{kind=link}

Global Gas Prices Rally Amid Strong Demand

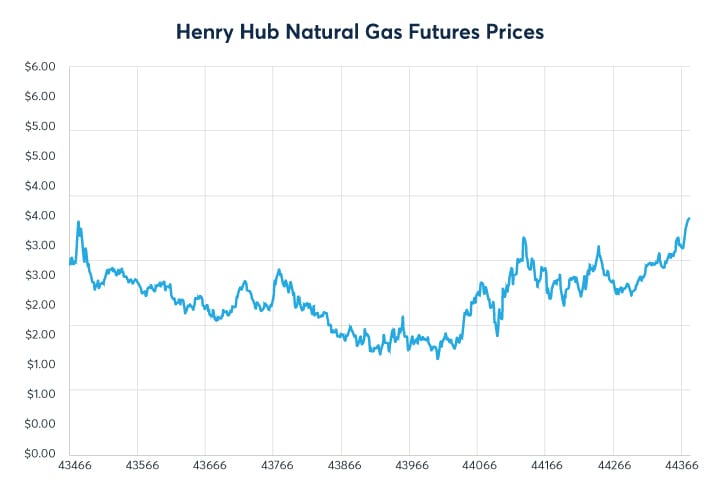

The scorching temperatures and heat wave that descended into the Northern Hemisphere in the middle of June 2021 have pushed natural gas prices to multi-year highs and spurred air-conditioning demand from power plants. Henry Hub Natural Gas futures have come under pressure, with prices trading above $3.5 per MMBtu (Figure 1) as power burn demand hits record highs and US liquefied natural gas (LNG) exports continue to exhibit resiliency.

Figure 1: Bullish environment, driving Henry Hub futures prices to rally

{kind=link}

Source: CME Group

Natural gas demand has spiked as a result of a significant increase in cooling loads that has led to gas being taken out of storage. For the week ending June 30, working natural gas stocks totaled 2,558 Bcf, which is 17% lower than the year-ago level and 5% lower than the five-year (2016–2020) average.

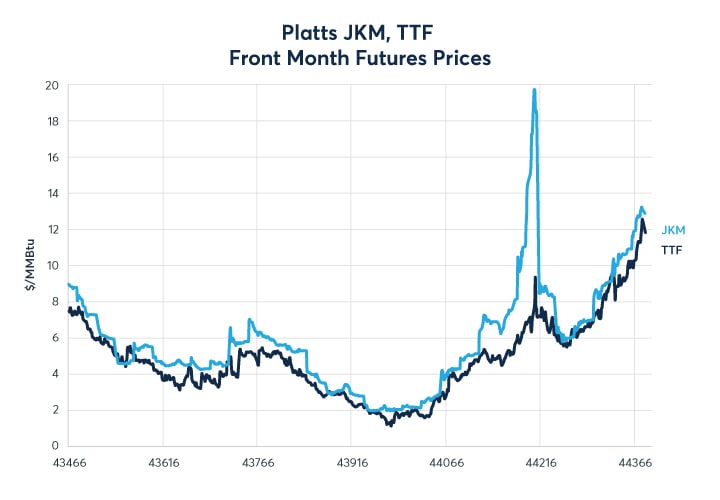

International gas prices have also reached multi-year highs amid strong fundamentals ranging from low storage levels and tight supply in Europe to the demand strengthening from the power sector in Asia. Japan/Korea Marker (JKM) Front-Month futures jumped to $13 MMBtu while the JKM spot price surged to $14 as a response to economic recovery and the increase of coal-to-gas switching mainly in China (Figure 2). As JKM and Henry Hub are driving arbitrage opportunities, and given the price premium, more cargoes are being redirected to the Asian market. This has tightened supply in Europe and pushed Dutch Title Transfer Facility (TTF) prices to record highs.

Figure 2: Strong fundamentals propelled JKM and TTF prices

{kind=link}

Source: CME Group, Platts

Global LNG trade has expanded for the second consecutive year despite the onslaught of the pandemic on the demand side. The continued growth has been driven largely by US exports, which hit historic records in the first two quarters of 2021, while exports from almost all other producing countries experienced a decline. The US LNG industry has exuberated resilience and flexibility despite the extreme market shock caused by an unprecedented level of export curtailments and cargo cancellations during the COVID-19 pandemic.

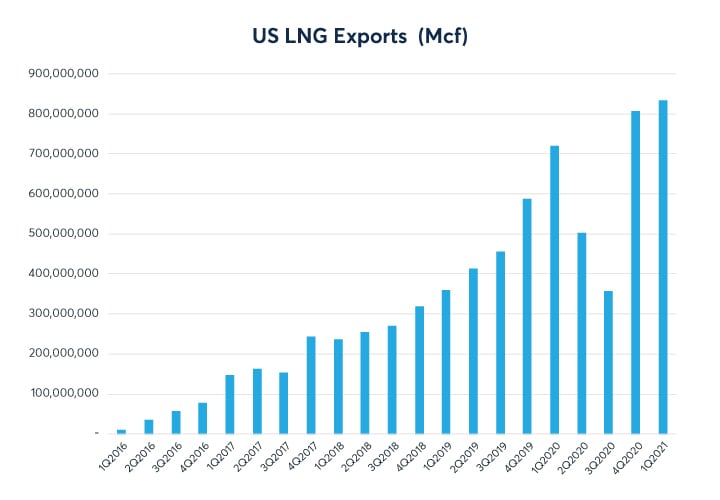

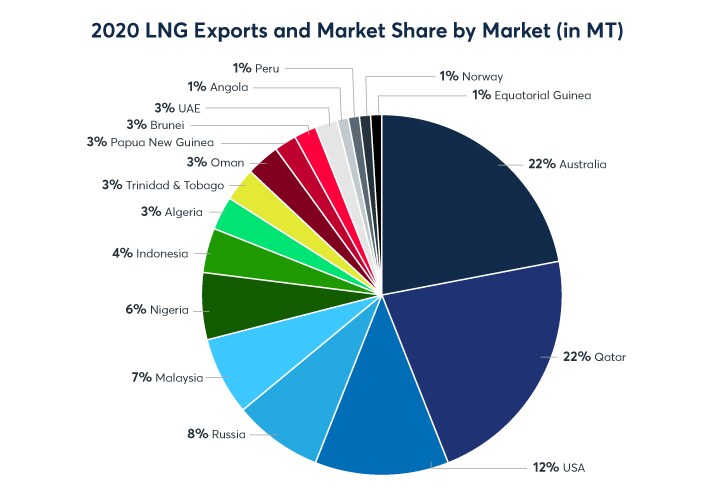

US LNG exports have demonstrated remarkable strength after bouncing back rapidly from historic lows of 3.1 Bcf/d during last summer to a record levels of 9.41 Bcf/d and 9.8 Bcf/d in November and December 2020 successively, exceeding the previous record in January 2020 of 8 bcf/d (Figure 3). Australia overtook Qatar as the largest LNG exporter in the world , exporting 77.8MT in 2020 while the US remained the 3rd largest exporter of LNG at 44.8 MT after eclipsing Malaysia in previous year ( Figure 4).

Figure 3: US LNG exports have recovered after overcoming a short-term market shock related the pandemic

{kind=link}

Source: DOE

Figure 4: The US and Australia have replaced the traditional LNG producers

{kind=link}

Source: IGU and GIIGNL

US supply flexibility

The flexibility of the US LNG contract and its resilience to extreme market shocks has reinforced the critical role of the US as the world’s LNG swing producer. The US has dynamically rebalanced the global market by redirecting cargoes where needed and by adjusting production and utilization rates in accordance with demand levels. The pandemic caused major cargo cancellations which slashed export volume by 61% back in July 2020 compared to the beginning of the year. Approximately, 1752 US LNG cargoes were cancelled between April and November 2020 across all US terminals.

Cancellation rights are among the unique contractual provisions that have been pioneered by US LNG exporters. Once these clauses are triggered, the offtaker (LNG buyer) can forgo lifting an LNG cargo and only pay a fixed cancellation fee, without being liable for the cost of the LNG. On the other hand, the seller/terminal has the optionality to resell the cancelled cargo in the spot market as long as the cancellation fee covers the cost of producing LNG. The flexibility of the contract’s structures and the art of portfolio optimization have insulated US terminals from major financial impacts.

The pandemic has provided an opportunity to stress test the performance of the US LNG business model with its unique flexibility. This has begun to incentivize some global market participants, mainly in Asia, to emulate the US contractual structure, resulting in the rise of new generations of LNG contracts.

Capacity buildup

Global liquefaction capacity grew by more than 20 MTPA compared to 2019 ‒ reaching 454 MTPA in 2020. This expansion was largely driven by capacity addition in large-scale US projects that started commercial operations such as Cameron LNG T2–3 (8.0 MTPA), Freeport LNG T2–3 (10.2 MTPA), and Elba Island T4–10 (1.75 MTPA). Though, many pre-Final Investment Decision (FID) liquefaction projects continue to struggle to secure financing due to market oversupply, which was exacerbated by the demand contraction during the pandemic. In addition, supply chain issues have adversely impacted some under-construction projects.

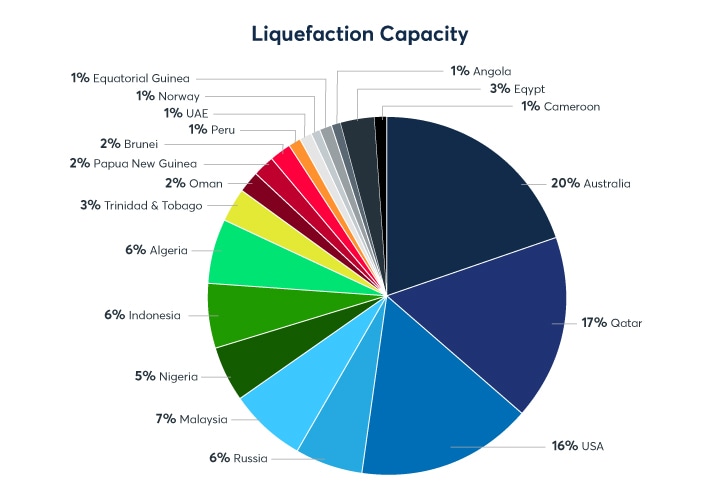

Figure 5: The US, Australia, and Qatar have more than 50% of the global LNG liquefaction capacity ‒ global operational liquefaction capacity by country

{kind=link}

Source: Rystad Energy and IGU

Qatar recently announced a plan to move forward with building North Field East Project (NFE), the world’s largest LNG project, which will ramp up production capacity from 773 million tons per annum (MMTPA) to 110 MMTPA. The announcement represents an aggressive attempt to restore Qatar’s dethroned position and to compete with rising LNG titans ‒ Australia and the US.

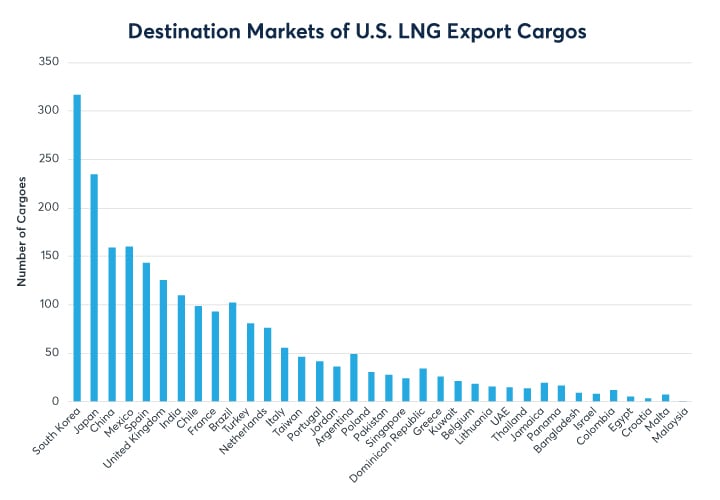

Figure 6: South Korea, Japan, and China are the largest importers of US LNG

{kind=link}

Source: DOE

US LNG exports have reached over 35 countries since it started exporting in 2016 ‒ with Asia the leading destination, importing 44% of total US exports (Figure 6). The region has recovered relatively quickly from COVID-19, attracting a 71%4 share of global LNG imports, an increase of 69% compared to last year. LNG imports into most Asian countries have experienced growth, except Japan, where LNG consumption decreased by 3.2% in 2020. Despite the decline, Japan remains the world’s largest LNG importing country as well as the largest importer of US gas. However, LNG demand from China has been progressively gaining ground after a turbulent year amid the increased competitiveness of LNG versus other fuels, which has led to some coal to gas switching. Moreover, the accelerating economic recovery has been a catalyst in invigorating consumption from the industrial sector. China is expected to continue driving the global demand recovery as natural gas and LNG are poised to play a key role in the country’s efforts to reach its target of zero emissions by 2060.

European net imports contracted due to the extended lockdowns in many European countries which negatively impacted economic activity. Nevertheless, Europe’s extensive infrastructure and storage facilities acted as the balancing market that absorbed supply when the Asian market was constrained.

Sources

- EIA - https://www.eia.gov/todayinenergy/index.php?tg=lng%20

- https://www.spglobal.com/platts/en/market-insights/latest-news/natural-gas/102120-no-us-lng-cargoes-canceled-from-cheniere-terminals-for-december-sources

- https://www.reuters.com/article/qatar-petroleum-lng-int/qatar-petroleum-signs-deal-for-mega-lng-expansion-idUSKBN2A81ST

- https://www.energy.gov/fe/listings/lng-reports