{kind=link}

Hedging Repo Exposure in the Treasury Basis with One-Month SOFR Futures

A Treasury repurchase agreement (“repo”) is a key element of any Treasury cash/futures basis trade. For example, being long a Treasury cash/futures basis position involves a long position in cheapest to deliver (or another note/bond eligible for delivery) Treasury note/bond and a DV01 weighted short position in the futures contract. The long basis typically involves financing ownership of a Treasury note or bond with funds borrowed in the Treasury repo market. For this purpose, the borrowing typically occurs in the overnight bilateral repo market1, with the bond or note posted as collateral for the loan.

In the case of a long Treasury basis position, you would pay Treasury repo interest for as long as you hold the basis spread. Conversely, in the case of a short Treasury basis position, you receive Treasury reverse repo interest for as long as you maintain the position. In either case, unexpected shifts in repo rates can significantly impact its profitability.

Bilateral Treasury overnight repo data are a primary input to the Secured Overnight Financing Rate (“SOFR”) benchmark, accounting historically for around 55 percent of the trade activity on which the benchmark is based.2 For this reason, the SOFR benchmark provides a reasonable proxy for your Treasury overnight repo exposure, and CME One-Month SOFR futures offer a good tool for managing this risk.

Suppose that on Sep 28, 2018, you initiate a long cash/futures basis spread in “Classic” 10-Year Treasury Note (“ZN”) futures for Dec 2018 delivery (“ZNZ18”). First, you identified the 2-7/8s of July 2025 to be the Treasury note that is cheapest-to-deliver for the ZNZ18 futures. Assume you purchased $500 million face value of this note for a full price (price + accrued coupon interest) of $498,125,025. On Oct 1, this purchase settles. You intend to finance it by borrowing funds in repo until Dec 30, the day preceding the ZNZ18 contract’s last delivery day, Dec 31.

As a result, you expect to pay Treasury overnight repo from Oct 1 through Dec 30. If you paid SOFR overnight for this time period, you would have paid an annualized rate of 2.241%, which represents the average daily SOFR for this 91 day period. For your $500 M Treasury cash position, the cost from repo to finance your cash position would have been $2,821,754, if your overnight repo rate is identical to SOFR.

To hedge this overnight repo exposure, you would’ve sold similar amounts of October, November and December One-Month SOFR futures. Based upon the timing of your basis trade, your positions result in exposure to the repo rate for 91 days, from Oct 1 through Dec 30. Given the timing of the trade and size of the cash position, you need to sell 302 One-Month SOFR futures distributed across three contract months by number of days to hedge your overnight repo exposure: Oct 102, Nov 100, Dec 100. (302 contracts = ($ full price of note*0.0001*91/360)/$41.67 SR1 DV01)

Assume that you sold each of the Oct, Nov and Dec 2018 One-Month SOFR contracts at their settlement prices on Oct 1. You held the Oct and Nov 2018 One -Month SOFR contracts until their respective final settlement prices. You covered the short Dec 2018 position at the settlement price on Dec 31, the first available trading day following the conclusion of your repo exposure. Because of your futures hedges, you have locked in an average interest rate of 2.246%, nearly identical to the projected rate of 2.241% to finance your position. The average interest rate implied by the final settlement prices of the Oct, Nov and Dec contracts was 2.249%.

Note that the lower rate to finance your position and profits from the hedges are attributable to a relatively higher SOFR of 3% on Dec 31 that was reflected in the SR1Z8 prices, but it was not included in the cost of financing the note. Additionally, the short SR1Z8 position benefited from the market expecting SOFR on 12/31 be higher than it was. SR1Z8 settled at 97.6475 on 12/31, and it had a final settlement price of 97.657.

Please refer to the Exhibit 1 below for the trade details of the One-Month SOFR hedges.

Exhibit 1: One-Month SOFR Hedges: Oct, Nov and Dec 2018 Contracts

| SR1V8 | SR1X8 | SR1Z8 | Average | ||||||||

| Date | Price | Yield | Trade | Price | Yield | Trade | Price | Yield | Trade | Price | Yield |

| 01-Oct-18 | 97.7975 | 2.203 | -102 | 97.775 | 2.225 | -100 | 97.69 | 2.31 | -100 | 97.754 | 2.246 |

| 01-Nov-18 | 97.818 | 2.182 | Settle | ||||||||

| 03-Dec-18 | 97.778 | 2.222 | Settle | ||||||||

| 31-Dec-18 | 97.6475 | 2.353 | 100 | ||||||||

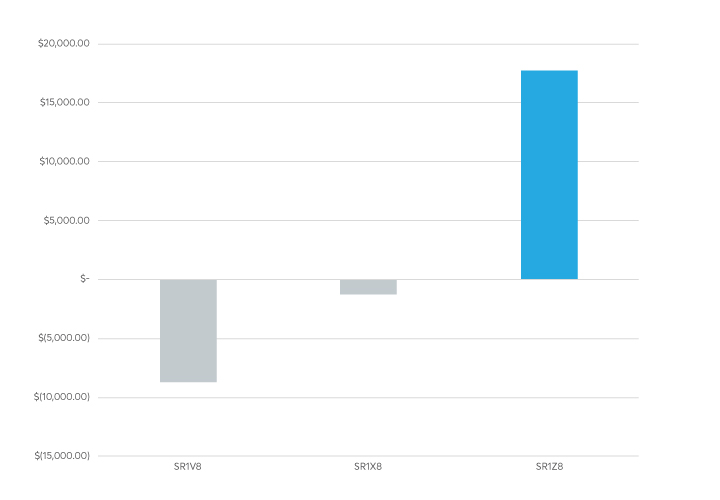

| Profit/Loss | -$8,713.20 | -$1,250.10 | $17,709.75 | ||||||||

As demonstrated in Exhibit 2 below, the net result of this hedging strategy would have produced a gain of $7,746, largely due to a gain of $17,709 in the Dec (SR1Z8) contract, which more than offset losses in the Oct (SR1V8) and the Nov (SR1X8) contracts of $8,713 and $1,250, respectively.

Exhibit 2: Profit/Loss from One-Month SOFR Hedges

302 Contracts: Oct (102), Nov (100), Dec (100) from 1 Oct 18

{kind=link}

The net profit/loss of the hedged positions was small relative to the cost of financing because repo rates were relatively steady. Nevertheless, Treasury repo rates can change unexpectedly due to changes in factors that influence them such as monetary policy and bill issuance. Repo hedgers are encouraged to be mindful of these risks when establishing a hedging strategy.

For example, consider the potential scenario of a surprise tightening of monetary policy. Suppose the Federal Open Market Committee (FOMC) provided an inter-meeting rate hike on Nov 16 by increasing the target range for the effective federal funds rate (EFFR) from 2.25/2.50 to 2.50/2.75. Given the stable spreads between EFFR and SOFR, it is reasonable to assume daily SOFR would be 25 basis points higher for the rest of the applicable dates, Nov 16-Dec 30. In this case, the daily SOFR for Oct 1-Dec 30 is projected to be 2.365%, 12.4 basis points higher than the observed annualized rate for this period. As a result, your expected cost of financing is $2,977,888, an increase of more than $156,000. Your futures hedges would have produced a net gain of more than $164,000, which would fully compensate the higher cost of financing due to the rate hike.

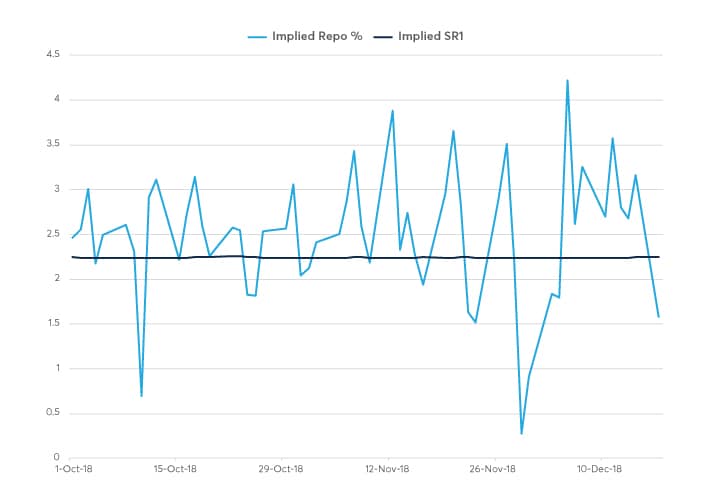

The implied repo rate for a Treasury bond or note future is defined as the rate of return to buying the note or bond and fulfilling futures delivery with it. The bond or note with the highest implied repo rate is typically the cheapest-to-deliver. The implied repo rates are generally consistent with other short-term interest rates. The note in our basis example, the 2-7/8s of July 2025, had the highest implied repo rate, and it was cheapest-to-deliver. Exhibit 3 below shows how the implied repo of this note compared to the implied interest rate of the One-Month SOFR futures hedges, which represents the average daily interest rate of each of the SOFR contract months. The interest rates implied by the final settlement prices were applied to dates that followed the respective settlement dates for the Oct and Nov 2018 contracts.

Exhibit 3: Comparison of Daily Rates, 1 Oct- 17 Dec 2018

Implied Repo for Dec 2018 10-Yr Note Cash (2-7/8s of Jul 25)/Futures Basis (Light Blue)

Implied Rates of One-Month SOFR Hedges (Dark Blue)

{kind=link}

Source: Bloomberg

One-Month SOFR Futures Contract Terms

The structure of the One-Month SOFR (“SER”) futures contract, summarized in Exhibit 4, resembles the exchange’s 30-Day Federal Funds (“FF”) futures in nearly all respects.

Exhibit 4 -- CME One-Month SOFR Futures Contract Specifications

| Trading Unit | Average daily SOFR interest during futures contract Delivery Month, such that each basis point per annum of interest is worth $41.67 per futures contract. |

| Price Basis |

Contract-grade IMM Index: 100 minus R. R = average daily SOFR interest during contract Delivery Month. Example: Contract price of 97.295 IMM Index points signifies R = 2.705 percent per annum. |

| Contract Size | $41.67 per basis point per annum (or $4,167 per contract-grade IMM Index point) |

| Minimum Price Increment (MPI) |

0.005 IMM Index points (½ basis point per annum) equal to $20.835 per contract, provided that:

|

| Termination of Trading |

Last Day of Trading: Last Exchange Business Day of contract Delivery Month. Termination of Trading: Close of CME Globex trading on Last Day of Trading. |

| Delivery | By cash settlement, by reference to Final Settlement Price, on first US government securities market business day following Last Day of Trading. |

| Final Settlement Price: Contract-grade IMM Index evaluated at R = arithmetic average of daily SOFR during Delivery Month. | |

| Delivery Months | Nearest 7 calendar months. |

| Trading Venues and Hours | CME Globex and CME ClearPort: 5pm to 4pm, Sun-Fri. |

| CME Globex Algorithm | Split FIFO and Pro-Rata (K Algorithm, with Top Order Allocation = 100% and Pro Rata Allocation = 100%) |

| Block Trade Minimum Size |

Asian Trading Hours (4pm–12am, Mon-Fri on regular business days and at all weekend times) 125 contracts European Trading Hours (12am– 7am, Mon-Fri on regular business days) 250 Regular Trading Hours (7am–4pm, Mon-Fri on regular business days) 500 |

| Product Codes |

CME: SR1 Bloomberg: SER Cmdty |

Sources

1 See, eg, Adam Copeland, Darrell Duffie, Antoine Martin, and Susan McLaughlin, Key Mechanics of the U.S. Tri-Party Repo Market, FRBNY Economic Policy Review, Federal Reserve Bank of New York, November 2012, available at: https://www.newyorkfed.org/medialibrary/media/research/epr/12v18n3/1210cope.pdf

2 See, eg, Joshua Frost, Introducing the Secured Overnight Financing Rate (SOFR), Federal Reserve Bank of New York, presentation with underlying data delivered at the Alternative Reference Rates Committee (ARRC) Roundtable held on November 2, 2017, available at: https://www.newyorkfed.org/newsevents/speeches/2017/fro171108