{kind=link}

EFRP Transactions for Equity Index Products

Exchange for Physical (EFP) transactions originated over a century ago in US markets for grains and grain futures. Since then the practice has been adopted in other commodity futures markets as well as in financial futures markets, and it has been expanded and generalized as Exchange for Related Position (EFRP) transactions, comprising Exchange for Risk (EFR) trades and Exchange of Options for Options (EOO) trades in addition to EFPs.1

This document gives an overview of EFRP practices in equity index futures and options listed on the CME Group designated contract markets (Exchange or CME Group Exchanges). In what follows, Section (1) defines the essential features of an EFRP. Section (2) summarizes and illustrates the rules of the road for entering an EFRP transaction. Section (3) discusses the rôle that EFRPs play in the greater liquidity pool for the Exchange’s equity index products, and Section (4) offers a birds-eye view of the scale of EFRP trading activity among the Exchange’s equity index futures listings.

(1) What is an EFRP?

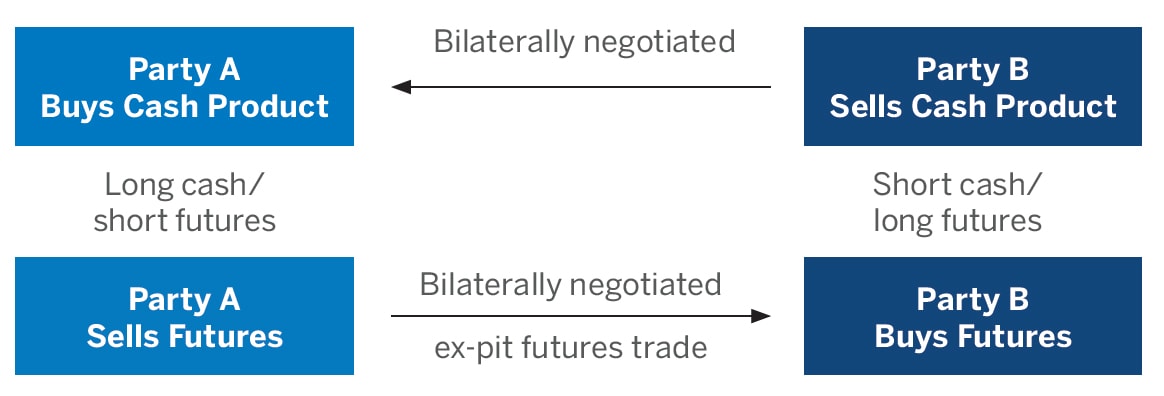

For futures, an EFRP trade is the simultaneous sale/purchase of an Exchange futures position and the purchase/sale of a corresponding, economically offsetting position in either:

- a physical or cash-market asset, or an over-the-counter (OTC) forward contract on a physical or cash-market asset, in the case of an EFP, or

- an OTC derivative contract position, in the case of an EFR.

For options, likewise, an EOO trade comprises the simultaneous exchange of a position in an Exchange option (ie, an Exchange-listed option on an Exchange-listed futures contract) for an economically offsetting position in an OTC option contract. See Exhibit 1.2

Exhibit 1 – Schematic of an EFRP Trade

{kind=link}

The hallmark of an EFRP is that the futures leg of the trade is not executed in the Exchange’s centralized competitive market (ie, neither the CME Globex electronic trading platform). Rather, it is executed through a privately negotiated, non-competitive, off-exchange transaction.

The EFRP’s futures leg must be reported to the Exchange, and it is cleared by CME Clearing, like any Exchange-listed product. Beyond this, the Exchange plays no direct role in facilitating the trade. Notably, the two parties to the EFRP, and not the Exchange, remain responsible for subsequent maintenance and bookkeeping of the physical asset exposure or OTC derivative position entailed in the cash leg of the trade.

What Makes the Related Position Related?

An Exchange for Related Position transaction qualifies as such only if both legs of the trade are in fact “related.” The cash leg must be a legitimate economic offset to the futures leg in terms of its scale (Exchange Rule 538.E.) and its relation to the futures contract’s underlying commodity (Exchange Rule 538.C.). Specifically, the asset exposure represented by the cash leg must be (a) identical to that which underlies the futures leg, or (b) a by-product, related product, or OTC derivative of the futures contract’s underlying commodity, with a reasonable degree of price correlation between them.

The Exchange’s Market Regulation Department establishes and publishes standards for acceptability of offsetting positions. For an EFRP in any of the Exchange’s equity index contracts, for instance, allowable offsetting positions include “stock baskets, provided [that any such] basket is highly correlated to the [contract’s underlying] index and, further, that the basket represents at least 50% of the underlying index by weight or includes at least 50% of the stocks in the underlying index. The notional value of the basket must be approximately equal to the value of the corresponding [Exchange equity index] contract. Other acceptable instruments include equity index swaps and swaptions, OTC equity index options, ETFs and ETNs.”3

(2) EFRP Trade Mechanics

An EFRP may be transacted at any time, at any price that is both mutually agreeable to the counterparties and commercially reasonable. For practical purposes, “commercial reasonability” means that if the price agreed for the EFRP’s futures leg is away from prevailing market levels, then the counterparties may be required to demonstrate that the price is indeed legitimate.

Upon agreement to the transaction’s terms, the resultant futures position must be reported to CME Clearing as soon as possible, either by the counterparties’ CME Clearing member firms or by the counterparties themselves, via CME Direct or CME ClearPort.4 Absent extenuating circumstances, submission must be made on the same day the trade is executed. In all events, an EFRP submitted to the Exchange is not considered to have been accepted by CME Clearing until (a) the transaction has cleared and (b) the first payment of settlement variation and performance bond has been confirmed.

The assets or OTC derivatives entailed in the EFRP’s cash leg are not reported to the Exchange and are presumed to be held in suitable accounts established by the counterparties. If a trade investigation or periodic audit by the Exchange’s Market Regulation Department calls for it, however, the CME Clearing member firms who act on behalf of the counterparties to the EFRP may be required (i) to obtain from the respective counterparties the relevant records evidencing that the cash leg was indeed transacted and that it meets Exchange standards as a permissible offsetting position and (ii) to provide such records to the Market Regulation Department.

Example

An EFRP often involves a dealer who quotes markets in such transactions and a customer of the dealer. Where the dealer has an affiliated futures commission merchant, the customer typically is required to carry both a futures account in which the EFRP’s futures leg is booked and a securities account or bank account in which the cash leg is booked.

With this in mind, consider an investment manager who holds approximately 1.83 million shares of the Consumer Discretionary Select Sector SPDR® Fund (XLY), worth $200 mln. (See Exhibit 2.) Because maintenance margin applicable to CME E-mini Consumer Discretionary Select SectorTM (XAY) futures is around 3.4% versus the Reg T (50%) or prime broker (15-20%) margin rates applicable to XLY, the investor can free between $25 mln and $80 mln of cash by exchanging her ETF position for XAY futures.

She asks the dealer to quote an EFP market in futures expiring in September 2018 (XAYU8) versus XLY. The dealer quotes a bid/ask of +1.85/+2.15, in terms of the price basis versus the previous day’s closing level of the S&P Dow Jones Consumer Discretionary Select Sector index, 1102.61. The investor agrees to buy futures at the dealer’s offered price of 1104.76 (equal to 1102.61 plus the offered basis spread of 2.15). At the same time, the investor and dealer agree to exchange the XLY position at its previous day’s net asset value (NAV) of 109.44.

Exhibit 2

| Dealer | Investor | |

| Starting positions | Flat | +1,827,485 XLY ≈ $200 mln |

| EFP is privately negotiated | Dealer and asset investor agree terms of EFP: * Investor buys and dealer sells 1,810 XAYU8 at 1104.76 (+2.15 basis the previous day’s closing index level of 1102.61) * Investor sells and dealer buys 1,827,485 shares of XLY at prior day’s NAV of 109.44 ≈ $200 mln |

|

| Dealer reports cash trade via TRF | +1,827,485 XLY | -1,827,485 XLY |

| EFP is reported to Exchange | Dealer’s and investor’s CME Clearing member firms report EFP to Exchange via CME Direct or CME ClearPort. Agreed futures price, 1104.76, is achieved by executing EFP as two trades, each at contract minimum price increment of 0.10 index points. |

|

| Dealer futures account -1,418 XAYU8 @ 1104.80 -392 XAYU8 @ 1104.70 | Investor futures account +1,418 XAYU8 @ 1104.80 +392 XAYU8 @ 1104.70 | |

| Final positions | -$200 mln of XAYU8 +$200 mln of XLY Net market exposure is flat. | +$200 mln of XAYU8 |

Since XAY futures can trade only in minimum price increments of 0.1 index points, the futures leg of the EFP is booked in two lots: 1,418 contracts at 1104.80, and 392 contracts at 1104.70. The CME Clearing member firms for the dealer and the investment manager promptly report these transactions to the Exchange, in accord with the rules for EFRP execution. The dealer also reports to the Financial Industry Regulatory Authority’s Trade Reporting Facility (TRF) a client-sale/broker-purchase of 1,827,485 XLY at 109.44.

At completion of the EFP, the investor and the dealer have different positions but essentially the same market exposure:

- Before the trade, the investor was long $200 mln of index exposure via ETFs. After the trade, she is long an equivalent index exposure of CME XAY futures.

- Prior to the transaction, the dealer had no position. After the transaction, the dealer holds equivalent and offsetting index exposures, long the ETF and short XAY futures.

Tailing the EFRP Ratio

In this example, the notional values of the two legs of the EFP turn out to be equal. In many instances, however, the EFP’s legs do not, and should not, match because of the cash-futures basis that stands between them. The futures contract in the EFP signifies a claim on a future value of its underlying equity index, whereas the EFP’s related position is a transfer, typically for spot settlement, of cash index exposure (or some suitably close proxy for the index). The size of the differential between them depends on several factors: (a) the length of the interval until final settlement of the futures leg, (b) the expected level and volatility of stock lending or financing rates during that interval, (c) the expected pace of dividend payouts during that interval, and (d) the prevailing degree of uncertainty among market participants in regard to (b) and (c).

To compensate for these differences, the parties to EFP transactions often agree to apply “tail” adjustments either to the number of futures contracts exchanged (where the trade specifies a given notional exposure to an ETF or cash equity basket) or to the size of the related position (where the trade specifies a given number of futures contracts). Either way, the objective in applying the “tail” adjustment is for the EFP’s legs to have comparable price sensitivity to market dynamics, despite having possibly different notional values.

NAV Pricing

As the example illustrates, prevailing market practice is to price and trade the physical leg of an EFP by reference either to the prior day’s closing share prices (where the related position is a cash equity basket) or to the prior day’s NAV (where the related position is an ETF). Because the NAV reflects not only the prices of the ETF’s component shares but also the accrued dividends and cash held in the fund, occasionally the NAV price may have to be adjusted to reflect any changes that have occurred since the previous day (eg, a component stock of the ETF having gone ex-dividend).

Alternatively, it is possible to execute an EFRP after the close of cash market trading, by reference to the closing value of the related position (either the closing prices for a cash equity basket or the closing NAV for an ETF) as of the EFRP trade date.

(3) What Do EFRPs Do?

The signal feature of any futures contract is the centralized, competitive, all-to-all market in which it trades and in which price discovery occurs. US law requires any futures exchange it regulates to “provide a competitive, open, and efficient market and mechanism for executing transactions that protects the price discovery process of trading in the centralized market.”5 The corresponding regulatory requirement is that “all purchases and sales of any commodity for future delivery, and of any commodity option, on or subject to the rules of a contract market shall be executed openly and competitively” through the market’s central limit order book.6

Exceptions, such as EFRPs, are permitted for transactions to be executed non-competitively, provided that such exceptions are:

(a) authorized by exchange rules that have been submitted to and approved by the US Commodity Futures Trading Commission, and

(b) “made in accordance with written rules of the contract market”, and

(c) made for “bona fide business purposes.”

Since before the 1920s the Exchange’s rules have allowed noncompetitive, privately negotiated EFP trades as an accommodation to grain elevator operators, millers, and processors for whom the basis spread between the futures price and the spot price of grain at the location of business is a pivotal commercial concern. A century later -- in a more general acknowledgement of the needs of commercial users of futures and options -- the Exchange’s rules permit a broader range of EFRP trades to be privately negotiated rather than competitively executed.

An EFRP transaction meets these needs in potentially several ways. For users of the Exchange’s equity index futures and options, the most common are7 --

- Basis integrity – An EFRP facilitates not only accuracy of hedging but also arbitrage trading, because it ensures that the basis relationship between the futures contract price and the price of the contract’s underlying commodity is preserved, irrespective of the transaction’s size.

- Price uniformity -- The buyer and seller of the futures contract may use an EFRP as a means to ensure they can execute a large transaction at a single price.

- Trade facilitation -- In a futures market that is historically illiquid -- or for a transaction that takes place at an hour of day when an otherwise liquid futures market is relatively inactive -- the buyer and seller of the futures contract might use an EFRP to ensure they can execute the trade at all.

Common applications of EFRPs in the Exchange’s equity index products illustrate these functions –

Synthetic Stock Loans and Inventory Management

Suppose a rise occurs in market demand for borrowings in a particular ETF or in the component stocks of the ETF basket. A broker/dealer can use the EFP market to obtain additional lendable supply. By lowering his offered price (ie, the price at which he would sell Exchange equity index futures for an offsetting purchase of physical shares), he can induce a long holder of either the ETF or the component stocks to exchange them for futures. On the other side of the trade, a long holder of the ETF or the component stocks who is bound by restrictions on stock lending may be able to use the EFP mechanism as an alternative means of participating.8

Index Arbitrage

Throughout the day, index arbitrageurs buy and sell baskets of index component shares, index ETFs, and index futures to capture the profit opportunities that arise through transient misalignments in relative values. Many such arbitrage trading firms are unable to carry large inventory positions overnight. In instances where intraday trading activity results in an arbitrageur holding on his books a large stock balance and a comparably large offsetting short position in index futures, an EFP transaction may be a convenient means for him to collapse these positions so that he may continue to transact.

Delta-Neutralizing OTC S&P 500 Index Option Trades

EFR transactions in either E-mini S&P 500 Stock Price Index (ES) futures or S&P 500 Stock Price IndexTM (SP) futures make a convenient tool for achieving uniform and reasonably precise offsets to the residual delta exposures in purchases or sales of OTC S&P 500 Index options. In this application, the ES or SP futures obviously stand as the “futures” leg, while the OTC equity index options or option combinations serve as the “related position.” It merits emphasis that only bona fide OTC options qualify for use in such EFR transactions. Neither the index option products that are listed for trading on securities exchanges nor the options on index futures that are listed for trading at another futures exchange are eligible for use as related positions.

(4) EFRPs in CME Group Equity Index Futures Products

EFRPs account for a slender share of contract trading volume among the Exchange’s equity index futures products9 -- lately just over 0.8 percent of the total, with around 0.6 percent in EFPs and the remainder, roughly 0.2 percent, in EFRs. The relative predominance of EFPs to EFRs is unsurprising, insofar as it broadly resembles the proportions of the corresponding adjacent physical markets.10

As the discussion in Section (3) suggests, the decision whether to trade a futures contract via a privately negotiated, non-competitive EFRP transaction hinges, among other things, upon the parties’ assessment of the liquidity available in the contract’s centralized competitive market. This is supported by the evidence in Exhibits 3 and 4, which summarize the gross characteristics of EFP markets and EFR markets, respectively, during the interval from third Friday of June 2017 to third Friday of June 2018 .11 Generally, the deeper and broader the liquidity pool, the lower is the profile of EFRP activity in that liquidity pool. But the data reveal exceptions that lend useful perspective upon this point.

Exhibit 3 – CME Group Equity Index Futures: EFP Trading Activity, 19 June 2017 -- 14 June 2018

| Equity Index Product | Total Volume (Contracts/Yr) | EFP Volume (Contracts/Yr) | EFP Volume (Pct of Total) | EFP Trades per Year | Average EFP Trade Size (Contracts) |

| E-mini S&P 500 | 390,138,559 | 1,180,084 | 0.3 | 962 | 1,227 |

| E-mini NASDAQ 100 | 92,944,977 | 738,621 | 0.8 | 2,588 | 285 |

| CBOT E-mini DJIA | 45,938,954 | 135,132 | 0.3 | 460 | 294 |

| E-mini Russell 2000 | 27,109,612 | 511,959 | 1.9 | 1,714 | 299 |

| Nikkei Stock Average | 10,846,355 | 4,728 | 0.0 | 5 | 946 |

| E-mini S&P MidCap 400 | 4,407,525 | 64,059 | 1.5 | 509 | 126 |

| S&P 500 | 1,366,506 | 627,925 | 46.0 | 5,672 | 111 |

| CBOT DJ Real Estate | 487,845 | 51,878 | 10.6 | 317 | 164 |

| S&P 500 Annual Dividend | 215,118 | 550 | 0.3 | 70 | 8 |

| S&P 500 Total Return | 193,414 | 7,498 | 3.9 | 1 | 7,498 |

| E-mini Russell 1000 Value | 186,203 | 5,447 | 2.9 | 57 | 96 |

| E-mini Russell 1000 | 150,083 | 2,042 | 1.4 | 41 | 50 |

| E-mini Russell 1000 Growth | 115,302 | 2,470 | 2.1 | 35 | 71 |

| E-mini S&P Select Sector | |||||

| Financials | 521,750 | 28,704 | 5.5 | 259 | 111 |

| Utilities | 416,124 | 22,651 | 5.4 | 198 | 114 |

| Energy | 308,648 | 22,876 | 7.4 | 229 | 100 |

| Consumer Staples | 278,942 | 17,601 | 6.3 | 137 | 128 |

| Technology | 240,673 | 17,838 | 7.4 | 129 | 138 |

| Healthcare | 178,977 | 10,987 | 6.1 | 159 | 69 |

| Consumer Discretionary | 157,031 | 14,627 | 9.3 | 158 | 93 |

| Industrials | 143,345 | 22,603 | 15.8 | 188 | 120 |

| Materials | 121,683 | 16,270 | 13.4 | 156 | 104 |

| Real Estate | 99,087 | 9,488 | 9.6 | 52 | 182 |

| All E-mini S&P Select Sector | 2,466,260 | 183,645 | 7.4 | 1,665 | 110 |

Source: CME Group

Among the deepest and broadest liquidity pools at the core of the Exchange’s equity index futures offerings (Exhibit 3, upper panel, and Exhibit 4, upper panel) --

- EFR traffic represents a tiny share, ranging from 0.3 percent for ES futures to near zero for each of E-mini NASDAQ 100 Index ® (NQ) futures and CBOT E-Mini Dow Jones Industrial Average SM Index (YM) futures.

- Similarly, EFPs account for a small share of total trading volumes, from 1.9 pct for E-mini Russell 2000 ® Index (RTY) futures down to 4/100 ths of one pct in Nikkei Stock Average (NIY) futures.

- Despite this, the incidence of EFP activity in these products is impressively high. In ES futures and NQ futures, for instance, EFP trades occur at the rate of roughly 4 per day (962 per year) and 10 per day (2,588 per year), respectively.

Exhibit 4 – CME Group Equity Index Futures: EFR Trading Activity, 19 June 2017 -- 14 June 2018

| Total Volume (Contracts/Yr) | EFR Volume (Contracts/Yr) | EFR Volume (Pct of Total) | EFR Trades per Year | Average EFR Trade Size (Contracts) | |

| E-mini S&P 500 | 390,138,559 | 1,205,724 | 0.31 | 307 | 3,927 |

| E-mini NASDAQ 100 | 92,944,977 | 2,210 | 0.00 | 6 | 368 |

| CBOT E-mini DJIA | 45,938,954 | 538 | 0.00 | 2 | 269 |

| E-mini Russell 2000 | 27,109,612 | 4,071 | 0.02 | 8 | 509 |

| Nikkei Stock Average | 10,846,355 | 1,205 | 0.01 | 2 | 603 |

| S&P 500 | 1,366,506 | 53,501 | 3.92 | 21 | 2,548 |

| E-mini S&P Technology Select Sector | 240,673 | 213 | 0.09 | 1 | 213 |

| S&P 500 Annual Dividend | 215,118 | 100 | 0.05 | 20 | 5 |

| S&P 500 Total Return | 193,414 | 28,528 | 14.75 | 7 | 4,075 |

Source: CME Group

Among other liquidity pools orbiting those at the core, the only clear conclusion one can draw is that the profile of EFRP activity varies widely (Exhibit 3, middle panel, and Exhibit 4, bottom panel) --

- The long-established SP futures market exemplifies one extreme. EFRPs play a far more prominent rôle here than in any of the Exchange’s other equity index futures products, accounting for nearly half of all SP trading volume (46.0 pct in EFPs, 3.9 pct in EFRs).

The frequency of EFPs in SP is likewise far greater than in any other Exchange equity index futures product, exceeding 22 per day (5,672 per year).

EFRs occur in SP much less frequently, roughly once every two to three weeks. But when they do happen, they are massive: On average, more than 2,500 SP contracts are exchanged in each EFR against OTC S&P 500 Index swaps. - Another standout is S&P 500 Total Return Index (TRI) futures. TRI is second only to SP in terms of relative volume of EFRP activity, which accounts for nearly 19 pct of its total trade volume. But TRI contrasts sharply with SP in emphasis: Of that 19 pct, EFPs account for just 3.9 pct, while EFR activity represents 14.75 pct, a reflection of market participants’ abiding preference for OTC swaps as the vehicle for transfer and risk management of S&P 500 Total Return Index exposures.

TRI also differs dramatically from SP in frequency of EFRP trades. In the year we observe, only eight occurred. Similar to EFR transactions in SP, however, size matters: Of the 7 EFRs executed in TRI, the average was nearly 4,100 contracts; the sole EFP trade weighed in at a colossal 7,498 contracts. - S&P 500 ® Annual Dividend Index (SDA) futures occupy a different extreme altogether. Here, EFRPs account for a scant 0.3 percent of total trading volume (with slightly more than ¼ of one percent in EFPs and 5/100 ths of one percent in EFRs). Frequency of occurrence is low, at around two per week (90 per year, comprising 70 EFPs and 20 EFRs). So is the average EFRP trade size (eight contracts per EFP, five contracts per EFR). This combination of features suggests that SDA futures users prize the EFRP mechanism as a means for ensuring close precision of risk management of S&P 500 ® Annual Dividend Index exposures.

A final example, drawn from midway among the Exchange’s non-core liquidity pools, is the E-mini S&P Select SectorTM Stock Index (XA) futures suite (Exhibit 3, bottom panel), originally introduced in March 2011. The 10 products now comprised within the XA suite have seen their underlying liquidity pools grow significantly over time. During the period we observe, aggregate trading volume exceeds 9,750 contracts per day (around 2.5 million per year).

An exceptional feature of EFP activity in the XA products is the consistency of its profile. Irrespective of the measure of comparison, each member of the XA suite bears remarkably close resemblance to the other nine12 -

- EFP trading volume: For the average XA product, the rate of EFP traffic is centered on 18,400 contracts per year, with individual products ranging narrowly from 28,700 contracts per year (E-mini Financials Select Sector (XAF) futures) to around 9,500 contracts per year (E-mini Real Estate Select Sector (XAR) futures).

- EFP volume as percent of total trading volume: Values of this measure cluster tightly around an average of 7.4 pct, ranging from 15.8 pct (E-mini Industrial Select Sector (XAI) futures) to 5.4 pct (E-mini Utilities Select Sector (XAU) futures).

- Frequency of EFP transactions ranges from 259 per year (XAF) to 52 per year (XAR), with all values centered tightly around an average of 166 trades per year.

- Average EFP size is likewise bound by a narrow range, with values spanning from 182 contracts per trade (XAR) to 69 contracts per trade (E-mini Healthcare Select Sector (XAV) futures), all centered on an average trade size of 110 contracts.

Contact Us

Lori Aldinger

+1 312 930 2337

lori.aldinger@cmegroup.com

Richard Co

+1 312 930 3227

richard.co@cmegroup.com

References

1. For EFRP trades involving futures or option contracts listed on the CME Group Exchanges, the authoritative reference is the CME Group Market Regulation Advisory Notice (MRAN) entitled Exchange for Related Positions, available at: https://www.cmegroup.com/rulebook/files/cme-group-Rule-538.pdf.

2. In Exhibit 1 and elsewhere, we use “futures” or “futures leg” as shorthand reference for either the Exchange-listed futures component of an EFP or EFR or the Exchange-listed option component of an EOO. Similarly, we use “cash” or “cash leg” or “related position” when referring to the physical, cash-market asset position in an EFP, or the OTC derivative position in an EFR, or the OTC option position in an EOO.

3. What’s permissible as an offsetting position may change from time to time, at the sole discretion of the Exchange. The roster quoted here is as set forth in CME Group Market Regulation Advisory Notice RA1716-5R, Exchange for Related Positions, 21 February 2018.

4. For information on various means of registration for access to CME Direct, visit: http://www.cmegroup.com/trading/cme-direct/registration.html#newFirmUserRegistration For general information about CME Direct, please visit: http://www.cmegroup.com/trading/cme-direct.htm

Information on means of registration for access to CME ClearPort is available at: http://www.cmegroup.com/clearport/registration.html For general information about CME ClearPort, please visit: http://www.cmegroup.com/clearport.html

5. See US Commodity Exchange Act Core Principle 9 for Designated Contract Markets (17 USC 38.500):

The board of trade shall provide a competitive, open, and efficient market and mechanism for executing transactions that protects the price discovery process of trading in the centralized market of the board of trade. The rules of the board of trade may authorize, for bona fide business purposes:

1. Transfer trades or office trades;

2. An exchange of:

1. Futures in connection with a cash commodity transaction;

2. Futures for cash commodities; or

3. Futures for swaps; or

3. A futures commission merchant, acting as principal or agent, to enter into or confirm the execution of a contract for the purchase or sale of a commodity for future delivery if the contract is reported, recorded, or cleared in accordance with the rules of the contract market or a derivatives clearing organization.

6. See 17 CFR 1.38 (“Execution of transactions”):

1. Competitive execution required; exceptions. All purchases and sales of any commodity for future delivery, and of any commodity option, on or subject to the rules of a contract market shall be executed openly and competitively by open outcry or posting of bids and offers or by other equally open and competitive methods, in the trading pit or ring or similar place provided by the contract market, during the regular hours prescribed by the contract market for trading in such commodity or commodity option: Provided, however, That this requirement shall not apply to transactions which are executed non-competitively in accordance with written rules of the contract market which have been submitted to and approved by the Commission, specifically providing for the non-competitive execution of such transactions. 2. Noncompetitive trades; exchange of futures, etc.; requirements. Every person handling, executing, clearing, or carrying trades, transactions or positions which are not competitively executed, including transfer trades or office trades, or trades involving the exchange of futures for cash commodities or the exchange of futures in connection with cash commodity transactions, shall identify and mark by appropriate symbol or designation all such transactions or contracts and all orders, records, and memoranda pertaining thereto.

7. For a more extensive roster of the functions that EFRPs serve, see Division of Trading and Markets, Report on Exchanges of Futures for Physicals, pp 17-20 and pp 253-6, Commodity Futures Trading Commission, 1 October 1987, and see CME Group, Understanding EFRP Transactions, 1 November 2017, available at: http://www.cmegroup.com/education/understanding-efrp-transactions.html

8. The EFP mechanism for futures is broadly analogous to the creation/redemption mechanism for ETFs, despite differences in their operational detail and their regulatory frameworks. Each enables a riskless conversion from one tool for index tracking to another. In the inventory management example above, even if the upshift in market demand is specifically for the ETF’s component shares, the broker/dealer can still benefit from a futures EFP executed against the ETF, because the ETF can be redeemed subsequently through the issuer in exchange for its underlying shares.

9. All futures products shown in Exhibits 3 and 4 are listed for trading on the CME designated contract market, with the exceptions of E-mini Dow Jones Industrial Average SM Index futures and Dow Jones US Real Estate Index futures, which are listed for trading on the CBOT designated contract market.

10. At 2017 year-end, for example, US equity market capitalization was $27.776 trln (Wilshire 5000 Price Full Cap Index, Federal Reserve Bank of St Louis, FRED Economic Data, available at https://fred.stlouisfed.org/), whereas the notional principal amount outstanding of OTC US-equity-linked derivatives was an order of magnitude smaller, at $2.923 trln (BIS, OTC derivatives outstanding, 3 May 2018, available at https://www.bis.org/statistics/derstats.htm?m=6%7C32%7C71).

11. Ie, from (and including) final settlement of June 2017 futures to (and not including) final settlement of June 2018 futures.

12. Following architect Louis Sullivan’s axiom, “form follows function”, EFRP activity in CME S&P Select Sector Stock Index futures appears to exemplify the corollary that “unity of form follows unity of function.”