{kind=link}

Hedging with Ag Weekly Options

The Agricultural Grain futures and options markets are some of the most liquid and actively traded global commodities in the world. With Weekly options on Agricultural Grain futures expiring on Friday each week, CME Group provides market participants with a flexible tool to fine-tune their cash market exposure. In 2019, Weekly options saw volumes increase 65% compared to 2018, with almost 7,000 in average daily volume. The addition of Weekly options to a trader’s hedging strategy can offer a low-cost tool to mitigate risk associated with physical or financial positions.

Market-moving events such as WASDE reports, changes in trade policy/geopolitics, and weather-related events can significantly impact volatility in agricultural markets. Weekly options give traders a greater flexibility to manage volatility arising from these events, along with the added features of shorter expirations and lower premiums.

Key features

- Expire every Friday that is not a standard expiration date for quarterly/serial options

- Exercise into front month futures contract

- Flexibility to manage short-term volatility and risk

- Precision timing to hedge around high-impact events such as USDA and WASDE reports

- Lower premiums due to less time covered

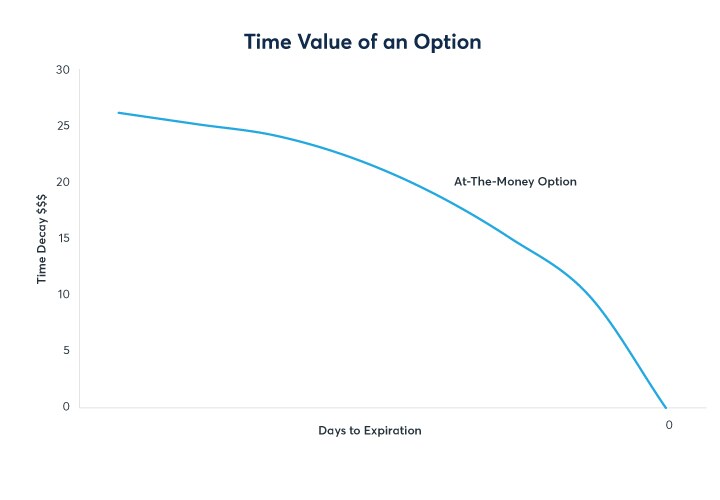

Time-decay (theta decay)

An option loses value as its time to expiration draws closer since there is less time for the option to move in-the-money. This is called time-decay (theta decay) and is an important factor in option pricing. For Weekly options, this provides intrinsic benefits for both the long and short position holders. For the short position holder, the time window in a Weekly option leads to an aggressive decay in premium as the option approaches expiration. For the long position holder, the shorter time window lowers the initial price of the premium paid for the option relative to a longer dated option while still providing short term coverage.

{kind=link}

Weekly options applications

Agricultural Grain options trading is applicable to market participants with exposure to cash market volatility. Since cash markets are settled to a new price each day or series of daily prices averaged, using a specific series of days is useful to fit a given pricing or hedging window for both buyers and sellers. Scenarios in which traders and producers require hedging for short-term price risk exposure can provide opportunities for utilizing Weekly options strategies. While longer-term price risk exposure typically falls into a range along the forward curve influenced by market fundamentals such as supply/demand, cost of storage, interest, and production, market moving events in grain have a way of materializing spontaneously causing short-term price risk exposure to arrive and detach from the longer-term view of the market. In this paper, we will explore the use of Weekly options in the following scenarios/events:

- Trade war and tariffs announcement

- Adverse weather during harvest

- WASDE report release

Example 1: Using Weekly Soybean options to hedge US-China trade war and tariffs announcement

A US-based grain exporter is aggressively selling cargoes of soybeans to Chinese importers in a series of tenders to try and get ahead of a possible trade war between the two countries. There have been persistent rumors and talks about tariffs for weeks, but little action. Chinese buyers are looking to shore up supply in anticipation of an upcoming announcement from the US administration. On these deals, the exporter has long cash flat price exposure against the anticipated tender sales. If they win the tender, the new cash sale offsets their long physical position. Typically even if they do not make the sale, the market tends to rally on the announcement of new export business, and they can hedge their position without taking a loss. However, in the current situation, there is a risk that China could suspended business between the two countries and prices could drop precipitously.

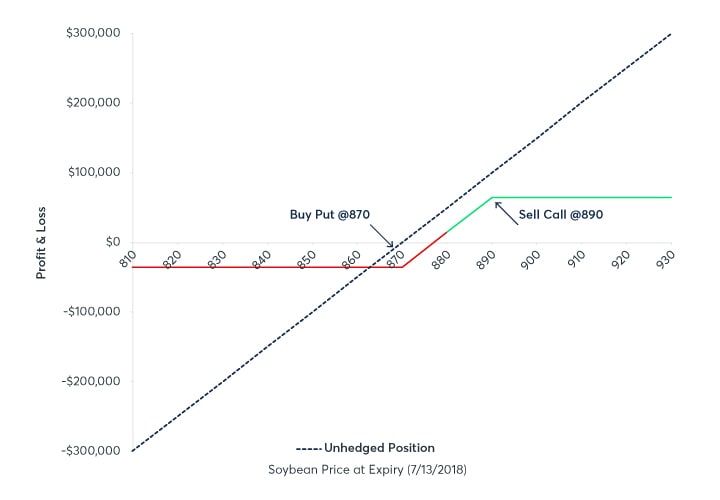

To hedge against this enhanced risk, the exporter implements a collar strategy which includes purchasing an at-the-money Weekly put option and selling an out-of-the-money Weekly call option with the same expiry. This strategy allows the exporter to hedge downside risk while reducing the cost of the strategy by selling the call. The upside of this trade is limited at the strike price of the call, which partially offset the cost of the hedge. Additionally, the exporter’s expiration timeline is precise and tailored to their specific short-term needs.

Date: 07/06/2018

Soybean futures (August18) Price: 870.00¢

Physical position: 500,000 bushels soybeans

Collar strategy:

Buy 100 Weekly puts @870.00¢ for 13.00¢ premium

Sell 100 Weekly calls @ 890.00¢ for 6.00¢ premium

Figure 1. Collar hedge using Weekly options

{kind=link}

On Friday 07/06/2018, the exporter initiates a collar using Weekly options that expire on Friday 07/13/2018. At expiry, the underlying Soybean futures Aug18 price drops and settles at 814.00¢/bu following the US Administration’s announcement to impose tariffs and China’s immediate retaliatory tariffs on US agricultural goods. The sale falls through, and the exporter’s physical position of 500,000 bushels realizes a $280,000 loss in value while waiting to be loaded onto a vessel. However, because the exporter has used Weekly options to construct a collar hedge, the loss is offset with a $245,000 gain generated through the options position ($280,000 gross profit - $35,000 cost to implement the strategy).

Compared to a standard options strategy using the same strikes, the use of Weekly options realized a net savings of 15%, while also providing a tailored time window to meet the exporters unique risk management situation.

| Unhedged Market Position | Position + Weekly Options | |

| Friday 07/06/2018 [text-align: left] | cash Soybean price is 870.00 | Sell Calls @890 for 6.00¢ - Buy Puts @870 for 13.00¢ |

| Friday 07/13/2018 [text-align: left] | cash price after tariff announcement is 814.00 | long weekly puts expire deep in-the-money with 56¢ gain |

| P&l/Change [text-align: left] | 814.00 - 870.00 = (56.00) loss (56.00) loss x 500,000 bu = ($280,000) loss | 56.00 gain – (7.00) premium = 49.00 gain 49.00 gain x 500,000 bu = +$245,000 gain on options position |

| ending Net position Value [text-align: left] | 814.00 X 500,000 bu = $4,070,000 | 814.00 + 49.00 gain = 863.00¢/bu sell price 863.00 x 500,000 bu = $4,315,000 |

Example 2: Pre-hedge adverse weather during harvest using Weekly Corn options

A pre-hedge or anticipatory hedge describes a futures or options position taken in advance of a physical purchase or sale. In grain merchandising and origination, they offer a great way to lock in costs of anticipated purchases or protect against downside price risk of anticipated sales.

In Example 2 we will look at utilizing Weekly Corn options to pre-hedge a large commercial feed yard’s anticipated purchases going into a weekend of potentially adverse weather conditions during harvest. “In the past, our customers have used Weekly options around reports or extreme weather events. Especially when they have a sizeable position, Weekly options can help protect against short-term market fluctuations,” said Trey Warnock, Risk Manager at Texas-based commodity broker Amarillo Brokerage Company.

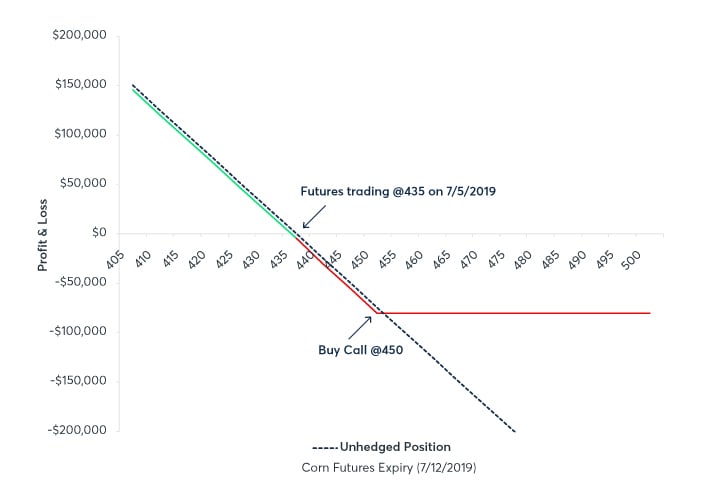

Feed Yard Company ABC has been buying both old crop and new crop harvest delivered corn from producers in the surrounding area as prices have increased on hot dry weather during the growing season. Going into the July 4th weekend, there are conflicting 5-day weather forecasts; there is a slight chance heavy precipitation could put some downward pressure on the market, while another hot streak could result in higher prices and increased old crop deliveries over the weekend. Rather than pre-hedge deliveries with futures, Feed Yard ABC decides to buy an out-of-the-money Weekly Corn call option that expires the following week to reduce a potential loss from upward price action over the weekend.

Date: 07 /05/2019

Corn futures (Sep19) price: 435.00 ¢ per bushel

Physical position: 500,000 bushels

Buying call with physical strategy:

Buy 100 Weekly calls @450.00¢ for 1.00¢ premium

Figure 2. Long call hedge using Weekly options

{kind=link}

On Saturday morning, the chances of wet weather erode, with sustained high heat and sun predicted throughout the week. Over the weekend, the feed yard books an additional 500,000 physical bushels priced at the Monday close. On Monday 07/08/2019, Sep19 futures open sharply up and settle at 455.00¢/bu for a final purchase price of $2,275,000 ($100,000 more than expected on 07/05/2019 when Corn Futures were 435.00¢). However, the feed yard’s increased input costs are offset by the gain realized in the long call option.

| Unhedged Market Position | POSITION + SHORT Weekly Options | |

| Friday 07/05/2018 [text-align: left] | cash price is 435.00 | Buy Calls @450 for (1.00¢) |

| Monday 07/08/2018 [text-align: left] | cash price is 455.00 | exercise in-the-money call options with 4¢ gain |

| P&l/Change [text-align: left] | 455.00 - 435.00 = 20.00 increase in net purchase price 20.00 x 500,000 bu = $100,000 increase in net costs |

5.00 gain – (1.00) premium = 4.00 gain 4.00 gain x 500,000 bu = +$20,000 gain on options position |

| ending Net Purchase Price [text-align: left] | 455.00¢/bu | 455.00 cash price - 4.00 gain from options = 451.00¢/bu |

Compared to a standard options strategy using the same strikes, the use of Weekly options realized a net savings of 105%.

Example 3: Using Weekly Wheat options to hedge WASDE report

In example 3, a US flour mill has been hedging their monthly processing needs in the nearby Chicago Wheat futures contract. There is still a good amount of old crop available and all indications point to a healthy US harvest. While their long-term view of the market remains bearish and they do not feel the need to hedge too far beyond harvest, there is talk the USDA may reduce the world wheat stocks in the upcoming WASDE report. A lower number may temporarily rally the market and increase domestic competition for local supply with the export market.

On the Friday prior to the WASDE report, to extend their physical coverage, the miller has agreed to buy an additional 80,000 bushels to arrive next week at a fixed basis with futures to be price on delivery. While they have no futures price exposure, they are concerned price might go up.

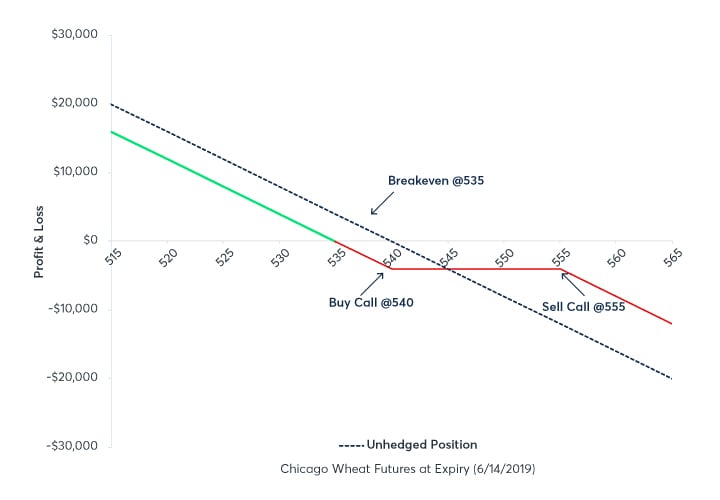

To hedge the increased purchases against temporary upside risk, the miller implements a Weekly bull call spread strategy that expires June 14, 2019. The bull call spread includes buying a lower strike call option and selling a higher strike call option with the same expiry in order to hedge against bullish market expectations. By purchasing a call spread instead of an outright call, the miller reduces the cost of the options hedge in a trade off for limited upside profit.

Date: 06 /10/2019

Wheat futures (Jul19) price: 540.00 ¢ / bu

Expected physical exposure: 80,000 bushels

Bull call spread with physical strategy:

Buy 16 Weekly Wheat calls @540.00¢ for 6.00¢

Sell 16 Weekly Wheat call @555.00¢ for 1.00¢

Figure 3. Bull call spread hedge with Weekly options

{kind=link}

From 06/10/2019 to 06/14/2019, Jul19 Wheat futures rise approximately 4% to 565.00¢/bu corresponding to a lower-than-expected world wheat stocks number from the latest USDA’s WASDE report. While the additional purchased bushels cost the miller an additional 25¢/bu, the gain from the option strategy results in a net price of 555.00¢/bu, a relative bargain compared to the market rate of 565.00¢/bu.

When optimal pricing scenarios come about, the miller can replicate this strategy on a weekly basis to hedge last-minute additional purchases.

| Unhedged Market Position | Position + Weekly Options | |

| Monday 06/10/2019 [text-align: left] | cash price is 540.00 | Sell Calls @555 for 1.00¢ - Buy Calls @540 for 6.00¢ |

| Friday 06/14/2019 [text-align: left] | cash price after WASDE announcement is 565.00 | long weekly calls expire deep in-the-money with profit capped @555.00 due to short call position |

| P&l/Change [text-align: left] | 565.00 - 540.00 = 25.00 increase in net purchase price 25.00 x 80,000 bu = $20,000 increase in net costs |

555.00 - 540.00 = 15.00 gain 15.00 gain – (5.00) premium = 10.00 gain 10.00 gain x 80,000 bu = +$8,000 gain |

| ending Net Purchase Price [text-align: left] | 565.00¢/bu | 565.00 cash price - 10.00 gain from options = 555.00¢/bu |

Compared to a standard options strategy using the same strikes, the use of Weekly options realized a net savings of 115%.

Summary

Grain prices are highly elastic with respect to various fundamental factors including economic data, geopolitical risk, and unanticipated supply/demand issues. Unpredictable changes in any of these factors can have an impact on unhedged financial and physical grain positions. CME Group’s Agricultural Weekly options provide a deep pool of liquidity for market participants to not only express their views on market-moving events, but also manage the volatility associated with them. Using Weekly options, participants can leverage lower option premiums coupled with precision to implement efficient and timely hedging strategies.