sub-target of 2.2% (single counted) for advanced biofuels or 4.4% (with fuels such as used cooking oil which are double counted). Overall, the renewable share in gross final energy consumption looks set to rise to between 38% and 40% which will boost the mandates of each EU country in 2021 and beyond.

Low carbon gasoline solutions

Bosch, Shell and Volkswagen have developed Blue gasoline, a low carbon gasoline which uses 33% renewables, made up of biomass-based naphtha or ethanol certified by the International Sustainability and Carbon Certification (ISCC) system.8 This is an important step in the environmental and sustainability roadmap of gasoline markets. Further developments around products like E-gasoline, which is generated from renewable electricity could also form part of the supply mix. It is likely that these types of fuels could provide a significant boost to net zero carbon emissions. One of the key challenges will be the availability of large-scale hydrogen (and green power) but many countries are looking to address this over the coming years.

Higher ethanol blends into the gasoline mix is widely seen as one possible solution to reduce the global carbon impact from fossil fuels. A broader adoption of blends in gasoline, could help support the drive to reduce the carbon footprint from road transport fuels and combined with other initiatives, keep the drive to net zero carbon emissions by 2050 on track.

Any further transition to E10 gasoline is likely to see global gasoline markets converge more closely and this may enhance the futures benchmark role that RBOB gasoline plays on the international stage. At the same time, companies will be looking to increase purchases of ethanol to meet the more stringent blending requirements thereby boosting demand for risk management products in this market.

As volatility continues to be paramount in risk management in the gasoline markets, RBOB gasoline looks set to play a larger role globally as global gasoline specifications continue to converge more closely together and align more towards that of the blendstock markets in the United States.

References

- IEA Report – Transport 2020 https://www.iea.org/topics/transport

- ePure – https://www.epure.org/wp-content/uploads/2020/11/200612-def-pr-epure-fuelling-europe-future-leaflet.pdf

- ePure – E10 gasoline by EU member country – https://www.epure.org/about-ethanol/fuel-market/fuel-blends/

- UK Government introduces E10 gasoline – September 2021 https://www.gov.uk/government/news/fuelling-a-greener-future-e10-petrol-set-for-september-2021-launch

- https://www.cmegroup.com/fuels/ethanol_fuel_basics.html

- https://www.epa.gov/gasoline-standards/reformulated-gasoline

- Tighter revisions to RED II (Proposals) July 2021 https://ec.europa.eu/info/sites/default/files/amendment-renewable-energy-directive-2030-climate-target-with-annexes_en.pdf

- ESG today – Low Carbon gasoline launched in Europe https://www.esgtoday.com/bosch-shell-and-volkswagen-launch-low-carbon-gasoline/