{kind=link}

Kansas City vs. Chicago Wheat Spread: A Tale of Two Markets

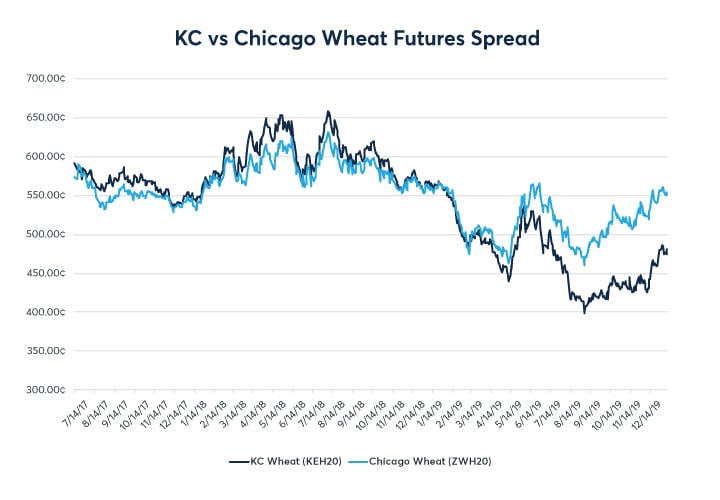

Figure 1: Kansas City vs Chicago Wheat Futures Spread

{kind=link}

Source: CME Group

Starting in 2019 and going into 2020, The Kansas City Wheat futures (KE) contract has been trading at an unusual discount relative to Chicago Wheat futures (ZW). With the Mar 2020 KE contract trading at a 75 cent per bushel discount and the Dec 2020 KE contract trading at a 65 cent per bushel discount, the market’s current expectations imply continued tightness in the Chicago Wheat market compared to KC throughout 2020.

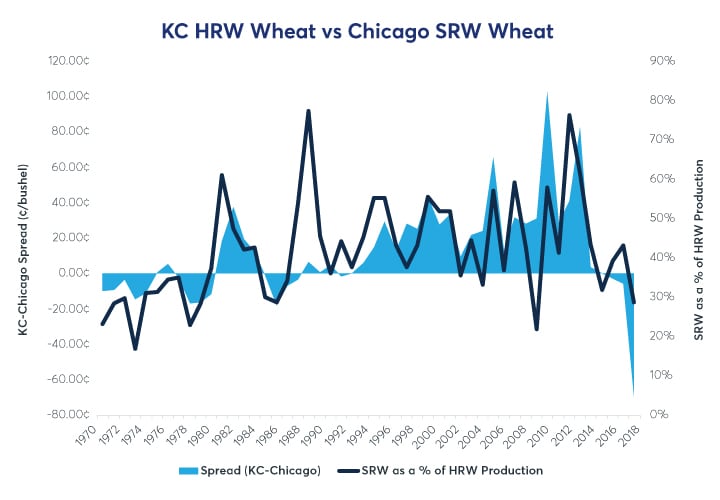

The chart below shows that the Kansas City premium or discount versus ZW is closely related to production of Hard Red Winter wheat (HRW), the underlying commodity for the KE contract, relative to Soft Red Winter wheat (SRW) production, the underlying commodity of Chicago Wheat. 2017, 2018 and 2019 all saw SRW production historically small relative to HRW production resulting in tight SRW availability and stocks and record SRW cash premiums versus HRW (HRW cash discounts versus SRW).

Figure 2: KC-Chicago Futures Spread Relative to SRW % of HRW Production

{kind=link}

Source: USDA and CME Group

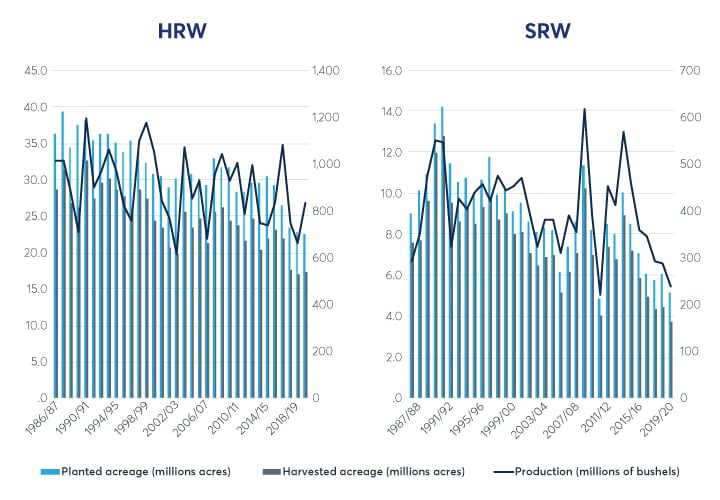

Looking at Figure 3, SRW production has hit near record lows after experiencing year-over-year declines in planted and harvested acreage since the 2013/14 marketing year. Continued and sustained poor weather conditions in SRW’s predominant growing region of Illinois, Indiana, Ohio, and Michigan have contributed to significant supply side concerns for the crop.[1]

Figure 3: US Soft Red Winter Wheat vs US Hard Red Winter Wheat Production, Planted Acreage, and Harvested Acreage

{kind=link}

Source: USDA

Representing the third largest wheat variety in the U.S., SRW wheat is mainly grown in 25 states east of the Mississippi River and is commonly used for producing flat breads, cakes, cookies, snack foods, and pastries. SRW’s domestic use/consumption has accounted for an average of 48 percent of total SRW supply since 1985, showing strong domestic demand for the grain. Comparatively, HRW’s domestic use/consumption represents on average only 40 percent of total HRW supply over the same duration.[2] In export markets, SRW is typically less sought relative to HRW due to its lower protein content relative to other varietals.

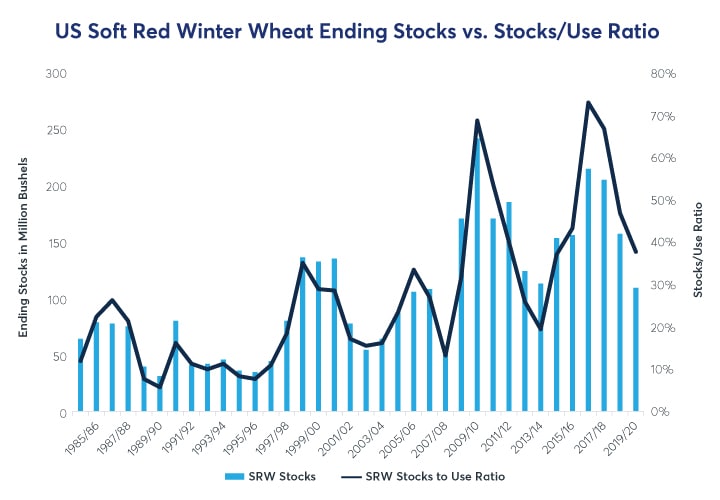

Figure 4: US Soft Red Winter Wheat Ending Stocks vs. Stocks to Use Ratio

{kind=link}

Source: USDA WASDE

Looking at the Stocks to Use Ratio, an indication of the level of carryover stocks for a given commodity as a percentage of total demand or use, USDA data shows an SRW ratio equal to 38 percent for the 2019/20 marketing year, representing a 4-year low for the crop. Characteristically, a lower stocks to use ratio is indicative of lower supply relative to demand (higher prices), while a higher stocks to use ratio indicates a higher or abundant supply relative to demand (lower prices).

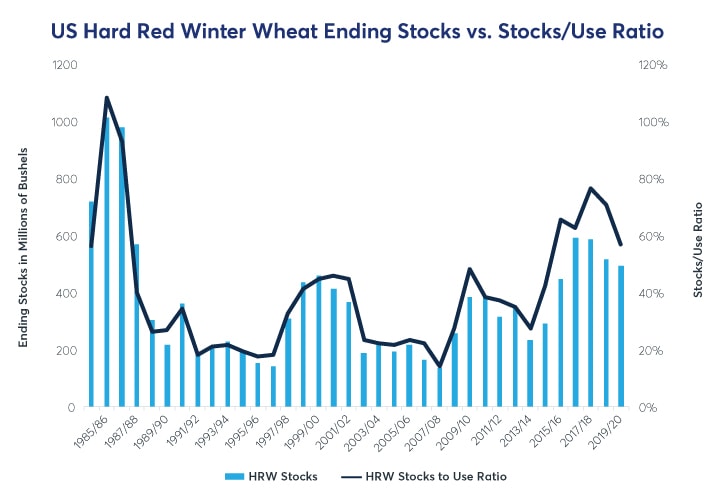

Figure 5: US Hard Red Winter Wheat Ending Stocks vs. Stock to Use Ratio

{kind=link}

Source: USDA WASDE

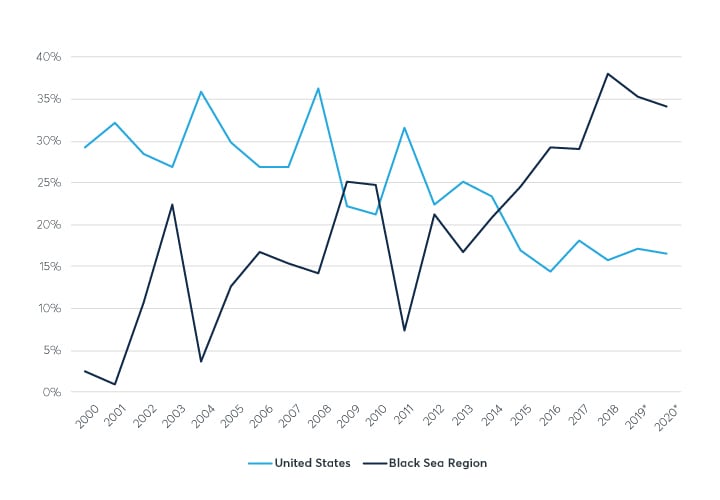

USDA data shows HRW’s 2019/20 stocks to use ratio equal to 58 percent as seen in Figure 5. In other words, relative to SRW, the higher ratio indicates there is less demand for and more supply of HRW. Representing the largest U.S. wheat variety, HRW is the primary ingredient in the production of bread and is highly sought after in world wheat export markets due to its versatility of use and high protein content. Since 1985, HRW has averaged almost 40 percent of all U.S. wheat exports while SRW has averaged only 15 percent of total U.S. wheat exports over the same duration. With HRW’s high dependency on export marketing channels, the shift in global wheat export markets away from the U.S. and towards Europe and the Black Sea Region (BSR) has had a marked impact on global demand for the US HRW crop and the price at which it can be exported. Once the dominating presence, the U.S.’s wheat export market share has decreased significantly from 29 to 15 percent since the trade year 2000 as seen from the Figure 6.

Figure 6. Export Sales Market Share U.S. vs Black Sea Region (Ukraine and Russia)

{kind=link}

Source: USDA

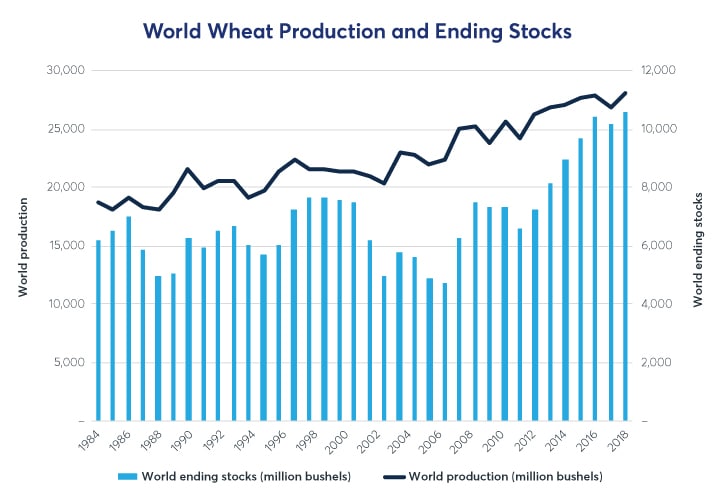

According to USDA, today’s world wheat markets are flush with record world ending stocks driven by massive growth in production and exports from the BSR, limiting the global competitiveness of US wheat as seen in Figure 7. This, combined with the domestic supply side concerns of SRW wheat relative to demand, and the competitive pricing of Black Sea Wheat, could carry the ZW-KE wheat spread well into the 2020 marketing year, as shown by the current Dec 2020 futures price spread.

Figure 7: World Wheat Production and Ending Stocks

{kind=link}

Source: USDA