{kind=link}

Case Study: Hedging Soymeal Price Risk for Feed Mills in Vietnam

Industry Background

Vietnam has a population of over 90 million people and consumes over 6 million metric tons (MT)1 of soymeal, mostly as animal feed for hogs, the most popular meat consumed in the country.

Vietnam is one of the world’s largest importers of soymeal, importing over 4.3 million MT2 in 2017, 85% of which was from Argentina and the rest mainly from the U.S. and Brazil.

Soymeal production within Vietnam is small, and domestic demand is mostly met by imports. Numerous small- to medium-sized feed mills buy and import most of the soymeal.

Risks Associated with Soymeal Imports

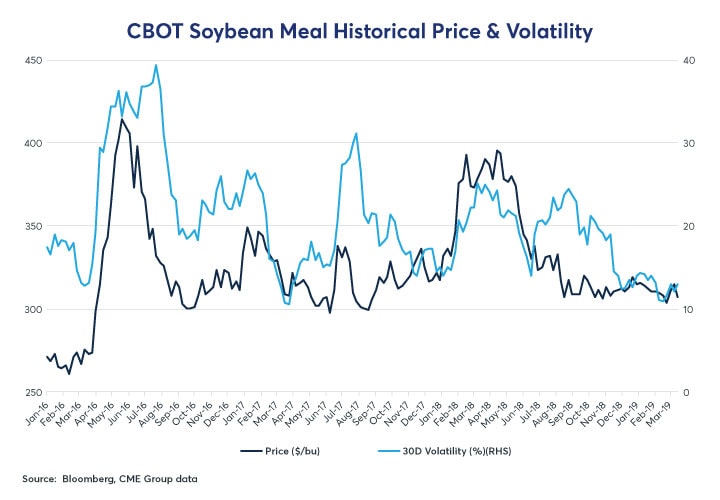

Vietnam is the world’s second biggest soymeal importer (after the EU-27 bloc); the three largest soymeal exporters are Argentina, Brazil and the U.S. The Sino-U.S. trade tariff disagreements that started in April 2018 have had an impact on the global soybean and soymeal trade resulting in the possibility for additional price volatility. Firms involved in importing soymeal into Vietnam may want to consider an active hedge program to guard against unforeseen price volatility.

{kind=link}

Commodities are a volatile asset class. Soymeal prices were relatively calm in the second half of 2018 despite turbulence caused by the Sino-U.S. trade tariff negotiations. Volatility typically increases from May to July when the U.S. soybean planting season gets underway.

When traders buy soymeal from overseas soybean crushers, the cargoes are usually procured as basis contracts where the soymeal is priced against an index such as the CBOT Soybean Meal futures price. The international traders importing soymeal in this manner typically hedge their price risk. The international traders then may sell to local traders, who then on-sell to domestic feed mills either at a fixed price or at a basis to the Soybean Meal futures price.

Vietnam is home to many small feed mills, who buy soymeal from traders either at fixed prices or at a basis. Purchases direct from crushers or international traders are typically conducted in USD while purchases from local traders are typically conducted in Vietnamese Dong (VND).

For purposes of this case study, currency risk is ignored by assuming that the foreign exchange rate between USD and VND is constant. Therefore, for mills buying at a basis, the main price risk is that soymeal prices may rise between the time of the contract and delivery on the contract. For mills buying on fixed prices, the main price risk is the opportunity cost that prices may decline between the time of the contract and delivery on the contract.

Company Profile and Situation

Consider an example company and its situation - Tortilla is a medium sized feed mill which buys soymeal from international and local traders. It buys in small parcels of 2,000 to 5,000 MT at a time, and its purchases can be at fixed prices or at a basis to the CBOT Soybean Meal futures price.

In March, Tortilla placed a purchase order with an international trader for 2,000 MT of soymeal for physical delivery in June. This parcel would be part of a larger 50,000 MT cargo that will be loaded from the Puerto Parana port in Argentina for May shipment, and be delivered to the Phu My-Ba Ria Serece port off Ho Chi Minh City3 in June.

In March, soymeal was quoted at $380 per MT in the Argentinian cash market for May shipment. Tortilla agreed to buy at a fixed price of $390 payable upon delivery in June.

Due to global economic conditions, Argentinian soymeal prices fall by $60 per MT when June arrives. Other feed mills in Vietnam who were actively placing orders for soymeal in June were being quoted $320 per MT, for August shipment. Tortilla wondered if it should have bought on basis instead of at fixed prices.

Tortilla did not open a letter of credit at the time it bought the meal, so the firm may face difficulty getting its cargo financed from banks since banks sometimes refuse to finance cargoes if there is a risk that the customer might fail to repay the loan.

Case Study

The case study considers two alternative scenarios where Tortilla buys at fixed prices or buys at basis and considers risk management strategies that it could have taken to manage price risks that improves on the example above.

Scenario 1 – Tortilla Purchases at Fixed Prices: If Tortilla purchases soymeal at fixed prices, its main risk is the opportunity cost if prices fall significantly. One way that Tortilla could manage this risk is with a put option on the July4 Soybean Meal futures contract. The following table illustrates potential outcomes where soymeal prices rise by $60 and fall by $60 compared to an unhedged position.

| Price per metric ton ($/MT) | Fell by $60 | Rose by $60 |

| March | ||

| Soymeal cash price | 380 | |

| July futures price | 385 | |

| July put option at $380 strike5 | 156 | |

| June | ||

| Soymeal cash price | 320 | 440 |

| July put option at $380 strike | 607 | 0 |

| Hedged with Put Option | ||

| Paid for put in March | - 15 | - 15 |

| Cash flow from exercising Put | +60 | 0 |

| Paid for soymeal in June | - 390 | -390 |

| Net cost of soymeal purchase | -345 | -405 |

| Unhedged Case | - 390 | - 390 |

| June soymeal cash price | - 320 | - 440 |

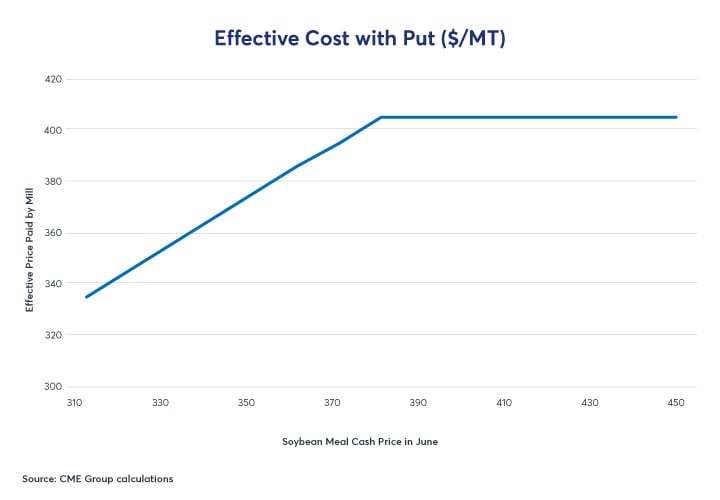

In other words, had soymeal prices fallen to $320, Tortilla would have been able to partially capture the cost savings by exercising the put option, and paid an effective price of $345 instead of the contracted fixed price of $390. Had prices risen, Tortilla’s cost would be fixed at $405 ($15 above the fixed contract price of $390 due to the cost of the put).

The mill cannot be certain whether soymeal prices will increase or decrease, so the fixed premium paid for the put option is like insurance against potentially disastrous price movements.

How Tortilla’s net price paid varied between simply paying the fixed contract price of $390 versus hedging that purchase with put options is illustrated in the charts below. In summary, when hedged, Tortilla pays a small amount more than the fixed contract amount if prices rise but gets to take advantage of a lower effective price paid should prices fall.

https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/2019/case-study-hedging-soymeal-price-risk-for-feed-mills-in-vietnam-fig02.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/2019/case-study-hedging-soymeal-price-risk-for-feed-mills-in-vietnam-fig03.jpg

{kind=link}

{kind=link}

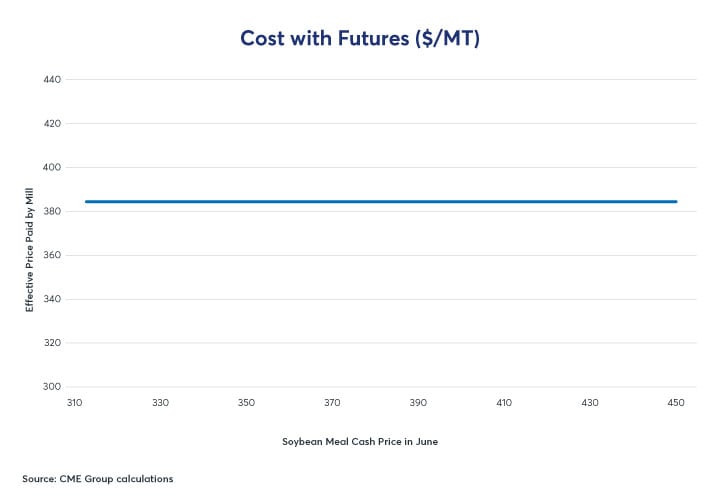

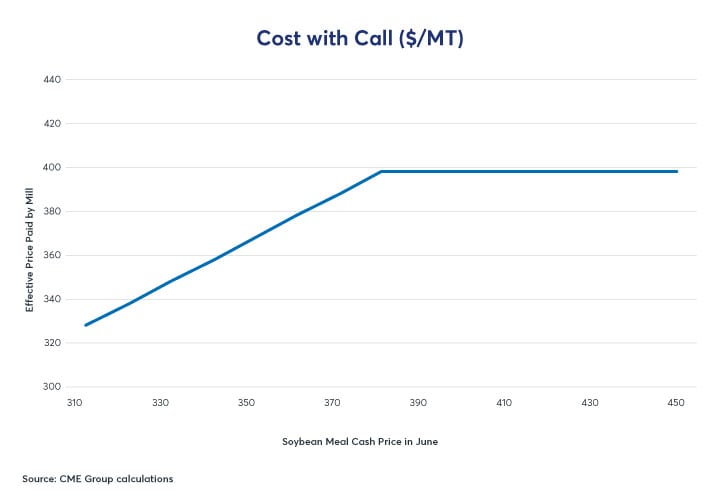

Scenario 2 – Tortilla Purchases on Basis: If Tortilla prices its soymeal parcel as a basis against the Soybean Meal futures price, it can hedge its price risk with either a futures contract or a call option contract. In essence, using a futures contract would effectively allow Tortilla the ability to fix the cost of soymeal, whereas a call option would allow Tortilla the ability to fix the cost of soymeal if soymeal prices rise above a pre-determined price, but allow Tortilla to capture a cost benefit if soymeal prices fall.

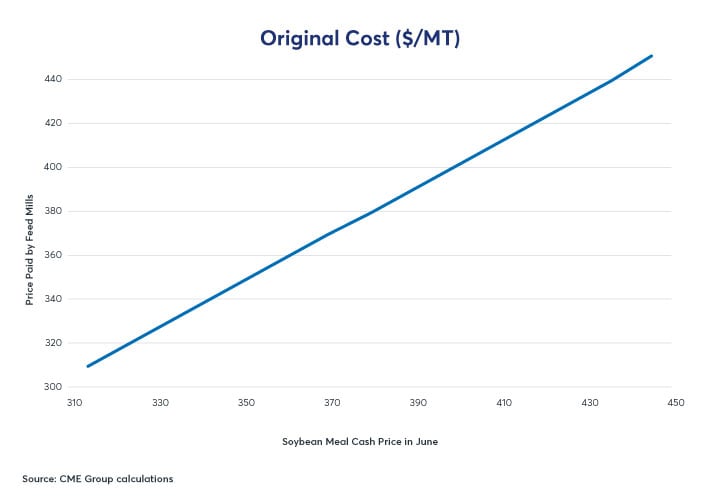

The potential outcomes from these three examples are illustrated in the charts below. The soymeal cash price and the July futures prices are assumed to be $380 and $385 respectively in March. The first chart shows that, if Tortilla does not conduct any hedging, it would be fully exposed to all soymeal price fluctuations.

The second chart shows that, if fully hedged with a futures contract, Tortilla’s purchase price will be fixed regardless of market price fluctuations. The third chart shows that, if hedged with a call option, Tortilla’s purchase price will be fixed if soymeal prices rise but allow it to pay a lower purchase price if soymeal prices fall.

https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/2019/case-study-hedging-soymeal-price-risk-for-feed-mills-in-vietnam-fig04.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/2019/case-study-hedging-soymeal-price-risk-for-feed-mills-in-vietnam-fig05.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/2019/case-study-hedging-soymeal-price-risk-for-feed-mills-in-vietnam-fig06.jpg

{kind=link}

{kind=link}

{kind=link}

This is illustrated numerically in the table below, for the specific cases where soymeal prices rise by $60 or fall by $60.

| Price per metric ton ($/MT) | Fell by $60 | Rose by $60 |

| March | ||

| Soymeal cash price | 380 | |

| July Futures price | 385 | |

| July Call Option at $390 strike8 | 189 | |

| June | ||

| Soymeal cash price | 320 | 440 |

| July Futures price | 320 | 440 |

| July Call Option Exercise Price | 0 | 60 |

| Hedged with Futures | ||

| Opened Futures position in March | - 385 | - 385 |

| Closed Futures position in June | + 320 | + 440 |

| Paid for Soymeal in June | - 320 | - 440 |

| Net Cost of Soymeal | -385 | - 385 |

| Hedged with Call Option | ||

| Paid for Call in March | - 18 | - 18 |

| Cash Flow from Exercising Call | +0 | +5010 |

| Paid for Soymeal in June | - 320 | - 440 |

| Net Cost of Soymeal | - 338 | - 408 |

| Summary: Tortilla’s cost of soymeal | ||

| Unhedged Case | - 320 | - 440 |

| Hedged with Futures | - 385 | - 385 |

| Protected with Call Option | - 338 | - 408 |

Concluding Remarks

Tortilla was likely better off using either Futures or Options to hedge its physical exposure compared to leaving its physical trades unhedged. Commodity derivatives were primarily developed to help commercial market participants manage their commodity price risk.

A firm buying physical commodity on a basis contract can fix its purchase price by buying futures contracts or can manage its purchase price risk by buying call options. A firm buying physical commodity on a fixed price contract can manage its purchase price risk by buying put options.

Questions

- If Tortilla entered into a fixed price contract (per Scenario 1), and soymeal prices decline, could they not simply negotiate prices down with the supplier?

Tortilla could try to reduce the agreed-on price by threatening to cancel the transaction, with the expectation that the supplier would find it uneconomical to take legal action against Tortilla. For example, legal costs might potentially be more than giving a $60 discount to Tortilla; the supplier’s loss on a 2,000 MT package would be $120,000.

However, such actions would damage Tortilla’s reputation, reducing its ability to secure favorable deals in future. - Following on from question 1, could Tortilla further reduce the cost of buying put options?

If Tortilla has built in some profit margin into its purchase costs, it could decide to only buy partial hedge coverage. For example, Tortilla could decide to only hedge half of its physical exposure.

A more common strategy would be to buy a put option with a lower strike price, which provides less protection. In the case study, the futures price in March was $385. Instead of buying a put option with strike price of $380, Tortilla could decide to buy a put option with strike price of, say, $360. This cheaper put option would provide a bit less protection but would cost less than the original $380 put option. - Under fixed price contracts (per Scenario 1), when is it appropriate to use the put strategy and when is it appropriate to leave the exposure unhedged?

It depends on Tortilla’s risk profile and its own macroeconomic view. The economic consideration would measure the cost of the option versus the expected downside price risk. If Tortilla believes that the probability of price decline is small, and/or if it has fixed its downstream sales revenues and its profit margin, it may decide not to buy the option.

However, if the probability of a price decline is significant, Tortilla’s downstream clients might expect Tortilla to reduce its sell prices accordingly. Whenever the potential cost savings are greater than the cost of the option, it might be prudent to utilize options to capture such cost savings so that it can be passed back to the customer if necessary. - The case study has not considered foreign exchange (FX) risks. What are the considerations here?

VND is not a convertible currency, and domestic traders and mills typically manage their FX exposure through their local banks. This adds an additional layer of operations, which is not dealt with in this study.

Some traders and mills might manage their currency risks by adopting a “natural hedge” strategy. This involves matching their cash inflows and outflows in that foreign currency. In practice, the firm would borrow the same amount of foreign currency from the banks as the amount used for their physical contracts.

If the feed mill services mainly the domestic market, and buys its soymeal feed in VND terms, then their physical business may have minimal FX exposure.

Most mills, however, likely have dealings with international traders who allow them to finance their trades using letters of credit. They would therefore have USD accounts with their banks, and be able to trade CBOT Soybean Meal futures and options.

FX risk exposure is more commonly assumed by the trader, who bought from overseas crushers in foreign currencies, paid for shipping and transportation costs in USD, and then sold to local traders or Vietnam feed mills in USD or VND.

More information about FX risk management using FX Futures and Options contracts can be found on the CME Group website.

Sources

- USDA: Vietnam Oilseeds & Products Annual 2018. 1.5 million MT domestic crush, and 4.5 million MT imported.

- Source: UN Comtrade data 2017. According to USDA, Vietnam imported 5 million MT soymeal in 2018.

- There are three deep water ports in Vietnam which can handle up to 75,000 dwt, Panamax sized ships. These are the Phu My and Cai Mep Interflour ports near Ho Chi Minh City, and the Quang Ninh port in Cai Nan.

- The futures expire on the 15 th day of the contract month, and the options expire on the last Friday of the prior contract month. To hedge until end of June, the July contract months for futures and options are used.

- The nearest Out-of-Money put strike, for underlying futures price of 385, is the 380 strike.

- Option parameters assumed were: interest rate = 3%, volatility = 25%, days till expiration = 90.

- Cash flow from exercising put = strike price – futures price = 380 – 320 = 60

- The nearest Out-of-Money Call strike, for an underlying futures price of 385, is the 390 strike.

- Option parameters assumed were: interest rate = 3%, volatility = 25%, days till expiration = 90

- Cash flow from exercising call = futures price – strike price = 440 – 390 = 50