{kind=link}

Magnesium – Abundant and Cheap or a Strategic Blindspot?

It’s tempting to think of magnesium as a less-famous cousin to the world’s premier structural light metal – aluminium. After all, the world’s entire primary magnesium supply could be produced in one decent-sized aluminium smelter, around 1 million tonnes. Compare this with the 65 million tonnes of primary aluminium produced globally each year.

Dig a little deeper into the magnesium industry and what is revealed are some concerning structural supply issues that should ring alarm bells not just in governments, but in the myriad industries dependent on an uninterrupted supply of semi-fabricated products from Big Cousin Aluminium. That includes the world’s automotive and construction sectors, as well as a raft of smaller industries, all reliant on aluminium alloy parts and componentry.

The average aluminium can contain around 1.5% magnesium (by weight), which might not seem like much because, well, it isn’t. However, without the addition of this small, critical, amount of magnesium, the physical and mechanical properties required of the can couldn’t be met using aluminium. The aluminium can as we know it wouldn’t exist. Neither, for that matter, would aluminium road wheels, extruded window frames, nor the wings of a modern Airbus airliner.

In fact, around 75% of all finished products made from primary aluminium wouldn’t be suitable for their applications because they all contain magnesium as a critical alloying element, for which there is no substitute.

If the magnesium tap turns off, where does it leave the world’s aluminium industry?

Aluminium alloying is the single largest market sector for primary magnesium, closely followed by die-casting, then steel desulphurisation at a distant third. Die casting and desulphurisation both have substitutes, meaning both are sensitive to fluctuations in magnesium prices.

The die-casting sector, particularly automotive, is worth a closer look; around 20 years ago three large, high profile primary magnesium projects burst onto the international stage, two in Australia, one in Canada. All three had secured large offtake agreements from automotive producers whose bullish forecasts had underwritten their future. Magnesium was to become the long-term, high-volume die-casting material of choice for the automotive sector. At only two-thirds the density of aluminium and comparatively easy to die cast, it was set to replace aluminium, steel and plastic in a range of high-volume applications.

A decade, and around US $2 billion later, all three projects had failed, auto producers had walked away from their offtake agreements, and the world’s magnesium supply-base had gravitated to inland China, where a simple, low capital cost, but highly labour and energy intensive process known as the Pidgeon Process, had taken hold.

In parallel, several ROW magnesium producers had shut up shop, in anticipation of new high-volume low-cost producers and the emerging threat from Chinese material. And it was the world’s big aluminium producers of the day; Alcan, Alcoa, Norsk Hydro, and Pechiney, who were doing so, having owned and operated their own magnesium production facilities for decades.

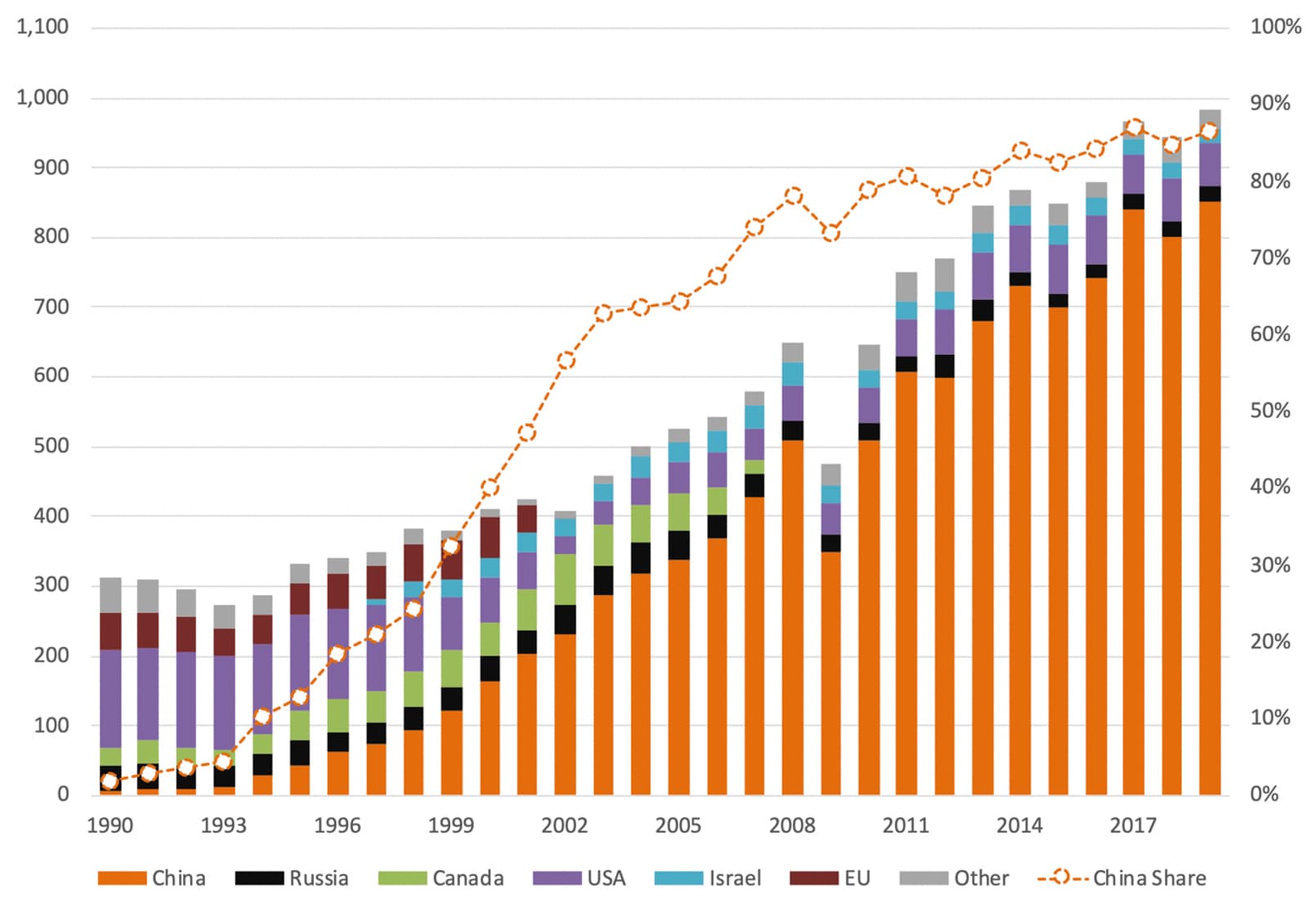

Today, China’s supply base accounts for over 80% of world primary magnesium production and, with Russia included, this figure increases to around 87%.

Figure 1 Global Primary Magnesium Production by Country, 1990-2019 (kt)

{kind=link}

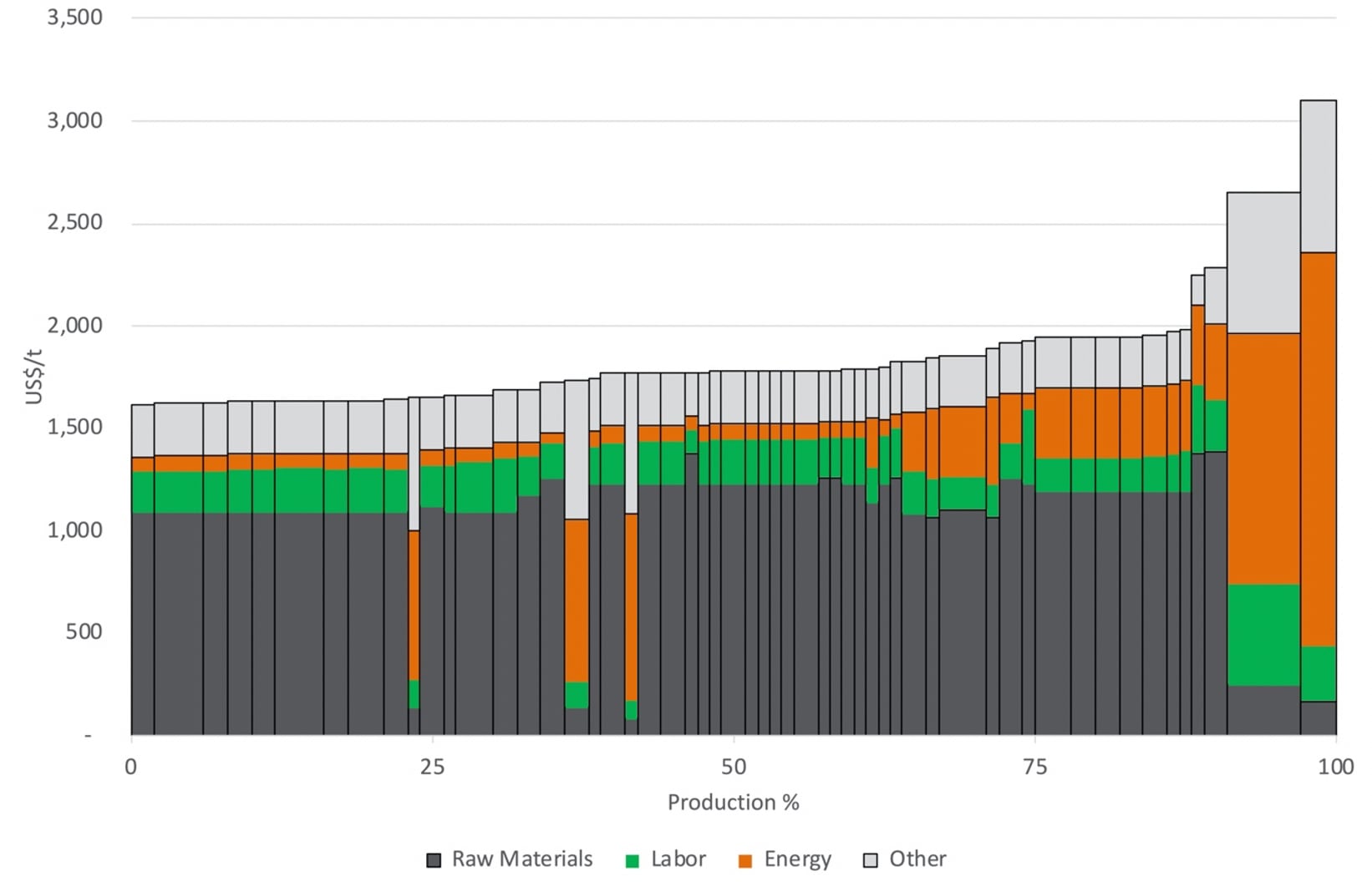

Chinese magnesium producers achieve a low cost because they take advantage of waste heat energy associated with coal gas production to drive the process, which they acquire virtually free by co-locating with coking ovens. The disadvantage is that the Pidgeon Process consumes around 1 tonne of ferro-silicon (FeSi) for every tonne of magnesium produced, meaning magnesium costs are strongly correlated with Fe-Si prices and, by association, steel prices.

Figure 2 Primary Magnesium Global Cash Cost Curve (2019, US$/t)

{kind=link}

So what might happen if Chinese costs are forced higher or supply becomes constrained? The world caught a glimpse leading up to the Beijing Olympic Games in 2008, when the country forced much of its magnesium supply base to close and prices in the EU more than doubled as a result. The kneejerk response from the world’s big aluminium producers was to send procurement department heads to China on fact-finding missions. The Chinese soon got wind of this and pushed prices even higher. By the time the Olympics were under way, magnesium prices had almost tripled.

What might be different next time? The short answer is nothing; no new greenfield primary magnesium plants have been built and operated competitively outside China for the past 15 years. Many of the world’s primary aluminium producers, therefore, remain critically exposed to a magnesium supply disruption, as do the thousands of downstream fabricators they supply.

It would take at least 18 months to establish a large, primary magnesium supply base to replace what is currently exported from China. Should the world be building more primary magnesium capacity now? Perhaps so, although some regions are more exposed than others. The US has one large primary Mg producer, USMag LLC, and its market is protected from Chinese primary Mg imports by an ad valorum anti-dumping duty set at 141.49%1. The EU on the other hand, has no anti-dumping duties and no domestic supply, so the market would likely be more sensitive. Any potential knock-on effect would become evident by monitoring CME’s US, Japan, and EU aluminium premium futures contracts, which may see a divergence emerge as markets respond according to their relative exposures.

In the interim, we believe global magnesium flows can be monitored closely and modelled, sensitised to the aluminium cost curves and downstream products to measure the risk to your aluminium exposure.