{kind=link}

Primary Aluminium Production in China and the Covid-19 Effect

In March, China’s Changjiang spot aluminium prices fell by 15%, plunging most Chinese smelters into losses and forcing some capacity out of the market. Since April, however, prices have rebounded strongly, bringing an estimated 98% of smelters back into profitability and closing the gate on any further curtailments. The combination of a rapid price rebound, minimal capacity curtailments, and a weaker demand outlook has created the perfect conditions for over-supply and for prices to come under renewed pressure.

Under price pressure, the primary aluminium industry behaves differently from other base metals industries because the fully-continuous electrolytic process makes capacity closures of any size difficult and expensive undertakings. Most owners will do whatever they can to avoid it.

History tells us aluminium smelters can withstand extended periods of low prices because their major cost inputs, alumina and electricity, can be forced lower when primary aluminium prices come under pressure. Prohibitively high closure costs can also provide plenty of incentive to continue operating at a loss. However, over longer periods, fundamental economics ultimately force high-cost capacity out of the market.

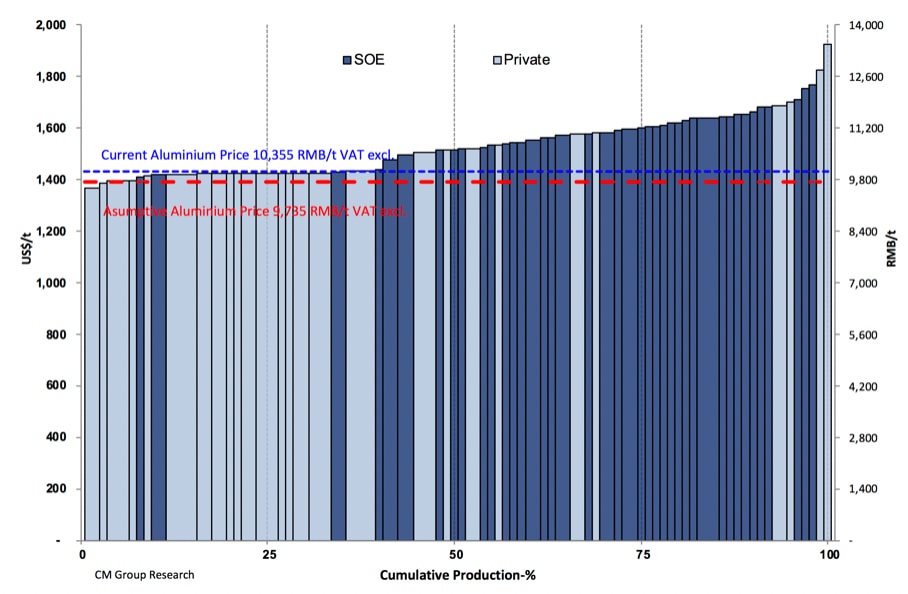

China’s primary aluminium sector, which currently produces around 60% of the world’s metal and is worth billions of RMB to the Chinese economy, is structured differently. Around 43% (18.6 mtpy) is controlled by privately-owned producers who are integrated either upstream (alumina) or downstream (finished products), or both, and all with “captive” electricity generating assets. Essentially, this means their smelting operations are less exposed to aluminium price volatility.

A further 32% (13.5 mtpy) of China’s smelting base is controlled by state-owned entities (SOEs) either with captive electricity sources or with substantial vertical integration who, in the past, have been far less inclined to shutter capacity, despite prices falling below production costs for extended periods.

The restcomprise private smelters with a handful of SOEs buying electricity from the state grid and who have little or no vertical integration. They represent around 25% (11 mtpy) of total capacity. Typically, these smelters operate under more flexible models; they respond quickly to changes in market dynamics, more so than other smelters, by swinging capacity off and back on at low cost.

Using this framework, CM’s bottom-up sector analysis monitors every smelter falling into this category. We’ve identified 18 in total, some of which contributed to the mothballing of 766kt/yr capacity due to falling primary Al prices during March and April.

Figure 1 – Cash operating cost curve for China’s primary aluminium smelters, Q1 2020 Source: CM Group

{kind=link}

Monitoring operations at these key smelters, as well as their alumina purchasing activities, can provide a penetrating insight into the likelihood of closures and, by extension, the trajectory of China’s supply demand balance. These smelters need to be watched closely if the true trajectory of the industry is to be forecast.

A key risk to our view is the potential for China to enter a prolonged period of low prices. Primary aluminium prices at or below RMB9,500/t (VAT incl.), i.e. RMB8,400/t VAT excl., over a period of at least six months would expose a second tier of around 22 smelters, representing 3.65 million tonnes per year of higher-cost capacity, to potential closure. This second-tier of smelters, spread throughout the country, comprises higher-cost independents, plus higher cost SOEs running older andless efficient smelting technology.

Assuming the worst of the COVID-19 pandemic has now passed in China, we expect its highly responsive primary aluminium producers to restart quickly, leaving little room for prices to rise above industry cost curve fundamentals. Already we’ve seen around 80ktpy of recently mothballed capacity re-enter the market, and around 125 ktpy of potentially delayed new capacity back on the agenda for commissioning. We continue to monitor these key smelters for guidance.

References

{kind=link}

https://www.cmegroup.com/content/dam/cmegroup/images/common/header/logo-cme-group.png

{kind=link}