{kind=link}

Hedging 3-Year Note Issuance

3-Year Treasury Note futures are an effective hedge for Treasury issuance. On September 8, 2020, the Treasury is scheduled to auction $50B of notes that will be eligible to deliver into the Dec 20 futures contract (Z3NZ0), the active front-month based on volume and open interest.

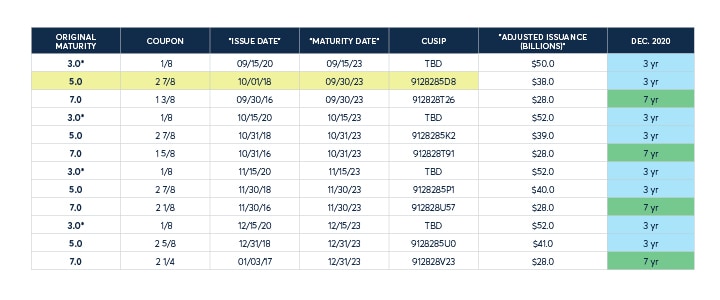

Please refer to Exhibit 1 below for Treasury notes eligible for delivery into the Dec ‘20 contract. The highlighted issue, the 2-7/8s of Sep 2023, is currently the cheapest to deliver (CTD) for the Dec ‘20 contract. The previously available 3-year and 5-year notes are shaded blue and labeled “3 yr”. The recently added 7-year notes are shaded green and labeled “7 yr”.

Exhibit 1

3-Year Note Futures Projected Deliverable Basket, Dec 2020 Contract

{kind=link}

*Assumes new 3yrs issued in Sep, Oct, Nov, Dec have same coupon as Aug issue

Sep, Oct, Nov and Dec issue sized based on Aug quarterly refunding

Several key dates to be mindful of as we are establishing an anticipatory hedge of the 3-year issuance:

- Announcement, Sep 3, when-issued (WI), trading begins

- Auction, Sep 8, when the coupon is determined via the auction process

- Settlement, Sep 15, when the note is made available

Auction participants can hedge the risk of new issuance by establishing short positions in Treasury futures to lock in today’s prices and yields. In contrast to the WI market, which becomes available upon announcement, Treasury futures’ markets are not subject to this constraint.

Suppose we are anticipating being an active participant in the auction. We need to hedge $100 million par amount of the new 3-year note until Sep 15, the issue date. One of several approaches to hedging this exposure with 3-Year Note futures is the DV01 (dollar value a one basis point change) hedge. In this method, the hedge ratio is the portfolio DV01 divided by the futures DV01. Therefore:

Hedge Ratio= Portfolio DV01/Futures DV01

As a proxy for the forthcoming Sep ‘23 3-year note, Portfolio DV01, it is reasonable to assume that it will have similar risk exposure as the recently auctioned, on-the-run (OTR) 3-year, the 1/8th of Aug ’23. As of Sep 1, 2020, the OTR 3-year had a DV01 of $56.11 per $200,000. Here are the steps to calculating a hedge ratio:

- Convert from OTR cash market DV01 ($56.11) in futures equivalent terms, $200K, to size of position being hedged, $100M

- Calculate Portfolio DV01=$28,055= $56.11 X ($100M/$200K)

- Identify futures DV01 of the Dec ’20 contract, $61.70

- Calculate Hedge Ratio= Portfolio DV01/Futures DV01=$28,055/$61.70=454.70 contracts

Therefore, based on our DV01 hedge ratios, we can hedge our position of $100M face value of soon to be issued 3-year notes by establishing a short position of 455 contracts in our Dec 20 3-Year Treasury Note futures.

Please refer to our Treasury Analytics tool for eligible securities, CTD analysis and current DV01s.

Please refer to our Understanding Treasury Futures whitepaper for alternative approaches to hedging with Treasury futures.