{kind=link}

CME Group’s Wheat Futures Lead Price Discovery of the Global Wheat Market

- CME Group launches new Wheat contracts

- Changing global dynamics reflected in Wheat derivative volumes

- Inter-commodity Wheat futures correlations and differentials

- CME Group Wheat hedge effectiveness

Introduction

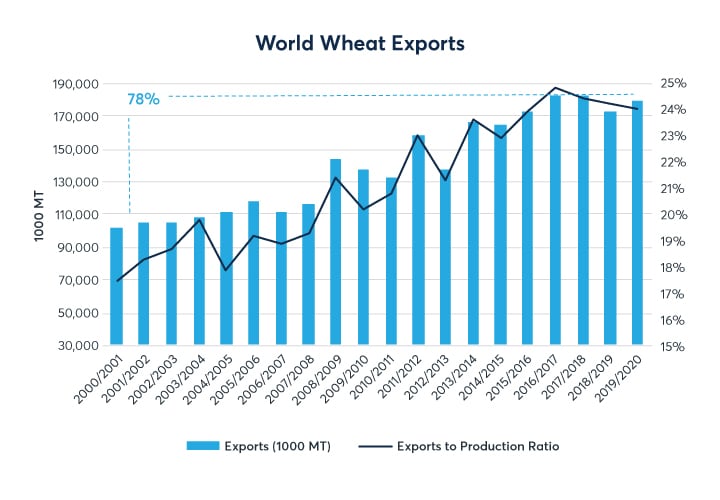

As world populations and per capita income have risen, global wheat exports have grown rapidly to support that growth. According to USDA data, over the past two decades world wheat exports have increased almost 80 percent with a 3 percent compounded annual growth rate. In comparison, world population and wheat production have grown roughly in proportion to each other experiencing only a 30 percent increase and 1.3 percent compounded annual growth rate.1 What is driving this surge in wheat exports and global trade? And how can market participants hedge this exposure?

Exhibit.1 World Wheat Exports and Export to Production Ratio Growth

{kind=link}

| 2000-2019 | Wheat Exports | Wheat Production | World Population |

| Compounded Annual Growth Rate | 3.07% | 1.44% | 1.20% |

| 20-Year Increase | 78% | 31% | 26% |

Source: USDA

CME Group launches Black Sea Wheat and Australian Wheat

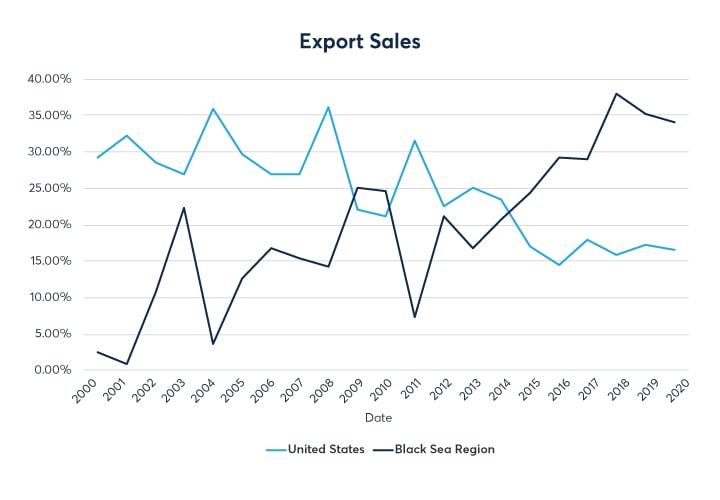

In the past two decades major global commodity export markets and production have undergone a shift towards regionalization as new centers of production emerge. The wheat export market is no exception. Once the dominating presence, the U.S.’s export market share has decreased significantly from 29 to 15 percent since the trade year 2000.2 Today, the Black Sea Region (BSR) has emerged as the dominant world wheat export market, supplying the world with high quality and competitively priced grain. Driven by production in Russia and Ukraine, the BSR accounts for close to 35 percent of world wheat export market share as seen from the Exhibit.2. Russian soft wheat, the most popular varietal from the region, has the benefit of broad-spectrum use in baking and can be used for a wide assortment of breads, cookies, flatbreads, as well as blending with other types of wheat. This broad-spectrum utility combined with large supplies, competitive pricing, and geographic proximity to the major wheat import markets of North Africa, the Middle East and Asia, has led this region to become the world’s top supplier of wheat.

With a growing need for region specific risk management tools, CME Group has responded to this trend by launching financially settled Black Sea Wheat (Platts) and Australian Wheat (Platts) derivative contracts alongside the legacy wheat products of the Chicago Board of Trade (CBOT) and Kansas City Board of Trade (KCBT). These new contracts, combined with CME’s best-in-class liquidity, can help market participants to effectively manage risk and effectuate price discovery in real-time in a manner that reflects the dynamics of today’s global trade.

Exhibit.2 Export Sales Market Share U.S. vs Black Sea Region (Ukraine and Russia)

{kind=link}

Source: USDA

Changing global dynamics reflected in launching new futures contracts

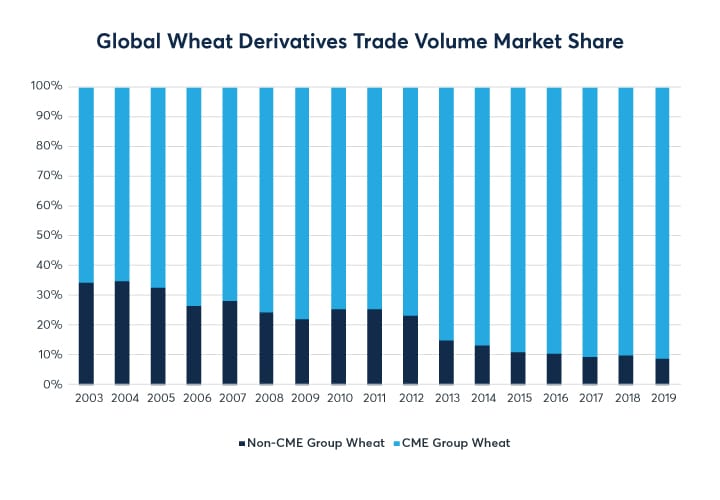

Since it began trading in 1877, Chicago Soft Red Winter Wheat futures (Chicago Wheat) remains the preeminent benchmark for pricing and hedging cash wheat around the world. Today, Chicago Wheat accounts for 62 percent of total wheat derivatives traded globally; this is down from 78 percent a decade ago. Representing the third largest wheat variety in the U.S., soft red winter (SRW), which is mainly grown in 25 states east of the Mississippi River and is commonly used for producing flat breads, cakes, cookies, snack foods, and pastries.

Over 140 years old and today accounting over 27 percent of global wheat derivatives trading, Kansas City Hard Red Winter Wheat (KC Wheat) is the second largest wheat derivatives contract by trading volume and has seen year-over-year growth since being acquired by the CME Group in 2012. Representing the largest U.S. wheat variety, hard red wheat (HRW) is the primary ingredient in the production of bread.

Launched in December 2017 as a price risk management tool for exports of BSR Wheat, CME Group’s Financially Settled Black Sea Wheat FOB (Platts) futures (Black Sea Wheat) and options have seen quick adoption as a hedging tool and trading instrument by a wide range of market participants, including producers, exporters, trading houses, and processors in Europe, the US, Middle East and Asia. By 2019, Black Sea Wheat futures average daily volume reached 600 lots along with 200 lots in options. This is the equivalent to 40,000 metric tons of wheat traded daily, with no defaults and minimal counterparty risk.

Australian Wheat (Platts) futures (Australian Wheat) were launched in June of 2017 to provide regional price discovery in the key Australian wheat export market. Wheat is a major winter crop grown in Australia, the majority of which is sold overseas to Asian and Middle Eastern markets.

Although the traditional Chicago Wheat market share has declined, trade volume across all CME Group wheat markets has increased to account for over 90% of the today’s total wheat derivative trade volume. This comparison includes Non-CME Group exchanges, including Minneapolis Grain Exchange, Euronext, MATba (Mercado a Termino de Buenos Aires), and the Australia Securities Exchange.

Exhibit.3 Futures Trade Volume Market Share 3

{kind=link}

Sources: Bloomberg and CME Group

The Strong Gluten Wheat contracts traded at China’s Zhengzhou Commodity Exchange (ZCE) has one of largest trading volumes among global wheat futures markets; however, it has limited global price influence because of ZCE’s restrictions on the foreign capital. If this situation were to change, the contract’s strong liquidity could propel it to become another global wheat benchmark.

Inter-commodity futures spread correlations and differentials

Using New Crop/Old Crop futures price series, the correlations amongst Chicago Wheat (ZW), KC Wheat (KE), Black Sea Wheat (BWF) and Australian Wheat (AUW) futures contracts are shown in Exhibit 4. The Chicago Wheat contract’s price series has moderate correlations with KC Wheat’s series (0.67) and Black Sea Wheat (0.66). Given efficient and effective price discovery is a function of market liquidity (i.e. the volume and frequency of trades per number of active market participants) these moderate correlations suggest that Chicago Wheat should be given serious consideration as a component in hedging strategies for the underlying commodities of KC Wheat and Black Sea Wheat due to the contract’s strong liquidity profile. From a trader’s perspective, this also suggests there may arise unique periodic arbitrage opportunities between these three contracts.

While uncommon but not unprecedented, since the beginning of 2019, Chicago Wheat has held a substantial premium over the KC Wheat contract. This year’s poorer weather conditions in Illinois, Indiana, Ohio, and Michigan (SRW’s main growing areas) have contributed to supply side concerns relative to HRW, resulting in a higher premium for the crop.

Exhibit.4 CME Group Wheat Products Price Series New Crop/Old Crop4

{kind=link}

| Chicago Wheat | KC Wheat | Black Sea Wheat | Australian Wheat | |

| Chicago Wheat | 1.00 | |||

| KC Wheat | 0.67 | 1.00 | ||

| Black Sea Wheat | 0.66 | 0.55 | 1.00 | |

| Australian Wheat | 0.42 | 0.51 | 0.58 | 1.00 |

Sources: CME Group

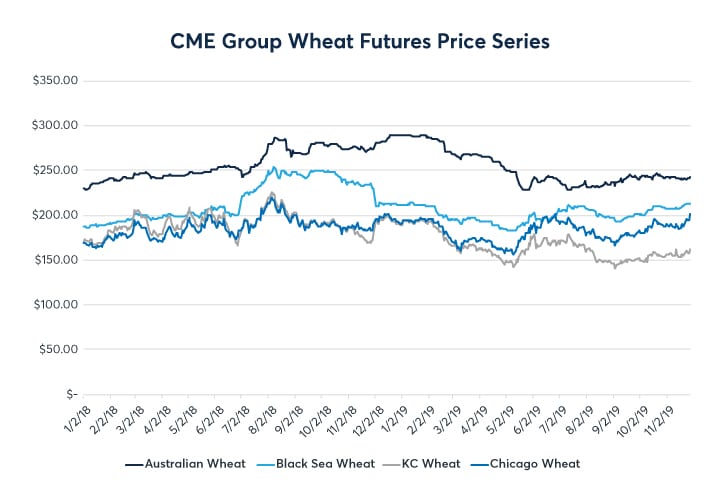

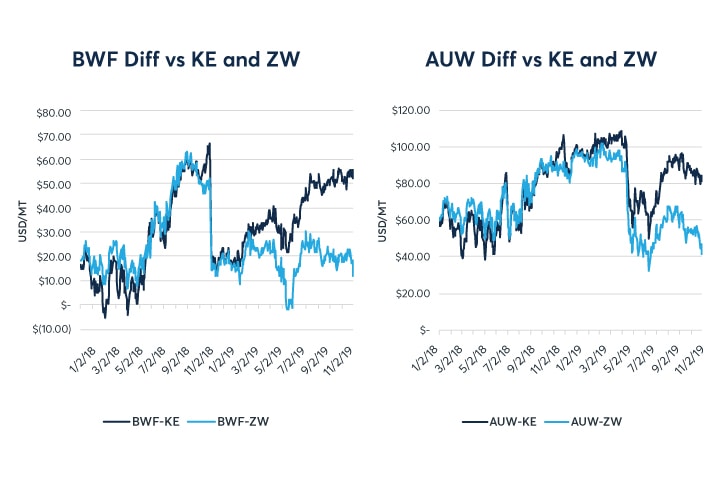

Since 2018, Black Sea Wheat futures has averaged a $25 per metric ton premium to Chicago Wheat and a $32 per metric ton premium to the KC Wheat as shown in Exhibit 5. Black Sea Wheat futures reflects Russia 12.5% protein FOB wheat price at the deep-water port of Novorossiysk on the Black Sea. The Black Sea is the main export corridor for wheat from Russia, Ukraine, and Kazakhstan. From 2000 to 2018, these three countries’ combined market share of world wheat exports increased from 5 to 35 percent according to USDA data.

The Australian Wheat contract reflects the FOB price of western or southern Australian Premium White wheat, the majority of which is exported to overseas Asian and Middle Eastern markets. Since 2018, Australian Wheat has averaged a $71 per metric ton premium to Chicago Wheat and a $78 per metric ton premium to KC Wheat as shown in Exhibit 5. Drier-than-average weather conditions over the past year have had a decimating impact to Australia’s wheat crops, leading to lower stocks and poor harvest conditions. These circumstances have elevated Australia’s FOB wheat export prices and limited the competitiveness of their exports.5

Exhibit.5 Black Sea and Australian Wheat Differentials vs. Chicago and KC

{kind=link}

Sources: CME Group

Hedge effectiveness 6

In this section, we investigate how the different CME Group Wheat futures prices perform as hedge instruments against movements in cash prices in the wheat production and export regions around the world. Hedge effectiveness, represented by the R-square between two price series, is the variation in cash commodity price explained by the futures price, or more simply, how much price risk is diminished when using a futures contract to hedge against movements in cash prices.7 A hedge effectiveness of 1.0 would be a perfect hedge, while a figure above 0.75 represents an effective hedge.

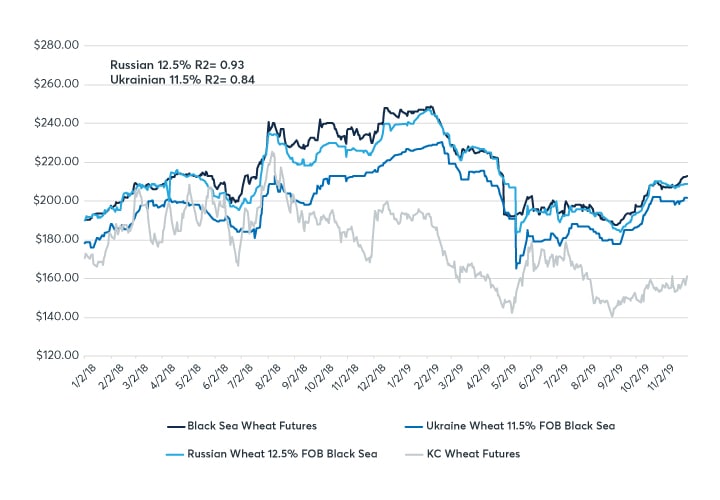

There is little surprise looking at the hedging performance of Black Sea Wheat and Australian Wheat futures for their respective markets. Black Sea Wheat futures can be a highly effective hedge for FOB Black Sea wheat cash markets, with hedge effectiveness equal to 0.93 for Russian 12.5% protein wheat and 0.84 for Ukrainian 11.5% protein wheat. With an average daily trade volume equivalent to 30,000 metric tons of wheat, Black Sea Wheat represents an effective and liquid hedging tool for price risk in the region.

Exhibit.6 Black Sea Wheat vs. Russia and Ukraine FOB Prices

{kind=link}

Sources: Bloomberg and CME Group

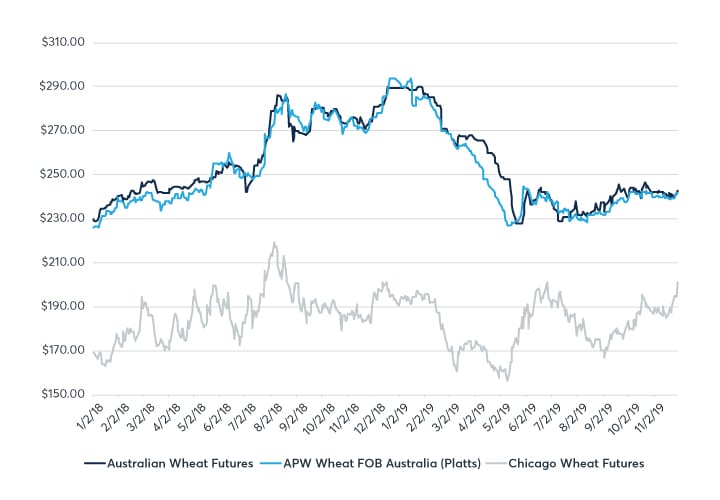

In the Australian wheat export market, Australian Wheat futures can be an effective hedging tool for FOB Kwinana, Western Australia (0.94). While the futures contract predominantly represents the Western Australia APW export market, it tracks well with other major export Australian export regions with an R-Square averaging 0.84. Since other grades of milling wheat are normalized APW, this suggests the contract can be a suitable hedging vehicle and proxy for most of the Australian wheat export market as shown in Exhibit.7.

Exhibit. 7 Australian Wheat Hedge Effectiveness

{kind=link}

| Australian FOB Cash Wheat Export | Hedge Effectiveness (R2) |

| APW Wheat FOB Australia (Platts assessment) | 0.97 |

| Individual Cash Prices (July 2017 - July 2019) | |

| APW1 Indicative Pt Kembla NSW | 0.86 |

| APW1 Indicative Geelong VIC | 0.86 |

| ASW1 Indicative Kwinana WA | 0.82 |

| APW1 Indicative Portland VIC | 0.87 |

| APW1 Indicative Newcastle NSW | 0.81 |

| Average | 0.84 |

Sources: Platts and Bloomberg

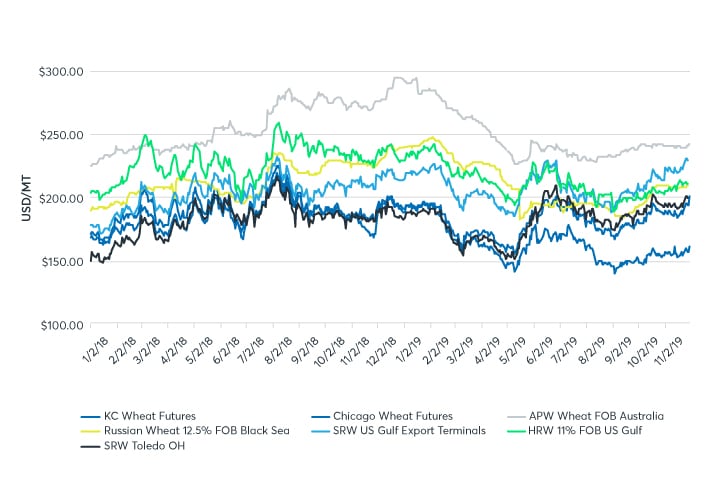

Exhibit.8 demonstrates the hedge effectiveness of the legacy Chicago Wheat futures versus international FOB wheat cash prices in Russia, Australia, and the U.S. Gulf export and domestic markets (Toledo, Ohio). As expected, both legacy contracts perform well as price risk management tools for US export and domestic exposure but are much less effective for the FOB Black Sea and Australian Wheat markets. KC Wheat has a hedge effectiveness of 0.76 for US Gulf HRW FOB, while Chicago Wheat has a hedge effectiveness of 0.66 for SRW FOB US Gulf and 0.81 for SRW Toledo OH (domestic).

Exhibit.8 Chicago Wheat and KC Wheat Futures vs Russia, Australia, US Gulf FOB Wheat Prices

{kind=link}

| R-Squared | FOB Black Sea | APW Wheat FOB Australia | US Gulf FOB HRW | US Gulf FOB SRW | US Toledo, OH SRW |

| Chicago Wheat Futures | 0.14 | 0.27 | 0.46 | 0.66 | 0.81 |

| KC Wheat Futures | 0.24 | 0.31 | 0.76 | 0.10 | 0.16 |

Sources: Platts, Agricensus, USDA, and CME Group

Conclusion

The Black Sea Region’s strengthening role as a global grain export market has had a marked impact on surging global wheat exports and has caused a shift among global wheat price benchmarks. Notwithstanding year-to-year seasonal variability, this impact is expected to continue to grow and have long lasting effects due to a multitude of competitive advantages including production growth factors, infrastructure investment, and proximity to the largest grain importers.8 These developments, alongside best-in-class liquidity and the addition of the Black Sea Wheat (Platts) and Australian Wheat (Platts) derivative contracts, creates a unique opportunity in assisting CME Group market participants to manage risk and effectuate real-time price discovery related to today’s leading global wheat benchmarks.

References

1 FAS USDA

4 New Crop/Old Crop price series combine the July and December futures contract price series with the roll between expirations occurring the first Friday or last trade day prior to spot month.

5 S&P Analysis: Australia Wheat

6 Ordinary least squares (OLS) was used to regress futures prices on cash prices. The results presented in this paper were cointegrated based on Engle-Granger two-step method. Ultimately, using an Augmented Dickey Fuller (ADF) to test for stationarity helped determined price level data could be used. Cointegration of two nonstationary series indicates a non-spurious relationship. If two nonstationary series are cointegrated, OLS regression statistics may be done on price levels and still hold true.

7 Cross Hedge Effectiveness of CME Group Contracts on Agricultural Commodities

8 Russia Port capacities for grain handling to increase by 75% before 2024