{kind=link}

Fed Funds Futures in a Post ZIRP World

Fed Funds Futures in a Post-ZIRP World

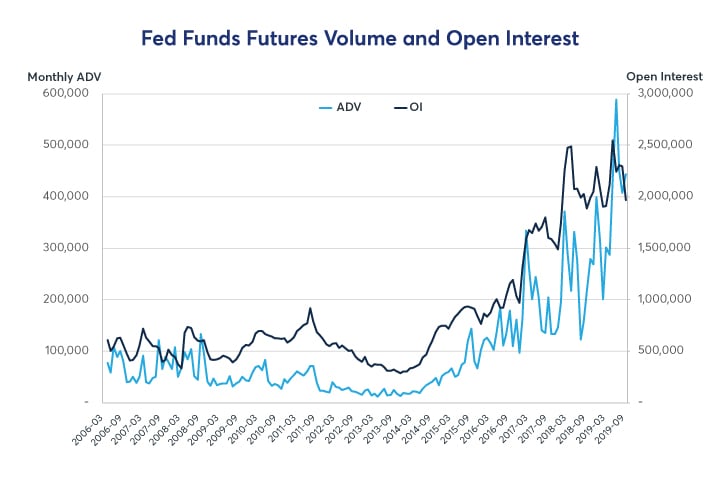

As the FOMC returns to more active management of its key target rate, Federal Funds futures have experienced dramatic growth.

{kind=link}

Source: CME Group

Contract Background

The Federal Funds (FF) futures contract provides a hedging tool for market participants seeking to hedge movements due to Federal Open Market Committee key rate decisions, settling each month to a simple average of the daily Effective Federal Funds Rate subtracted from 100. The EFFR value in turn is calculated by the Federal Reserve of New York as a volume-weighted median of overnight federal funds transactions1, making the futures contract price a measure of average overnight borrowing throughout a given month.

By design, EFFR exerts impacts far beyond the market for interbank borrowing. For market participants affected by Federal Reserve policy, the FF futures provide a reliable pool of liquidity in which to hedge short term interest rate movements, predicting upcoming policy decisions to a fair degree of accuracy. FF contracts with longer terms to expiry also allow market participants to act on views as far ahead as a year, which naturally adds variability since the FOMC incorporates new economic data into each meeting’s outcome. Since the end of the Global Financial Crisis (GFC) in 2009, trading volume and open interest have grown dramatically, making it easier than ever to establish and manage positions.

Fed Funds Futures as FOMC Predictors

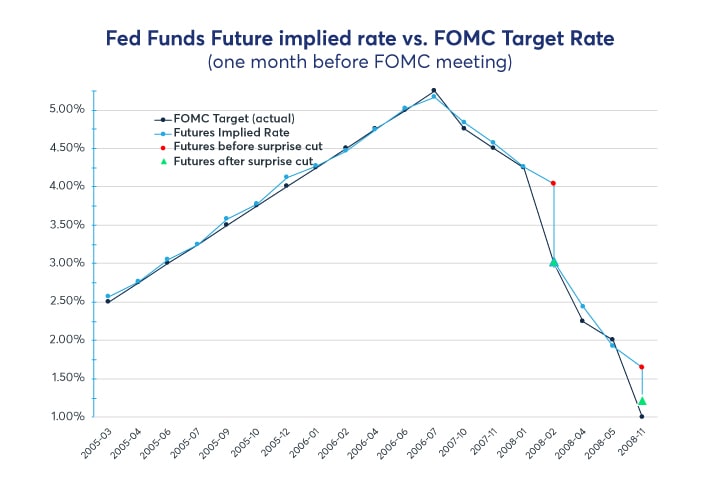

In measuring the track record of the FF futures in predicting FOMC rate changes, we split the data into three time periods. The first included the market top in 2007 and subsequent selloff of the Global Financial Crisis in 2008, a time of active FOMC policy changes. This period saw 19 changes to the Federal Reserve’s target rate, from the hikes in 2005-2006 as the economy overheated, to cuts throughout 2007-20082. The final recession-era cut took place at the end of 2008, when the prior practice of targeting a single EFFR level was replaced with a range of zero to 0.25%, beginning the era of zero interest rate policy (ZIRP).

For our evaluation, we used the nearest “clean” contract month; that is, the FF contract month whose full calculation period falls after a given FOMC meeting. Taking a three-day snapshot of FF futures prices four weeks ahead of the meeting, we compare the implied rate the market expects to the Fed Target rate after the FOMC meeting. For example, ahead of a mid-June FOMC meeting, the July FF future’s price would be the predictor.

By this measure, FF futures-based predictions were quite accurate, pricing an average around two basis points away from the target rate for the first 15 meetings, with a maximum divergence of 11 basis points when moves of 50-75 bps occurred regularly. The two outliers arose in January and October 2008, when the Federal Reserve made emergency cuts totaling 125 and 100 basis points for those months. As shown in Exhibit 2, futures estimates a month out (red dots) did not anticipate off-cycle or larger than standard cuts, but after each unscheduled cut the futures quickly re-priced to include the new expectations, landing within 10 bps (green triangles) of the realized target rate.

Exhibit 2: Fed Funds futures as FOMC predictors, 2005-2009

{kind=link}

Source: Federal Reserve Bank of New York, CME Group

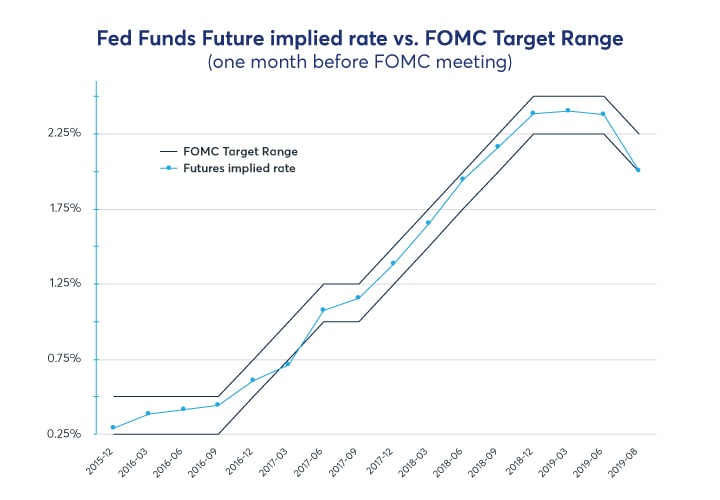

Post-recession, ZIRP persisted for nearly seven years, with the target range fixed at zero to 0.25% and futures contracts priced accordingly. With no FOMC rate changes or guidance to the market regarding plans for one, volatility was minimal and thus we have excluded this quiet period from our predictability analysis.

By the latter half of 2015, anticipation of a new period of tightening picked up in earnest. The first hike in the range came in December, and from there predicting the pace of tightening again became a concern for market participants. Over the next four years, the Federal Reserve made a series of nine increases followed by a cut in autumn 2019, this time setting a rate range in lieu of a specific level. During this new post-ZIRP regime, Fed Funds futures stayed almost entirely within the Fed Target range, even as cut and hike trends changed.

Exhibit 3: Fed Funds futures as FOMC predictors, 2015-2019

{kind=link}

Source: Federal Reserve Bank of New York, CME Group

Trading the FOMC Meeting

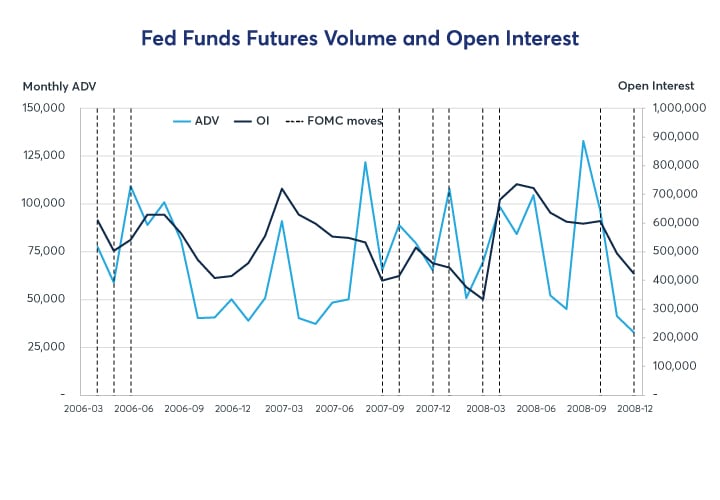

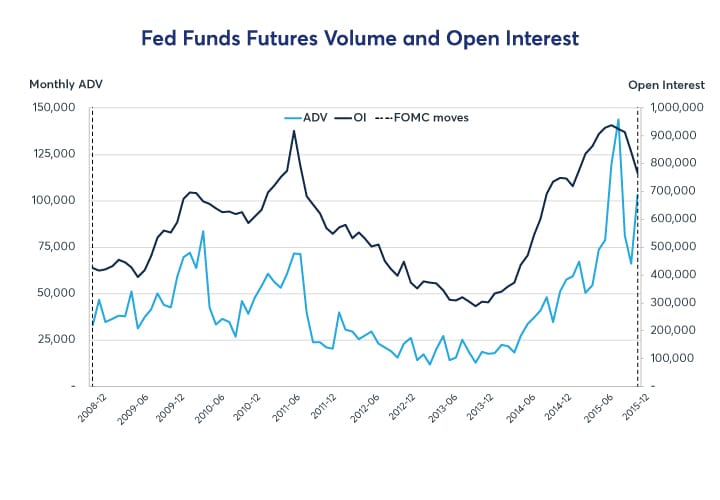

Our first time interval, encompassing the runup to the GFC, saw modest but steady volume and open interest, providing a good baseline to compare to modern liquidity levels. As the financial bull market peaked, crashed, and recovered between 2005 and 2009, the ensuing Federal Reserve intervention generated ebbs and flows in activity, until the “new normal” of interest rates near zero set in.

Average daily FF volume during this time stayed in the 50-100k contract per day range, with spikes to around 125,000 during volatile periods leading up to FOMC movements, and minima during less uncertain periods in between. Open interest was similarly rangebound, roughly between 350,000 and 700,000 contracts, with a less direct link to Federal Reserve policy. In Exhibit 4, changes to the EFFR level targeted by the FOMC are shown at the vertical dashed lines.

Exhibit 4: Fed Funds futures activity, 2006-2009

{kind=link}

Source: CME Group

While the ZIRP period offered little in the way of rate policy changes, the activity in the futures market shows a few points of heightened scrutiny during worries about a double-dip recession or European debt problems, in 2010 and 2011. Between those exceptions, the lack of U.S. rate uncertainty kept trade activity relatively subdued throughout this time period until 2015 when renewed anticipation of FOMC activity sent both volume and open interest back up.

Exhibit 5: Fed Funds futures activity, 2009-2015

{kind=link}

Source: CME Group

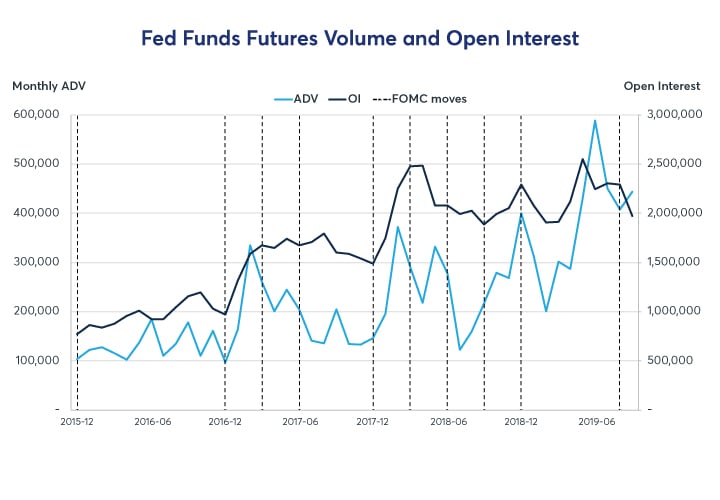

In 2015, as the economy regained its strength, the Federal Reserve made the first of nine increases through 2018, followed by a cut in autumn 2019. Volume and open interest trended sharply upward, with visible spikes preceding rate changes. Even when compared to the active FOMC periods of the GFC, both volume and open interest increased by around a factor of five.

Exhibit 6: Fed Funds futures activity, 2015-2019

{kind=link}

Source: CME Group

Growth in Liquidity and Market Participation

As a measure of risk management, we can look to the FF futures DV01, the dollar value of a one basis point (1/100th of a percent) move per contract. Contract terms fix this at $41.67. Accordingly, 2.1 million contracts of open interest as of September 2019 represent nearly $90 million in aggregate DV01 exposure. For a typical FOMC rate move of 25 bps, the corresponding FF price move would create a settlement variation movement of roughly $2.25 billion of DV01 exposure between holders of long and short positions, representing a substantial potential for hedging activity. The DV01 value also compares quite favorably with the Exchange’s most liquid interest rate products, US Treasury Note and Bond futures, shown in Exhibit 7.

Exhibit 7: DV01 of Fed Funds and Treasury futures

| Product | Fwd DV01/contract | Open Interest | Total DV01 |

| Fed Funds | 41.67 | 2,146,955 | $89,463,615 |

| 2yr | 33.54 | 3,528,880 | $118,358,635 |

| 5yr | 40.57 | 4,107,212 | $166,629,591 |

| 10yr | 62.26 | 3,585,666 | $223,243,565 |

| TN | 88.23 | 811,439 | $71,593,263 |

| Bond | 165.00 | 994,460 | $164,085,900 |

| UBE | 210.00 | 1,168,015 | $245,283,150 |

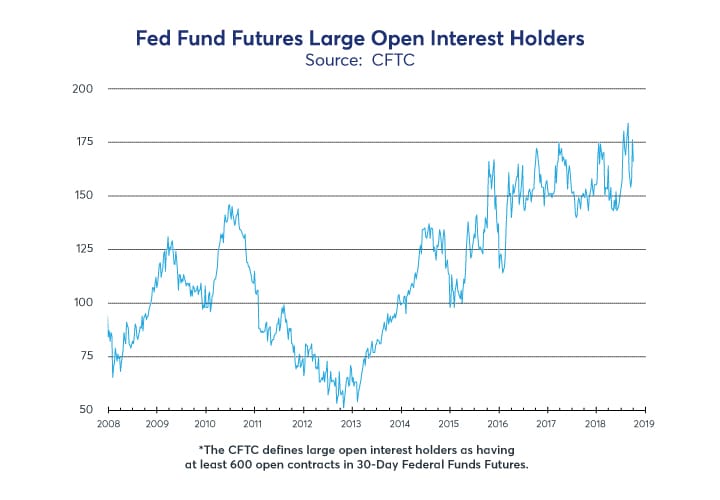

Beyond depth of market, we also have evidence of the increasing breadth of participants since the GFC in the form of the Large Open Interest Holders count tracked by the CFTC3. Based on established reportable position levels, this is an indicator of the number of active parties in a contract. For the Fed Funds futures, this quantity has more than doubled since the recession, and more than tripled since the depths of the zero interest rate environment around 2013. This indicates the growing volume was not simply concentrated among a few extremely large players but rather came from new participants and smaller players increasing their holdings over time.

Exhibit 8: Large Open Interest Holders, post-recession

{kind=link}

It seems reasonable to conclude that the growth in trading volume and participation in this market has increased the spectrum of viewpoints being incorporated into its price discovery, increasing its predictive abilities. But whatever the cause, the Fed Funds futures serve as an efficient tool for near-term interest rate hedging.

Contact Us

For more information about Federal Funds futures please contact…

Bobby Timberlake

+1 312 466 4367

Jonathan Kronstein

+1 312 930 3472

Frederick Sturm

+1 312 930 1282