{kind=link}

Can participants retain their OTC trading flexibility while accessing cleared liquidity for FX? Simply put, yes.

This article explores why there is a growing appreciation of how the efficiencies of central clearing can be equally applicable to parts of the FX market, as they have been in other financial products, and why more participants are voluntarily choosing to trade listed FX as a complement to OTC trading as the most efficient mechanism to access the benefits of clearing, while retaining the flexibility they expect and require.

Top line

The benefits of listed FX are meaningful for many – from capital efficiencies to a wider range of liquidity providers – yet many end-user participants remain exclusively in the bilateral OTC market as they perceive a lack of support from liquidity providers and/or lack of relevant infrastructure to make the transition operationally efficient and the structure too rigid.

However, recent changes in listed FX have reduced the cost of trading, made the products a closer proxy to the OTC market, and enabled a wider choice of trading mechanisms to suit both electronic trading and the relationship-based negotiation that is familiar to many within the OTC market today – resulting in over 200 new entrants to our markets in the last 15 months.

Drivers for clearing

Unlike other financial products such as interest rate swaps and credit default swaps, there is currently no mandate for the central clearing for any of the products within the FX asset class. As such, any utilization of clearing is on a purely voluntary basis in order to mitigate challenges or to gain benefits that may not be available by remaining in the OTC market on a bilateral or intermediated basis.

For large dealers, the primary driver of adopting clearing for NDFs has been the impact of the uncleared margin rules (UMR) – they have embraced clearing to enable netting benefits and margin efficiencies. With phases 5 and 6 of UMR still to come in September 2021 and 2022, respectively, the wider impact on the buy-side remains to be seen. But given the direct impact of UMR on bilateral products like NDFs and FX options, UMR may well create a compelling case for entities ultimately caught by the regulations to consider migrating impacted trades to a cleared alternative.

However, during 2020 and Q1 2021, we have already observed around 200 customers choosing to access clearing by adopting new currency pairs of FX futures or using FX futures for the first time, and this growth currently appears driven by a variety of other factors, many of which are unrelated to UMR. These factors include:

- Access to more liquidity providers and differentiated liquidity

- Netting of risk and positions against a highly rated CCP

- Ease of allocations and operational processing

- Freeing up bilateral lines and no need for ISDAs

- All-to-all anonymous and credit agnostic pricing

- Firm pricing with no last look

- Ability to trade passively

The listed FX CLOB, a source of cleared FX liquidity

Listed FX futures provide customers with a complementary source of liquidity and mechanism for risk transfer that is capital efficient, centrally cleared, and potentially available at a spread tighter than the OTC market. Trading FX futures is, however, synonymous with all-to-all trading in a central limit order book (CLOB), which may not be familiar to all customers.

For the 1,200+ customers familiar and comfortable with interacting with the CLOB, there are several benefits available to them, which include:

- Firm, all-to-all, credit agnostic pricing

- Regulated marketplace with easily evidenced best execution

- Fully automated post trade processing and allocations

- Ability to trade passively and to use algorithms

- Tighter pricing for outrights and calendar spreads by virtue of minimum price increment (“tick”) reductions of 50-60% in G5 currency pairs over the last 2 years

One of the unique differentiators underlying the value of the CLOB is the diversity of customers in the CME ecosystem, and by virtue of every contract being centrally cleared, every customer can trade against any other customer without an ISDA and on an anonymous, credit agnostic basis. This dynamic allows every customer to access the best price available in the market and enables the pricing in FX futures to potentially be very different to the spreads afforded to a customer in the OTC market.

{kind=link}

Voice vs. electronic, anonymous vs. disclosed

Trading listed FX on the CLOB may not suit everyone and, as such, other trading mechanisms are of growing importance to support the access to clearing for customer segments, including global macro Hedge Funds and Asset Managers.

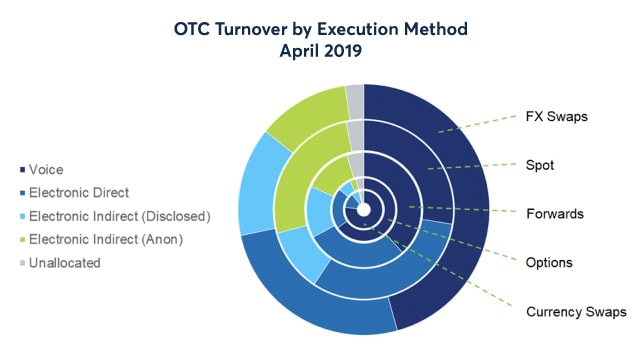

The 2019 BIS survey provided some detail on the types of trading methods used by FX market participants. Voice trading or, more generally, non-electronic trading, continues to represent a significant part of the market at over 40% of total FX volume, with this percentage being even higher when looking at FX swaps and options on a standalone basis.

{kind=link}

Source: BIS Triennial Central Bank Survey, 2019

Not only is the instrument type likely to influence how (and where) a trade is executed in the OTC market, but the type of customer involved in the trade is also likely to have a very big influence. The FX marketplace includes customers from retail investors to the largest and most sophisticated investment banks, and each individual customer in question will likely have very different trading preferences based on their own needs, resources, and experiences.

As a consequence, for a platform or ‘marketplace’ to resonate with multiple customer types and to support multiple FX instrument types, it would need a variety of trading mechanisms that customers could choose from, depending on the instrument, type of trade, and market conditions at the time of trading.

CLOB vs. EFRPs vs. blocks

In keeping with the OTC market, a wide range of trading mechanisms are both available and being actively leveraged by participants trading listed FX Futures and Options. Three key trading modalities available for accessing Listed FX are each very different and suit customers in differing ways – providing the same range of flexibility and choice as in the OTC market, but all resulting in a centrally cleared trade.

1. Central limit order book (CLOB)

The FX futures CLOB is a central execution point for firm orders, and by virtue of all the trades being centrally cleared, it is an all-to-all marketplace with every single customer being able to see and access the best price on a credit agnostic basis. All traders can trade passively by leaving resting orders in the orderbook, which enables them to potentially avoid paying any spread, as well as being able to trade immediately by aggressing on the best price at top of book. Prices in the CLOB can be viewed and accessed by several front-end trading platforms, including Bloomberg and Refinitiv.

2. Trading in blocks

Block trading in listed FX is a form of relationship-based trading that is akin to trading on a disclosed basis in the OTC market. Block trades are conducted away from the CLOB as privately negotiated transactions and, as such, blocks enable firms to leverage their bilateral OTC market relationships and to directly negotiate a price for the full size of their desired order before deciding whether to execute the position or not1.

Given the bilateral negotiation involved in blocks, this trading style allows the end user to access liquidity that may not be immediately available in the orderbook. For example, blocks are not necessarily reliant upon liquidity from the CLOB but, instead, leverage the liquidity of the counterpart(s) that the customer decides to contact. Recent refinements to the price increments at which futures block trades can be completed – in most cases to a tenth of a pip – have further increased the flexibility that block trading offers2.

A SAMPLE OF RECENT FXO BLOCK TRADES EXECUTED AT CME GROUP IS AS FOLLOWS:

| Date | Product | Contract Expiry | Strike | Volume (Lots) | Notional |

| 20 April 2021 | CAD Put | Sep 2021 | 0.7000 | 5000 | CAD 500Mn |

| 22 April 2021 | AUD Put | Sep 2021 | 0.6000 | 3000 | AUD 300Mn |

| 26 April 2021 | AUD Put | Aug 2021 | 0.5900 | 5000 | AUD 500Mn |

| 05 May 2021 | AUD Put | Sep 2021 | 0.6600 | 20294 | AUD 2.03Bn |

| 05 May 2021 | AUD Put | Sep 2021 | 0.6600 | 20294 | AUD 2.03Bn |

| 06 May 2021 | AUD Put | Sep 2021 | 0.6100 | 20000 | AUD 2.00Bn |

Source: CME Group, 2021

3. Exchange for Risk Positions (EFRPs)

The second mechanism of relationship-based trading available in listed FX is the exchange for physical, or EFP trade, which combines a spot FX trade with futures. As with block trading, these are privately negotiated transactions that enable customers to originate a position in the OTC market before then using an EFP to transition that risk in to listed FX. This approach resonates with customers who are executing multiple orders in the OTC market throughout the day but who value the benefits of netting all the resulting trades in one position against a highly rated central counterparty.

The concept of an EFP can be extended to an exchange for risk, or EFR trade. Again, this is a privately negotiated transaction. In this case, it supports the combination of a trade in a futures contract with a non-spot OTC FX transaction, such as a FX forward or FX swap3.

The link between OTC positions and FX futures

Our expectation for many customers active in the FX market is for them to retain access to the OTC market while also utilizing cleared FX products for efficiencies and access to complementary liquidity where it makes sense to do so. As a result, customers are likely to end up with ‘buckets’ of OTC risk against their bilateral counterparts (or FX prime Broker) and against their chosen central counterparty (CCP).

In this context, an additional tool for customers wishing to transition or optimize risk from the OTC market to FX futures, or for customers seeking a cleared alternative for FX swaps, is CME FX Link.

FX Link is a discrete product available in the CLOB that enables customers to see and trade on firm prices for the spread between OTC FX Spot and CME FX futures, with each trade resulting in the simultaneous execution of an FX futures contract and an OTC Spot FX transaction.

One of the use cases for this functionality is for customers to trade in OTC spot to establish their risk positions using their chosen liquidity providers and platforms, and to then utilize FX Link as a mechanism to flatten their OTC spot position and re-establish it in centrally cleared FX futures.

Bottom line

- There is currently no direct mandate for the central clearing of FX products, but there are a variety of potential catalysts for the voluntary adoption of clearing, ranging from macro factors such as UMR to trading based drivers such as access to differentiated liquidity.

- There is a broad range of trading styles across the global FX marketplace, reflecting the huge diversity of end-user customers and trading requirements. This range of trading styles needs to be available for customers to embrace the benefits of clearing.

- Listed FX offers a pool of cleared liquidity that is currently being utilized by over 1,200 customers.

- The CLOB remains the most widely recognized trading mechanism for listed FX, providing customers the ability to aggress on firm liquidity, trade passively using resting orders, or use algorithms from a variety of vendors.

- Relationship-based trading using OTC liquidity is, however, also very much available in Listed FX. Over 20 entities are now willing to facilitate blocks and/or EFRPs for their clients in CME listed FX products 4 , enabling customers to directly use OTC relationships to access the market.

To discuss these topics directly, please contact fxteam@cmegroup.com.

References

- See our white paper on block trading in FX for further details.

- See details on the recent rule changes for blocks and EFRPs here.

- See our white paper on EFRPs in listed FX for further details.

- Contact details of block and EFRP facilitators can be found here.