{kind=link}

Hedging with the CME Feeder Cattle Index White Paper

Hedging with the CME Feeder Cattle Index

What is the CME Feeder Cattle Index?

The CME Feeder Cattle Index (Index) is intended to serve as a benchmark for the price of cattle being placed on feed at the feedlot. Or as defined by the USDA in the monthly “Cattle on Feed” report:

“Placements are steers and heifers put into a feedlot, fed a ration which will produce a carcass that will grade select or better, and are intended for the slaughter market.”

The Feeder Cattle Index broadly represents the price of cattle purchased by feedlots that will likely grade select or higher, be placed on feed for an extended period, and finally marketed

to a packer for slaughter. The Index underlies the CME Feeder Cattle futures contract. The data used by CME to calculate the Index facilitates convergence — the tendency of the cash and futures prices to come together as the futures contract nears expiration — to the weighted average price of feeder cattle sold across 12 major feeder cattle-producing states.

The data used to calculate the Index is collected and reported by the USDA’s Agriculture Marketing Service and is publicly available. The states included in the Index are Colorado,

Iowa, Kansas, Missouri, Montana, Nebraska, New Mexico, North Dakota, Oklahoma, South Dakota, Texas and Wyoming. By defining the area and type of cattle used for calculating the Index, CME provides a reliable and publicly available benchmark for market participants to reference when making risk management decisions. USDA-AMS summaries and sales reports are available on the USDA webpage: ams.usda.gov/market-news/livestock-poultry-grain#Cattle

{kind=link}

CME Feeder Cattle Index – 12 State Region1

How is the CME Feeder Cattle Index Constructed?

The Index is based upon transactions from the USDA-AMS Feeder Cattle Reports, and the cattle included in the Index must meet the following criteria:

Weight and Frame Score Categories

- 700 to 899-pound Medium and Large Frame #1 feeder steers

- 700 to 899-pound Medium and Large Frame #1-2 feeder steers

All feeder cattle auction, direct trade, video sale and Internet sale transactions within the 12-state region for which the number of head, weighted average price and weighted average weight are reported are used in the Index calculation.

All direct trade reports are considered Friday transactions. Reports that are designated as “preliminary” are not included. Cattle identified in the report as being fancy, thin, fleshy, gaunt or full; having predominantly dairy, exotic or Brahma breeding; are currently excluded2. Transactions for cattle that are reported as having an origin outside of the United States are also excluded. Direct trade, video sale and Internet sales transactions must be quoted on an FOB basis, a 3% standing shrink or equivalent and with pickup within 14 days.

The Index is a seven-day weighted average and is defined as the total dollars sold during the seven-day period divided by the total pounds of feeder steers sold during the same seven- day period. Every pound of feeder steer sold during the seven- day period has the same impact on the final price.

Current and historical Index data can be found on the CME Group website here: cmegroup.com/market-data/reports/ commodity-index-prices.html

Why Not Physical Delivery?

Benchmark agricultural futures contracts that have maintained the physical delivery system through the years have done so because of the underlying market’s structure. Physical delivery is effective when a market has large, concentrated supply and/or demand centers. The feeder cattle market has evolved geographically over the years so that concentrated supply/demand hubs no longer represent this market. The old CME Feeder Cattle futures contract was physically delivered and had two delivery points: Oklahoma City, OK and Amarillo, TX. These locations stationed deliveries in areas with concentrations of large-scale feedlots and in relative markets that were similarly priced. This delivery system was limited by the fact that producers of feeder cattle are relatively small and geographically dispersed, leading to deliverable supply and freight issues.

The old contract required a feeder cattle owner in Iowa to haul his feeders to Oklahoma City to deliver against the contract. Because of the high cost to haul cattle that far, the basis would need to be strongly negative for it to be economical. If more delivery points were added, long/buy-side market participants would risk buying cattle that would be delivered to a location that is neither close to their operation nor has other feedlots nearby, further increasing the cost of freight.

In short, the feeder cattle market became too decentralized to support an efficient deliverable futures contract settlement process. Leading up to the transition to cash settlement, Feeder Cattle futures trading volume declined by nearly 70% from its peak (at the time) in 1979 of roughly 1 million contracts to only about 316,000 contracts by 1984. These factors led the Exchange to pursue a cash-settled contract that began with the September 1986 contract. The cash-settled Feeder Cattle futures contract provides effective risk management opportunities for market participants regardless of where they are located.

Hedge Effectiveness

Hedge effectiveness in the futures market is a function of the correlation between futures prices and cash prices. In other words, if cash market prices go up, futures price are expected to go up as well. This means cash prices are not expected to be the same as futures prices but the basis (the difference between cash and futures prices) at any given location in the country should be stable.

Hedge effectiveness is represented statistically by regressing cash prices on futures prices3. Hedge effectiveness measures the percent reduction in the variability of daily price changes between an unhedged versus hedged position. For example, a hedge effectiveness of 99 percent means that, on average, a hedged position faces 99 percent less daily price variability compared to an unhedged position.

Daily feeder cattle cash prices from Texas, Kansas and Nebraska were collected and regressed on daily Feeder Cattle futures prices, with the resulting hedge effectiveness percentages.

Exhibit 1. Hedge Effectiveness 2013-2017

| Texas | Kansas | Nebraska | |

| Hedge Effectiveness (R-squared4) | 99.8553% | 99.9212% | 99.8385% |

These results indicate that the CME Feeder Cattle futures contract is an extremely effective hedge for daily price movements in all regions, meaning that the futures market is highly correlated with the cash market. It is also worth noting that the hedge effectiveness is similar across all three regions, suggesting futures market prices move with cash prices regardless of location. These results show that a hedger can be confident in using Feeder Cattle futures to protect against adverse price movements.

Basis Difference by Region

The territory covered by the CME Feeder Cattle Index ranges from Texas in the South to Montana in the North; and from Colorado in the West to Iowa in the East. Because of the expansive area covered by the 12-state area, regional basis differences are one of the most important factors that a hedger needs to be aware of. This paper investigates the differences in basis across three cattle feeding regions: Texas, Kansas, and Nebraska.

For example, one can expect the cash price of feeder cattle in Nebraska to be higher than the futures price most of the time. Conversely, the cash price in Texas can be expected to be lower than the futures price most of the time. Average basis for the three regions are shown in the table below over the five- year period from 2013-2017.

Exhibit 2. Regional Average Annual Basis

| Regions | Mean Basis |

| Texas | -$4.9487/cwt. |

| Kansas | -$0.7687/cwt. |

| Nebraska | +$7.5884/cwt. |

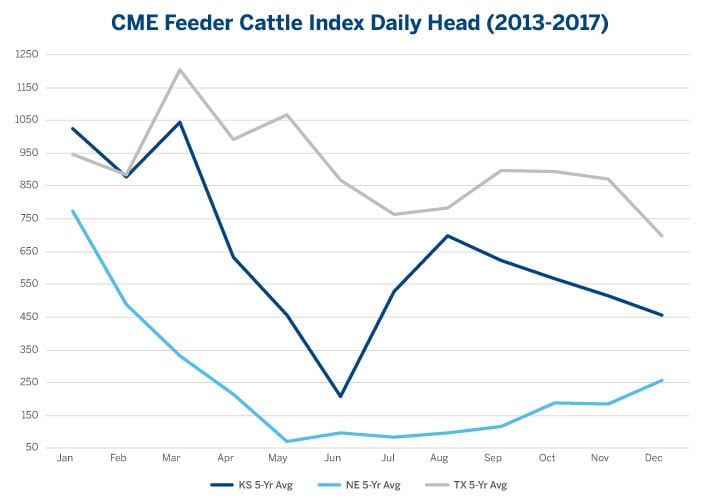

Many factors can be attributed to these differences in regional basis values. In addition to weather and the seasonal cycle of production, there are certain months during the year where Kansas and Nebraska do not contribute nearly as many head to the Index as Texas does. As seen in Exhibit 3, the five-year average daily head count in Nebraska is always below the Kansas and Texas counts.

Exhibit 3. CME Feeder Cattle Avg. Index Daily Head

{kind=link}

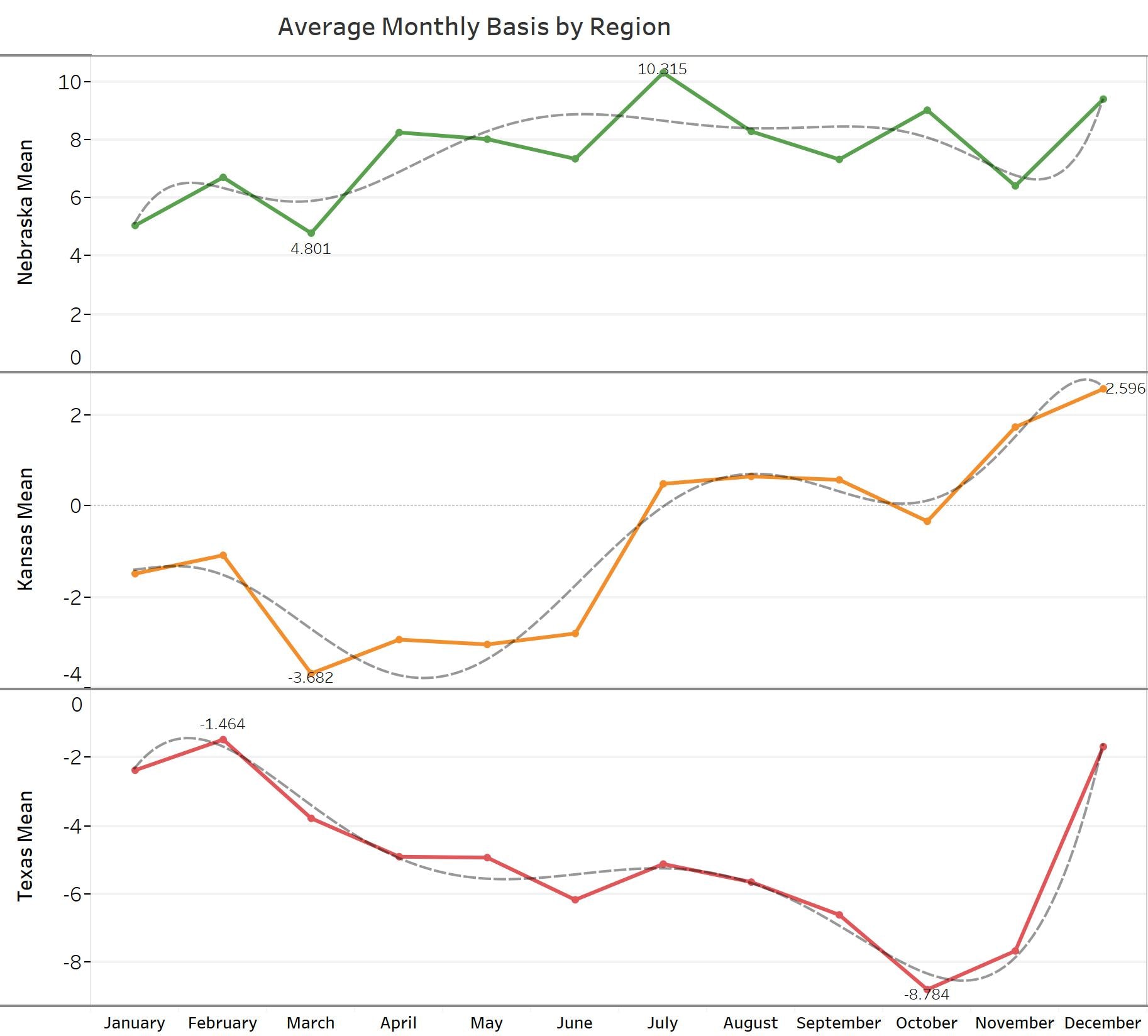

Seasonal Basis Difference per Region

Knowing which month(s) of the year the basis is likely to be strong or weak is beneficial to hedgers because it enables them to plan when to buy or sell futures contracts.

When all three regions are compared and analyzed statistically, some notable differences become apparent.

Exhibit 4. Regional Basis (CME & USDA-AMS)

{kind=link}

In Texas, October has the widest (weakest) basis, while December and February are the narrowest (strongest). Kansas had notable differences in basis that showed basis at its widest in March, April and May. Nebraska did not show any significant difference in basis over the course of a year. This means that the rate of change in the local cash price is not significantly different to the rate of change in the futures price.

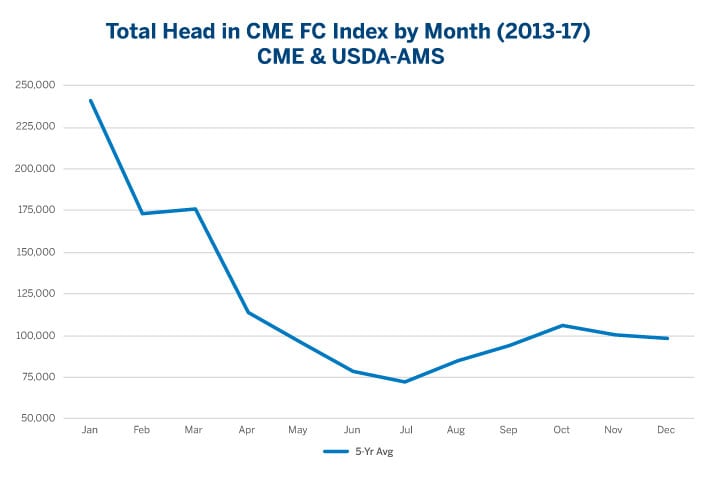

Therefore, there are significant basis differences across all three regions that vary by month. Factors driving these differences include local supply and demand for feeder cattle, weather conditions, access to feed and the cost of freight just to name a few. Additionally, the number of head included in the calculation of the Index ebbs and flows. For example, the total number of head included in the Feeder Cattle Index peaks in January and is at its lowest in July.

Exhibit 5. Average Total Head

{kind=link}

It is important for a hedger to consider the historical basis relationships that a local cash price has to futures throughout the year to make the best decisions on how and when to manage risk.

Hedge Examples

As discussed at the beginning of this paper, the CME Feeder Cattle Index price is a weighted average price that reflects the prices paid in the cash market across the 12-state region. Expiring CME Feeder Cattle futures contracts settle to the Index price average during the week preceding expiration.

On all days prior to expiration, futures reflect the price that the market expects the Index to be when the futures contract expires. For example, the settlement price for the August 2018 futures contract (“FCQ18”) on July 13, 2018 was $150.725/cwt.

That means the market believes that the Index price on August 31, 2018 (final settlement date of FCQ18) will be $150.725 based on all available information on July 13. Knowing how to interpret futures, cash and Index prices is critical to making decisions on how and when to manage risk. This last section will look at some real examples of how to hedge using Feeder Cattle futures.

From the regression results above, a cattle producer can expect to reduce price risk by over 99 percent by hedging feeder cattle using the CME Feeder Cattle futures contract. For the first example, consider a stocker operation in Texas.

Example 1: Stocker Operator ABC Cattle Co. (ABC) in Texas purchases 400 yearling steers averaging 400 pounds per steer in March that are put on pasture. Once the steers have reached 800 pounds, ABC intends to sell them at a feeder cattle auction in January. One contract of CME Feeder Cattle is 50,000 pounds, or approximately 62.5 head of 800-pound steers. Therefore, ABC’s purchase is equal to 6.4 contracts of CME Feeder Cattle futures, and these cattle are hedged by selling 6 contracts of the January (JAN) contract month in March, at $145.425. Exhibit 6 shows the regional basis values by month.

Exhibit 6. Basis to Futures by Region

| Month | Texas | Kansas | Nebraska |

| January | -$2.36 | -$1.48 | $5.07 |

| February | -$1.46 | -$1.07 | $6.72 |

| March | -$3.77 | -$3.68 | $4.80 |

| April | -$4.89 | -$2.93 | $8.26 |

| May | -$4.92 | -$3.04 | $8.03 |

| June | -$6.16 | -$2.80 | $7.36 |

| July | -$5.11 | $0.50 | $10.31 |

| August | -$5.64 | $0.67 | $8.30 |

| September | -$6.60 | $0.59 | $7.34 |

| October | -$8.78 | -$0.32 | $9.03 |

| November | -$7.65 | $1.76 | $6.43 |

| December | -$1.67 | $2.60 | $9.41 |

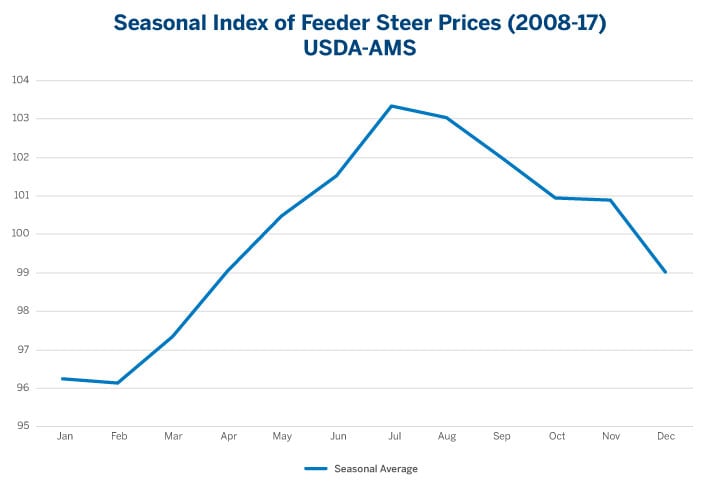

From the basis averages in Exhibit 6, ABC expects the cash price in January to be $2.36 under January futures or $143.065 ($145.425 price of JAN futures less $2.36 January average basis). Feeder cattle prices are at a seasonal low in January, so ABC is trying to lock-in a January selling price of no less than $143.065.

Exhibit 7. Seasonal Index of Feeder Prices

{kind=link}

All 400 of ABC’s 800 lb steers sell at auction on January 20 for an average price of $128.83. ABC then offsets its futures position by buying the JAN futures contract at $131.95. The result from the futures transaction is a profit of $13.475/cwt. (Original selling price of $145.425 minus the buy-back price of $131.95). With the cash market proceeds of $128.83 along with the futures market profit of $13.475, ABC effectively sold their feeder cattle for $142.305/cwt. This is a value above the cash market value on January 20, but is still below the target price of $143.065. This difference between the actual price ($142.305) and the expected price ($143.065) is due to the difference between the expected Texas basis ($2.36/ cwt under JAN futures) versus the actual basis ($3.12/cwt under JAN futures). Even a hedged position faces basis risk – that is basis values that differ from expectation. However, the good news for hedgers is that basis varies much less than price varies; thus, even with basis risk a hedged feeder cattle position faces much less risk than an unhedged position. Exhibit 8 below illustrates the hedging transaction.

Exhibit 8. ABC Hedge Deta

| Cash Market | Futures Market | |

| March | Expect January cash price in TX to be $143.065 | Sell JAN Feeder Cattle futures @ $145.425 |

| January | Actual cash price in Texas of $128.83 | Buy JAN Feeder Cattle futures @ $131.95 |

| Change | -$14.235/cwt loss | $13.475/cwt gain |

|

Sell steers at gain on futures position $128.830 + $13.475 Net Selling Price $142.305 |

||

Example 2: Feedlot Consider a feedlot in Kansas. Big Beef feedlot (BB) buys feeder cattle that are placed on a custom feeding program at their location in Kansas. Typically, cattle are fed a mix of high energy feed to promote rapid weight gain for around 150 days. Once the cattle have reached their finished weight, they are ready to be sold to a packer as “live cattle” to be harvested. At the beginning of April, BB decides that they must start planning to buy more feeder cattle in August to replace the ones currently on feed that will be sold at that time. BB has 2,000 head on feed that will all be sold to a packer in August. They intend on purchasing 2,000 more head in August to replace those sold for slaughter.

To manage the price risk in case the price of feeder cattle will be higher in August when they need to buy replacements, BB buys 31 contracts of the August (AUG) Feeder Cattle futures [(2,000 head / 65 head per CME contract). They buy AUG on April 7 at a price of $135.65. The expected basis in August for Kansas is $0.67 over the futures contract price, so BB anticipates that they will not pay more than $136.32 for the replacements they will buy.

In August, BB buys 2,000 head of feeder cattle in Kansas to refill their feedlot at an average price of $145.15. BB offsets their futures position by selling the AUG contract at $142.90 on August 30. Their hedge was able to lock in a purchase price of $137.90/cwt (paying $145.15 in the cash market minus $7.25 futures profit). The effective purchase price of $137.90 is a little higher than the expected price when the hedge was placed ($136.32) because the basis was $2.25 over futures rather than the expected $0.67 over futures, but still much lower than what they would have had to pay unhedged in the cash market. Exhibit 9 below illustrates the hedging transaction.

Exhibit 9. BB Hedge Detail

| Cash Market | Futures Market | |

| April | Expect August cash price in Kansas to be $136.32 | Buy AUG Feeder Cattle futures @ $135.65 |

| August | Actual cash price in Kansas of $145.15 | Sell AUG Feeder Cattle futures @ $142.90 |

| Change | -$8.83/cwt loss | $7.25/cwt gain |

|

Offset cost of buying steers with futures position $145.15 - $7.25 Net Selling Price $137.90 |

||

The previous examples illustrate the importance of risk management and the basis relationships across regions and seasons when making hedging decisions. The CME Group Feeder Cattle Index and CME Feeder Cattle futures contract provides the marketplace with the correct tools to hedge risk and run a successful livestock operation.

- Created with https://mapchart.net/usa.html

- Commencing with the listing of the May 2019 contract and all subsequent listings, cattle identified as being fancy, thin, fleshy, gaunt or full will no longer be excluded.

- Daily cash prices from the three regions of Texas, Kansas, and Nebraska from 2013-17 were used along with daily futures settlement prices for feeder cattle to analyze the effectiveness of hedging by regions. When data are cointegrated, regression can be done on levels of individual prices. Otherwise, regression on differences of the two price series is more appropriate. A test for co-integration was conducted for each region, the resulting analysis confirmed that the data are co-integrated in all regions, and hedge effectiveness tests were conducted on price levels rather than price differences.

- R-squared is a statistical measure that represents the proportion of the variance for a dependent variable that’s explained by the independent variable. More simply, it is the measure of correlation between the futures and cash. For the purposes of this paper, R-squared is considered the percentage of the regional cash price’s movements that can be explained by movements in the daily futures prices.