{kind=link}

COMEX Gold Futures and Options: A Look at APAC Liquidity

It is safe to say that global financial markets have had an eventful start to the year. Investors re-assessed the risks that the coronavirus could pose to the global economy. News of contagion beyond China’s borders led to a flight to safety. Treasury yields collapsed to record low levels, and stock markets suffered a severe sell-off. The last week of February saw equities decline by the largest amount since 2008. In another way, the current situation is also reminiscent of 2008: global leaders are coming together to coordinate a joint response to the threat. Meanwhile, gold was on many investors’ minds and heavily traded, possibly reflecting the precious metal’s function both as a safe-haven asset in times of market turmoil and as a product to hold when yields are low. How did APAC liquidity develop during the past months and how does it compare to other periods of high market activity? In addition, how does cost of trading during Asian hours compare to the rest of the trading day?

Gold futures and options – a secular trend towards higher liquidity in APAC hours

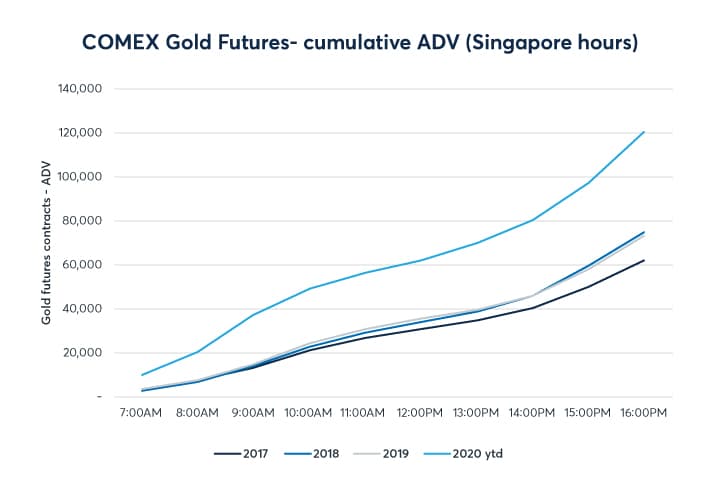

APAC activity has expanded its footprint on COMEX Gold trading. Trading volumes are growing during APAC hours, both on an absolute (how many contracts are traded in Asian markets) and on a relative basis (how much of total contracts traded were done in Asian hours). GC futures volume by Singapore midday now runs at 60,000 contracts ADV, and more than 100,000 contracts are typically exchanged by late afternoon – a notable increase versus prior years. In aggregate, ADV in GC futures contracts amounts to above 400,000 contracts, a 30% increase versus 2019 ADV figures.

{kind=link}

Source: CME Group, 2020 ytd includes data up to and including Feb 28th, 2020.

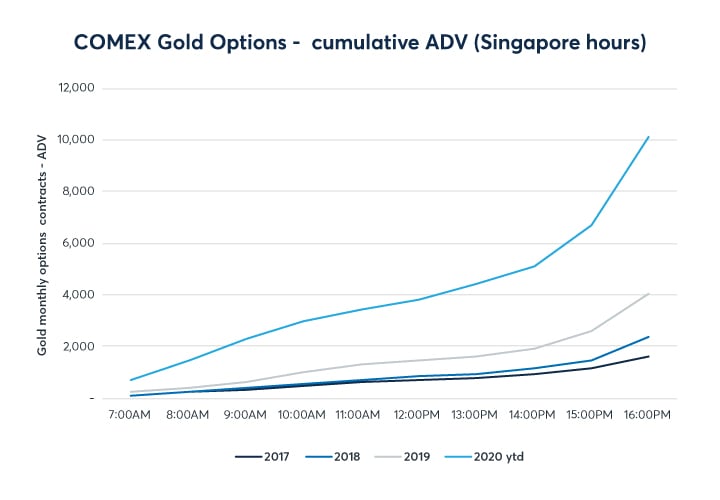

Growth in OG option liquidity is even stronger, albeit from a lower starting point. On average, 10,000 option contracts change hands by 16:00 hours SGP local time, a more than five-fold increase compared to 2017. Globally, ADV in OG options now runs at 85,000 contracts, 40% above 2019 numbers.

{kind=link}

Source: CME Group, 2020 ytd includes data up to and including Feb 28th, 2020.

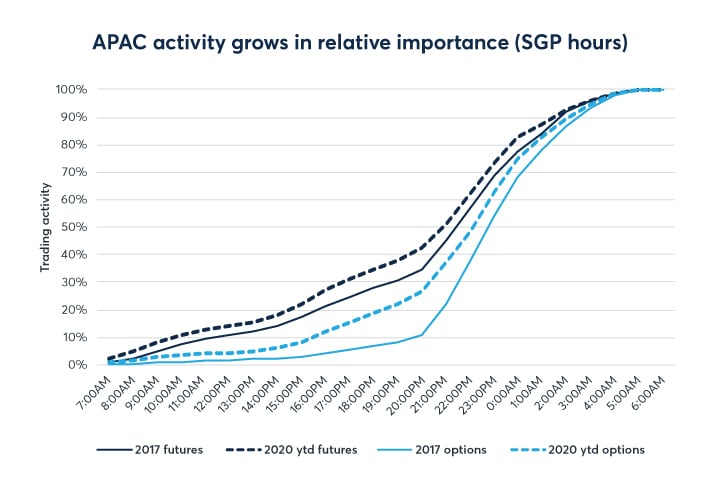

A look at the volume done in Asian hours as a percentage of total trading reveals an increase in the relative importance of APAC market activity. Trading is shifting to accommodate more volume outside of core U.S. market hours. This applies to both GC futures and OG options. This change in market structure is most pronounced in options market: in 2017, less than 10% of total OG trading was done prior to 19:00 hours Singapore time. In 2020 year-to-date, one quarter of total trading was done by that cut-off time. For futures, the figure is 31% for 2017, increasing to 38% year-to-date in 2020. The 50% percentile – or the time of day by which half of total daily trading is done - is moving to an earlier hour of the day, or, put in another way, moving closer to an Asian time zone.

{kind=link}

Source: CME Group, 2020 ytd includes data up to and including Feb 28th, 2020.

APAC liquidity in periods of high market activity

Focusing on single trading days with significant market activity also demonstrates how APAC market liquidity has advanced compared to earlier events. Below tables shows the share of futures volume done during Asian hours for selected days with high turnover.

| Singapore volume | ||||||

| Date | Event | Total Volume traded (contracts) | morning (7:00-12:00) | afternoon (12:00-18:00) | sum (7:00-18:00) | % of total volume |

| 08/24/2011 | Gold tops $1,900 | 483,429 | 27,049 | 33,244 | 60,293 | 12% |

| 04/15/2013 | Gold collapses below $1,500 | 751,058 | 97,365 | 96,371 | 193,736 | 26% |

| 06/24/2016 | UK votes for Brexit | 628,549 | 130,536 | 239,123 | 369,659 | 59% |

| 11/09/2016 | U.S. elects Trump | 897,219 | 270,660 | 304,285 | 574,945 | 64% |

| 01/08/2020 | Gold tops $1,600 | 886,139 | 280,235 | 129,215 | 409,450 | 46% |

| 02/28/2020 | Coronavirus sell-off | 831,427 | 69,745 | 194,564 | 264,309 | 32% |

Costs of execution – how does Asia compare to the rest of day?

Market microstructure data reveals that GC trading costs during Asian market hours are on a comparable level to those observed during the entire trading day. The analysis is focused on the actively traded GC contract (GCJ0 contract – April 2020 expiry) during the month of February and compares activity during the Singapore morning (7:00 to 12:00) to the average across the trading day. By focusing on the Asian morning, the analysis excludes the effects that changes in London activity may have on market liquidity.

The top-of-book bid/ask spread width and depth show that levels during the Singapore morning compare well to the average during the entire day, both at top-of-book and at deeper levels. The bid/ask spread is nearly identical, and the book depth is comparable to the average across the day (89 contracts depth in Singapore morning versus an average of 103 when including the top 5 order-book levels).

| Order book depth (contracts) | Singapore morning | Entire trading day | SGP morning vs. average |

| Depth 1 | 10 | 12 | -15% |

| Depth 2 | 18 | 21 | -14% |

| Depth 3 | 19 | 22 | -14% |

| Depth 4 | 20 | 24 | -15% |

| Depth 5 | 21 | 24 | -13% |

| Cumulative depth | 89 | 103 | -14% |

| Spread (ticks) | Singapore morning | Entire trading day | SGP morning vs. average |

| Spread 1 | 1.15 | 1.10 | 4% |

| Spread 2 | 2.00 | 2.00 | 0% |

| Spread 3 | 2.00 | 2.00 | 0% |

| Spread 4 | 2.00 | 2.00 | 0% |

| Spread 5 | 2.00 | 2.00 | 0% |

| Cumulative width | 9.16 | 9.11 | 1% |

Source: CME Group data for GCJ0 during Singapore morning (7:00-12:00 hours) in February 2020

Attractive liquidity levels during the Asian morning translate into low execution costs during that time frame. Measured in ticks, median costs to a trader aggressing the order book stands at 2.3 ticks to execute 25 contracts and 3.6 ticks to do 50 contracts. This compares well to the average across the day, which is only slightly tighter at 2.1 and 3.2 ticks for the same trades. Smaller clip sizes of 5 or 10 contracts can be executed at the same median costs of 1.1 ticks.

Conclusion

The long-term effects of the coronavirus on the global economy are very unclear. With many factors in play, the market environment remains highly challenging and investors may turn to gold to express their views. Traders based in Asia are benefiting from a trend towards higher liquidity in COMEX Gold futures and options during their core market hours. Execution costs are comparable to those observed during the rest of day. The volume growth in Asian hours reflects a secular long-term shift in market structure, but it also applies to single days with high market stress – as witnessed during high volume days this year. Liquidity in Asian hours is at unmatched levels for COMEX Gold, offering opportunities to the Asia-based trading community.